.png?width=141&height=141&name=Transact%20(1).png)

If there's anything certain about the current global economy, it's that eCommerce is advancing astoundingly. In the payments industry, the digital revolution has meant payments are becoming cashless. These payments are supporting the growth of digital economies, driving innovation, and are now a crucial for a business survival strategy.

Want to learn how to prepare your business for the changing payments industry? Download and read our guide today.

The division between bricks & mortar and digital commerce no longer exists. Global cashless payment volumes are escalating. Traditional businesses once firmly in the physical domain have now gone digital. While cash usage is down, contactless payments have risen, and e-Commerce payments are the way we do things every day.

Organizations have come to realize that when it comes to consumer preferences, omnichannel payments are the way of the future, and they must blend their payment channels into a seamless experience – or they won’t survive.

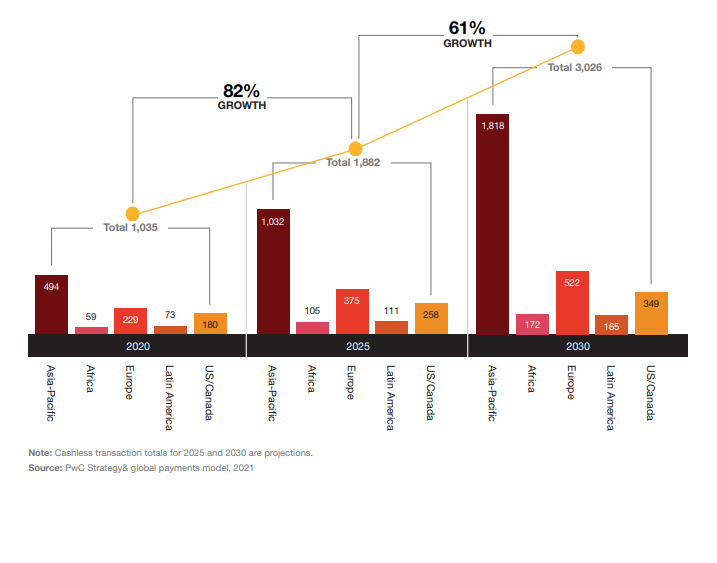

Image source: PwC

How are payments changing?

Underneath the shift to a cashless society there are larger, more prolific changes already making their way into the financial services industry and indeed the global economy.

Traditional ways of paying for goods and services, such as paper checks and analog invoices, are set for radical transformation. The whole infrastructure of the payments sector is being reshaped, with new business models emerging.

This transformation of the payments industry and in fact the global payments ecosystem involves two particular, and parallel trends:

-

An evolution of the front and back-end parts of the payment system , including instant payments, request to pay and plastic cards and digital wallets

-

A revolution involving huge structural changes to the payment mix and ecosystem, including the emergence of ‘buy now, pay later’ (BNPL) offerings, cryptocurrencies, and work underway on central bank digital currencies.

For fintechs and technology providers, business is booming. In the last decade, the fintech industry has experienced exponential growth. At the end of 2021, the industry was valued at US$3.56 trillion with expectations to grow at a compound annual growth rate of 23.58% between 2021 and 2025.

Key trends shaping the future of payments

PwC's revealing insights on the future of payments, shows six macro trends affecting the future of payments. These trends are driven by a combination of consumer preference, technology, regulation and Mergers & Acquisitions (M&A), and it's up to leadership teams to understand each of these trends in order to properly plan for their future.

Financial Inclusion and trust

According to The World Bank Group, in 2017, only 69% of the global adult population had a bank account or mobile wallet. This was quite a long way from the goal set for full financial inclusion by 2020.

Its Universal Financial Access program initiative was that by 2020, adults who were not part of the formal financial system would be able to have access to a transaction account to store money and send and receive payments.

This initiative, particularly in developing countries, will continue to be driven by mobile devices and access to affordable, convenient payment mechanisms. By 2025, smartphone penetration will likely reach 80% globally. This is due to an accelerated uptake in emerging markets such as Indonesia, Pakistan and Mexico.

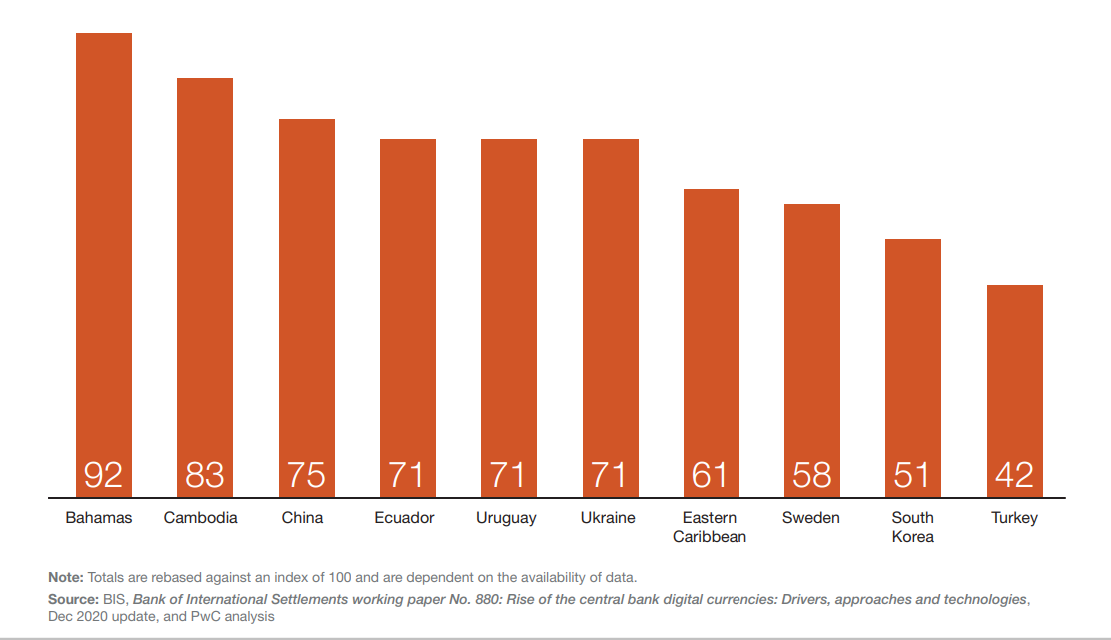

With Central Banks considering the feasibility of CBDCs, there is new emphasis on the role of supervisors to ensure data privacy and traceability for consumers and businesses.

Digital currencies

Central Banks Digital Currencies (CBDCs), are digital tokens or electronic records that represent the virtual form of a nation’s currency. These, along with private-sector cryptocurrencies are predicted to have the biggest disruptive impact over the next 20 years.

Financial institutions including Mastercard, Visa and BNY Mellon are already preparing to facilitate the use of CBDCs. And a recent survey by the Bank for International Settlements suggests that 60% of central banks are considering CBDCs and 14% are actively conducting pilot tests.

Digital wallets

Digital wallets enable consumers to load and store payment methods on their mobile phones, and access funding sources, such as cards or accounts, on any mobile device. These wallets will be increasingly important as a payment ‘front end,’ as exemplified by Apple Pay and the relaunched Google Pay, and the rise of super-apps WeChat Pay and Alipay in China.

Consumers are moving from card-based to account and QR code-based transactions. In response, traditional payments providers and financial services organisations have been partnering with or investing in digital wallet businesses to create payments platforms in keeping with rapidly shifting trends.

Cross-border payments

With the traditional correspondent banking model considered both cumbersome and costly, in the world of global payments, there has been a proliferation of non-bank payment providers.

New players and solutions are competing with bank and card-based solutions at scale, to provide instant, low-cost payment solutions. For example, the P27 initiative in the Nordic region, which integrates 27 million people across four countries and currencies in one ‘domestic’ instant payment system.

Read our comprehensive guide to cross-border payments here

Financial crime

With the pandemic driving an increase in eCommerce, it was always going to provide additional opportunities for fraudsters. In fact there was a 70% increase in fraudulent purchases in 2020 from the previous year.

Security, compliance, data-privacy risks and related issues were the top concern for banks, fintechs and asset managers in implementing a fully integrated technology strategy and payments system. This means the likelihood of greater collaboration among banks, payment providers and the public sector in preventing fraud and money laundering.

Retail Payments

When it comes to retail payments there needs to be flexibility. In the past, retailers' technology platforms limited them to what payment services they could integrate with. They were usually locked into one Payment Services Provider (PSP), and all their electronic payments transactions were handled by a local PSP chosen for its integration capabilities, rather than its innovation capabilities.

But today, innovative technologies in the retail payments landscape are helping keep up with consumers’ changing expectations, and with that, retailers need modern payments systems that extend their reach, and help them drive their business forward.

Open Banking

Today and in the near future, open banking has the potential to revolutionize the way we move and manage money.

The shift to digital channels has seen e-commerce, m-commerce and online banking use skyrocket. In 2020, mature markets like the UK and North America recorded between 75-80% of banking customers are now doing business online.

Research from PYMNTS.com shows that 46% of consumers shifted to digital and cashless payments following the onset of the pandemic.

As a result, the global online banking market is expected to hit $20.5 billion by 2026, up from $9.1 billion in 2019.

PSD2

Open Banking is often talked about in conjunction with PSD2, a piece of EU payments legislation which came into full effect in September 2019, and is aimed at improving digital payments capabilities and providing EU consumers with greater control over their financial data.

Sharing financial data across providers means that consumers can potentially use an app to have a single view of all their finances – and one place to manage it all, even if they have different bank accounts.

This also gives the opportunity for providers to overlay innovative services such as finance management or budgeting tools that create real value for consumers and strengthen their customer relationships.

IoT and the future of payments

The Internet of Things (IoT) is also affecting the payments landscape. This sector is growing by 15% every year, according to payments and banking analysts Mercator Advisory Group. The number of connected devices, like fridges, vehicles and machinery is growing exponentially, and presents significant sales opportunities for businesses that embrace IoT payments.

IoT payments can be triggered by specific 'events' to make automatic or semi-automatic payments.

What is the future of digital payments?

One of the main challenges faced by any organization is determining how and where to allocate resources to facilitate change, and bring about the types of significant transformation we've discussed in this blog. Payment leaders will need have a deeper understanding of where gaps in their payments infrastructure are, and where to prioritize.

To successfully secure the future today, it's critical for players in the payments ecosystem to understand what they need to do to stay relevant, while at the same time improving customer experience.

Let's look at some of the steps that these payments players are taking to rethink the way they do things. From banks, card networks and non bank providers to big tech companies, merchant providers, and third party processors, a global reshaping is taking place so that the financial services industry can keep up with payments trends and prepare for the future of payments.

Banks

-

Providing payment holidays

-

Adjusting pricing and reduce costs for remote services, for example through enhanced customer self-service options

-

Reducing dependence on transactional pricing in favour of subscription models

-

Optimizing partner sourcing and collaborating with other banks to create dispensing systems that ensure a continued supply of cash at lower cost

-

Rethinking their positioning in emerging open banking landscape.

Card Networks

-

Adjusting cost and investment plans to account for a collapse in pandemic-induced crossborder payments and foreign exchange business

-

Prioritizing solutions that help retailers and merchants enable e-commerce

-

Developing strategies for the emerging domination of alternative payment methods

-

Capturing account-based payment flows and improving coverage and capture of B2B payments

-

Integrating card and account-based rails into one system, leveraging ISO 20022.

-

Adding extra services on top of payment function and offerings.

-

Allowing for and engaging in local payment processing while maintaining global innovation.

Merchant Services Providers

-

Improving e-commerce and omnichannel capabilities to support retailers in their cashless transition.

-

Fostering terminal adoption and usage, particularly across small businesses

-

Launching digital sales and onboarding processes

-

Launching or upgrading merchant portals and self-service options

-

Upgrading fraud-detection, regulatory changes and counter-measures.

-

Expanding payment to checkout

-

Driving digital transactions and enabling the collection of rich transactional data.

Third Party Processors

-

Revisiting investment plans and cut spending on legacy platforms

-

Planing to transition to cloud-based, as-a-service models

-

Developing implementation road maps to enable issuers and merchants to offer virtual, instant, mobile-first products and services

-

Upgrading platforms and focusing on configurable, cloud-based architectures

-

Focusing more on the front end by rolling out fully digital, user-friendly interfaces to consumers and merchants

-

Refocusing sales efforts to extend beyond traditional banks and towards digital banks and payment service providers.

How IR Transact can ensure the success of your payments systems

IR Transact payment monitoring and performance management solutions bring real time visibility to your entire payments ecosystem so that businesses can streamline operations and reduce operating costs.

With transact you get data analytics that allow you the flexibility to add new payment types as well as elevating customer experience with real-time insights. Deep visibility and insight into all your inter-connected technologies from a single point of view ensures that you stay in control

This gives you the peace of mind that your systems are optimized and networks are running at their best.

Want to find out more about how to manage the evolving complexities of your payments environment? Download our essential guide.