.png?width=141&height=141&name=Transact%20(1).png)

Traditionally, nothing moves fast in the world of payments. But driven by consumer demand and a fluctuating global economy, at last instant payments are becoming firmly embedded in modern payment ecosystems.

Image source: PYMNTS

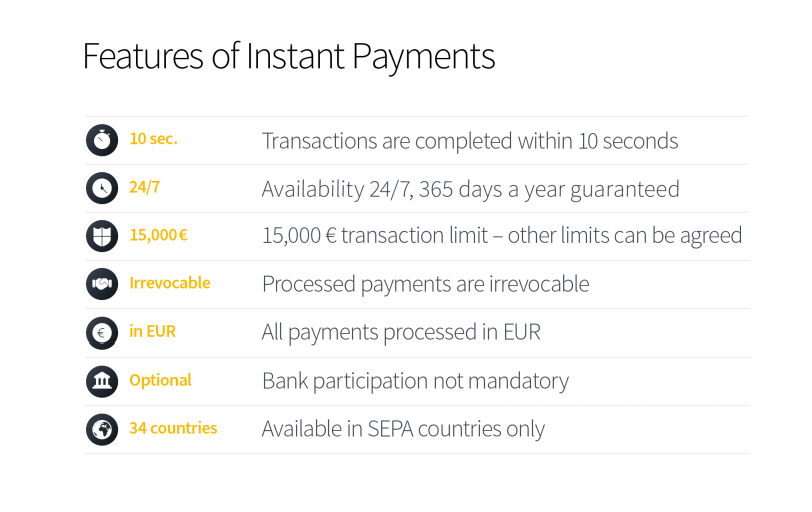

In November 2017, the Instant Payment System was launched by the European Central Bank making instant payments possible in any European payment area country, known as Single Euro Payments Area (SEPA)and also Switzerland and the UK.

These faster payments systems allow transfers to be processed directly between banks and financial organizations without the involvement of intermediaries such as clearing houses or correspondent banks. This means that transfers can be made very quickly and securely.

In this new era, consumers, businesses and payments stakeholders increasingly expect instant payments to be a standard feature offered by their banks and financial institutions. They're demanding the facility to transfer and receive payments and to access money between bank accounts not only domestically, but internationally, in real time.

Those financial organizations who don't offer instant payments, or those countries who lag behind with instant payment services can expect to lose valuable business.

For a comprehensive look at how instant payments are changing the world

What is an instant payment?

Instant payment systems enable consumers, businesses, and financial institutions to transfer money between bank accounts in near real-time. This means organizations can improve their liquidity and cash flow, as funds are transferred in seconds, rather than having to wait hours or even days for funds to clear.

Instant payments offer a faster, more affordable way to keep track of funds, obviously making funds available immediately, and streamlining the payment process.

Different instant payment methods

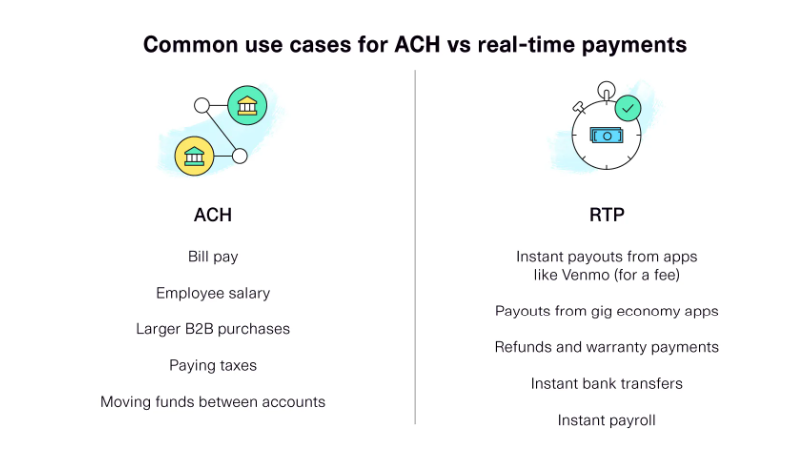

The terms instant payments and Real-Time Payments (RTP) are often thought to mean the same thing, but there are differences between the two.

Real time Payments (RTP)

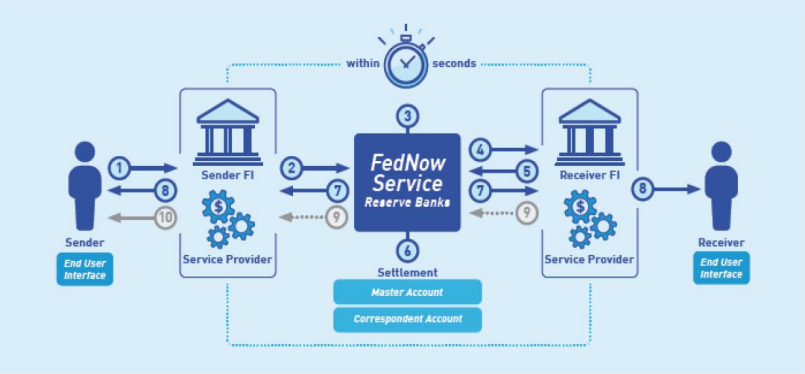

In the US, RTP is one of two instant payment rails (the infrastructure that moves money from one party to another) that process instant payments. RTP is operated by the Automated Clearing House (ACH), a member organization owned by all the major US banks.

FedNow service

The other instant payment rail is called FedNow, and is run by the Federal Reserve. In July 2023, the Federal Reserve invested $545 million to implement the FedNow Service, with banks and credit unions of all sizes. The Federal Reserve is a payment rail, and does not provide accounts or offer instant payment services to individual consumers and businesses.

Same-Day ACH

Same-Day ACH is an upgrade to the ACH network, allowing the processing of both credit and debit transactions several times daily. Same-day ACH is faster than traditional ACH, however it still may not be instantaneous, as it can still depend on submission times, the receiving bank's policies, and other intermediary banks involved in the transaction.

Image source: Plaid

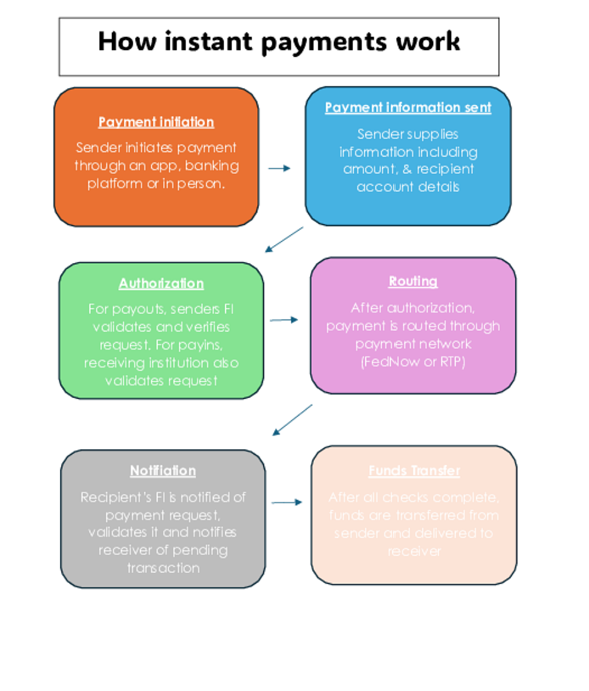

How do instant payments work?

While the process of executing instant payment transactions may look long and involved, the steps are fully automated and completed in a matter of seconds, with limited human involvement.

With recipients receiving funds immediately, the speed of this process makes instant payments a convenient option for a variety of financial transactions, including account-to-account payments, bill payments, and even eCommerce transactions.

-

Payment initiation. The sender, who can be a merchant, business or individual initiates the payment transaction through a mobile application, online banking platform or possibly even in person.

-

Payment information sent. The sender provides the relevant information such as recipient's details, account number, amount or any other requested information.

-

Authorization. For payouts, the sender's bank or financial institution validates the payment request, This includes verification of account balance and fraud checks. For payins, the receiving financial institution validates the request and obtains the payer's approval to send payment.

-

Routing. After the payment is authorized, it's routed through the payment service, either FedNow or RTP.

-

Notification. On the recipient's end, their financial institution is notified of the payment request and validates it, then notifies the receiver of the pending transfer

-

Funds Transfer. After checks are finalized, the funds are transferred from the sender's bank account and delivered to the receiver's bank account.

The features and benefits of instant payments

Instant payments offer a host of benefits for small businesses, large enterprises, individuals financial organizations and even for the global economy as a whole.

For example;

-

Outstanding bills and time sensitive payments can be settled more quickly, which improves liquidity.

-

Business partners benefit from faster payments, which makes collaborating easier and more streamlined.

-

There is far more transparency with instant payments regarding incoming and outgoing payments.

-

Faster payments also reduce the mechanics required to process payment transactions while still keeping transaction costs low.

-

As instant payments take only a few seconds, transactions no longer need to be manually checked or monitored.

-

Instant payments allow organizations to improve their cash flow, giving them more time to focus on their core business.

-

Banks and FIs can utilize instant payments to develop innovative financial services and strengthen their competitive position.

Image source: Coupa

Recalling an instant payment

While there are a myriad benefits with the instant payment system, the downside is that they are difficult if not impossible to recall. While a standard bank transfer has to go through the clearing process, allowing time to make corrections or recall the transaction, an instant payment is set up so that the money reaches the recipient's bank account within seconds, making it complicated to retrieve the money.

For this reason, senders should always ensure that the recipient's details such as IBAN, name and account number are checked and correct.

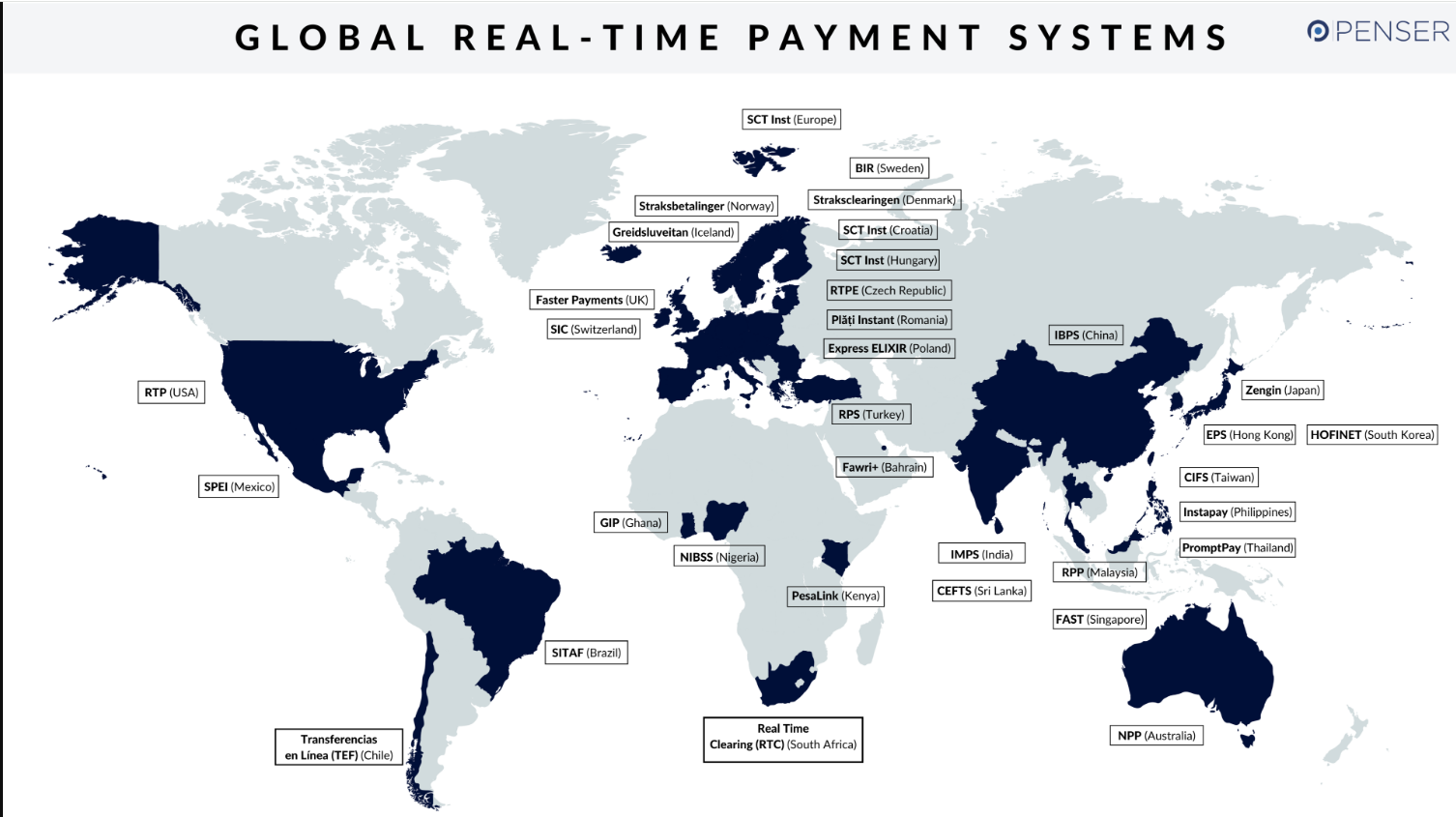

The global adoption of instant payments

In the last few years, most financial institutions across the globe have adopted instant payments solutions, and the number is rising exponentially. Here are some of the countries who offer instant payments schemes.

United Kingdom

![]()

The service has 35 participating organizations and over 400 other financial organizations, giving more than 52 million customers in the country immediate access to faster ways to transfer money. The Faster Payments infrastructure is built & operated by immediate payment solutions provider, Vocalink.

India

India’s real-time payments platform, IMPS was rated as the world's best instant payment service in 2019. It's managed by the National Payments Corporation of India (NPCI) and includes almost 200 banks and payment services in its network.

United States

![]()

In the US, The Clearing House, collectively owned by 25 financial organizations, provides the new technologies required for the US’s instant payment platform. It was launched in late 2017, and the network is available to any federally insured depository institution.

Learn more about the importance of payments resilience

Read what an expert has to say

How IR Transact can help

All payments infrastructures are complex, so it's imperative that you have real-time insights into all your payments data. Organizations need to have access to intelligence that can reveal and resolve issues affecting real time payments systems, such as:

-

Application performance or infrastructure issues related to customer payments

-

Performance problems and anomalies with specific payment types

-

The ability to handle payment volumes

-

System performance and root cause analysis

-

Fraud alerts for suspicious transactions or behavior

With an all-encompassing third-party performance management solution like IR Transact, financial organizations can gain unlimited access and insights into customer usage and end-to-end transaction performance metrics. This means the ability to increase transaction completion rates and improve stability across the entire delivery chain of payments.

An uncompromised, clear view of all metrics means that organizations can make proactive decisions instantaneously.

By gaining full visibility into their instant payment system, all players in the payments chain – from FIs to businesses, acquirers, and processors – can meet regulatory compliance requirements.

For more information on instant payments, read our payments blog