.png?width=141&height=141&name=Transact%20(1).png)

The financial services industry has undergone a massive shift in just a few short years. Digitization, and developing payment trends are changing the way consumers and retailers interact financially, and it's clear that the ability to accept digital payments is the pillar of today's global economies.

With the steady increase in mobile payments, and the growing collaboration between traditional financial institutions and the financial technology (fintech) industry, payment innovation has never been more exciting.

Customer expectations are high on the priority list for both businesses and financial institutions, and the ability to make and receive payments seamlessly and instantly, from anywhere in the world is no longer a wish-list item but an emerging reality.

Changing trends in payments

For quite a few years now, the fintech industry has been a major disrupter in the traditional payment industry, causing traditional banking institutions to rethink their banking infrastructure and payment technology.

With the rise of e-commerce, digital payments and mobile payment apps, customer demand means that a consistent digital payments experience across all their devices and platforms is non-negotiable. This includes frictionless payment methods, real time payments, digital wallets, open banking, mobile banking and cryptocurrencies.

In this in-depth article, we'll highlight eight of the most significant trends transforming the payments industry in 2024 and beyond, including:

-

The increase in global cashless payment volumes

-

The acceleration of cross-border, cross-currency instant and B2B payments

-

The use of data and analytics to streamline the customer journey

-

Innovations in security measures to reduce digital payments fraud

-

The increasing collaboration between fintechs and traditional payment providers

-

Developments in central bank digital currencies (CBDCs)

-

A2A payments set to challenge card usage

-

The continuing popularity of Buy Now Pay Later (BNPL)

Download a PDF of our guide to Managing Your Changing Payments Business

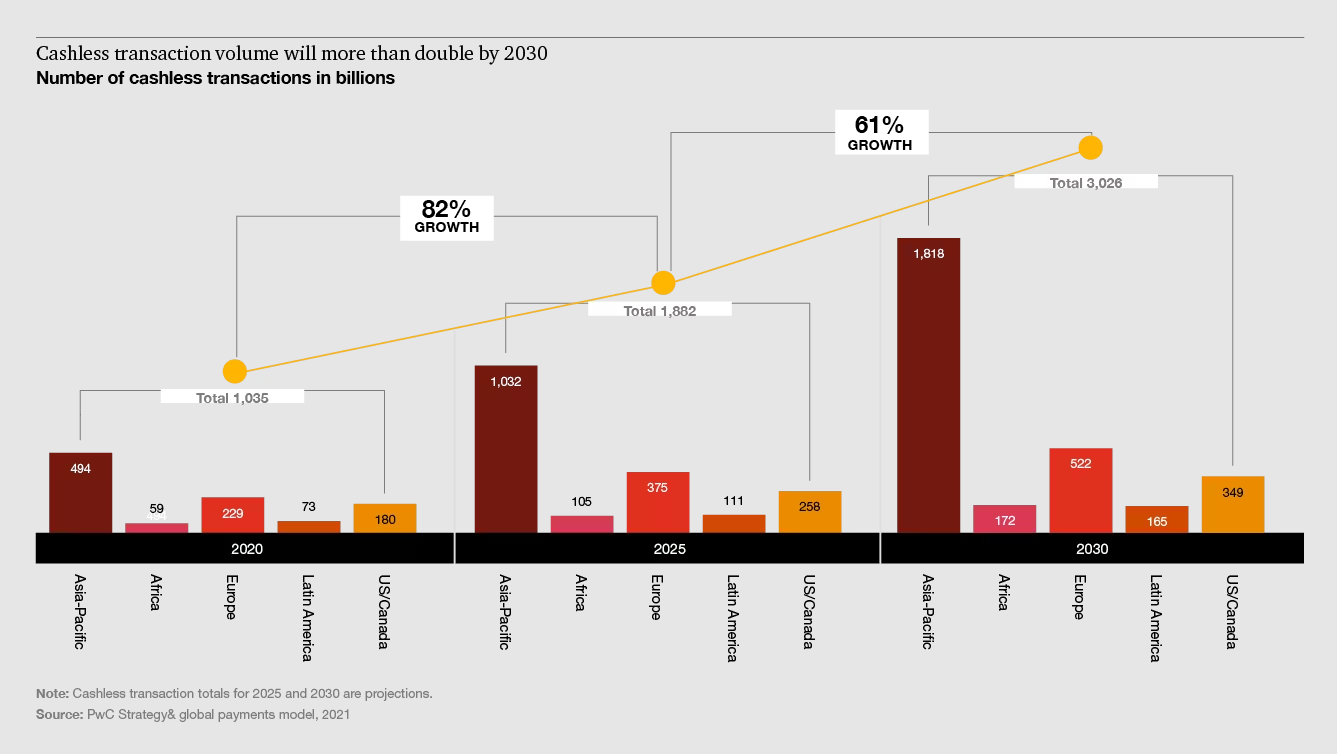

1. The rise in global cashless payment volumes

Global cashless payment volumes are predicted to increase by over 80% in the period between 2020 until 2025, according to a study by PwC Research.

The fastest growth is expected in the Asia-Pacific region, with cashless transaction volumes growing by 109% until 2025 and then by 76% percent from 2025 to 2030. The next most widespread adoption of digital payments is then predicted in Africa (78%, 64%) and Europe (64%, 39%). US and Canada are expected to grow less rapidly (43%, 35%), with credit and debit cards remaining preferred payment methods.

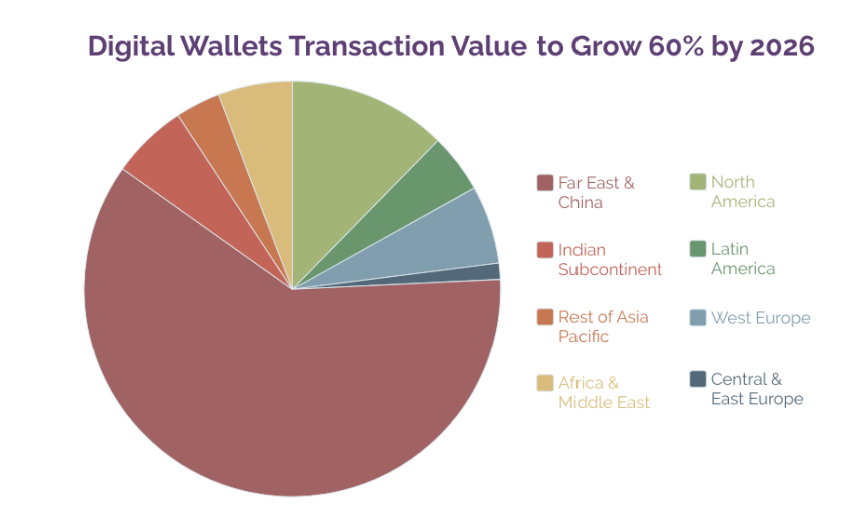

The increased use of digital wallets

Digital wallets are ubiquitous today, and not just with younger generation consumers. Mobile payments using Apple Pay, Google Pay, Alipay, PayPal and many other digital wallets have become the top preferences for consumer payments.

Digital wallets allow users to store and transfer money, make different types of mobile payments, and have a more streamlined payment experience.

The latest payment trends study from Juniper Research predicts that the global number of users of mobile wallets will exceed 5.2 billion in 2026, up from 3.4 billion in 2022.

Front end payment services like Apple Pay, Alipay and Google Pay have prompted businesses and banks to reshape their payment processes to remain competitive.

The traditional payment methods of credit or debit cards is stagnating, and the use of cash is diminishing in favor of mobile and digital wallets.

Image source:Payments

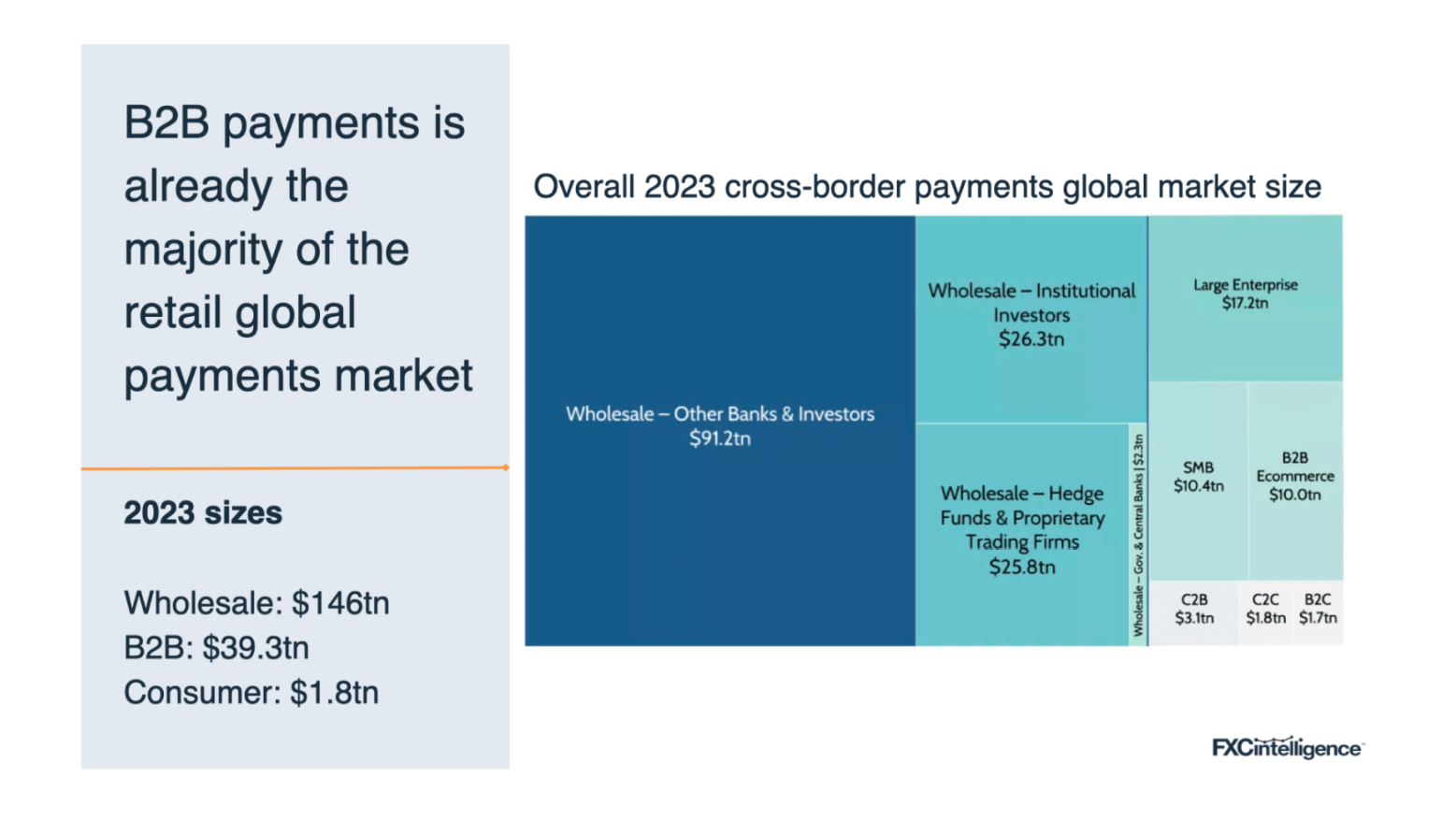

2. The acceleration of cross-border, cross-currency instant and B2B payments

Analyst firm FXC Intelligence reports that he B2B cross-border payments market will increase by 43% by 2030, and grow from $39.3 trillion to $56.1 trillion in the next seven years.

The report predicts that globally, B2B payments will grow from $190 trillion to $290 trillion by 2030, putting fintechs in a prime position to gain a significant market share.

New industry players and solutions are in direct competition with bank and card-based solutions at scale, for example the P27 initiative in the Nordic region, integrating 27 million people across four countries and currencies in one “domestic” instant payments system.

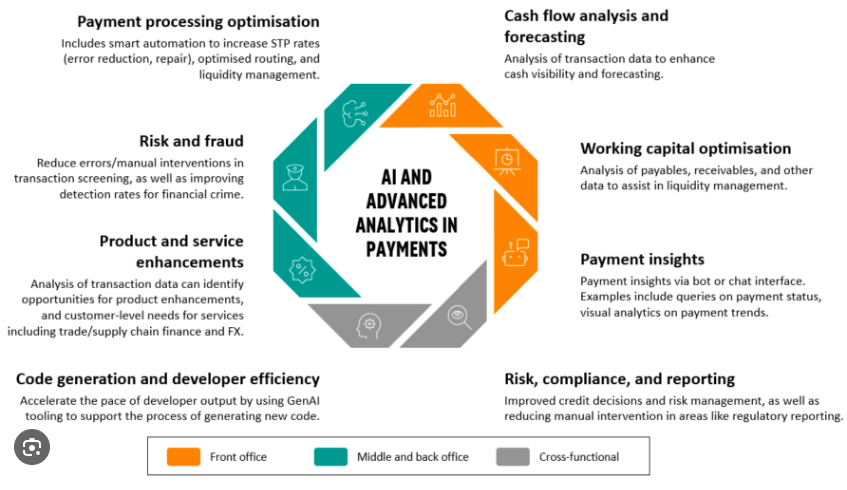

3. The use of customer data analytics and AI

With evolving consumer preferences, and the customer journey becoming more complex and multi-faceted, tools to facilitate the customer journey will grow more essential to CX-focused businesses.

The latest payment trends in the CX landscape indicate that businesses will need to consider adopting new service channels, focus more on leveraging innovative AI technology, and investing in automation. But within those mechanics, they’ll also need to ensure that they’re delivering customized, highly personal experiences, and at the same time protect customer data security and compliance.

As consumer demands continue to evolve, companies will need more innovative analytical tools and reporting systems to offer deeper and more granular insights into the customer experience.

AI and NLP

There's no doubt that AI tools are becoming prolific across almost every industry and these tools are changing how organizations manage and enhance customer experiences. Using vast amounts of historical data, companies can identify future trends and customer requirements - from using natural language processing systems to assess customer sentiment - to machine learning solutions for predictive analysis.

Today's intuitive AI tools can curate and consolidate data from multiple environments, converting vast volumes of data into actionable insights, and even delivering recommendations for business growth.

Generative AI tools can even personalize service by automating various parts of the customer's journey. Sentiment analysis can provide insights into how customers feel throughout each stage of their journey, and intuitive software can map their journeys across websites.

Image source: Mongo

4. Innovations in security measures to prevent digital payment fraud risk

To combat the escalating rate, scale, and sophistication of fraud, banks and financial institutions are increasingly relying on innovation and technology to prevent fraudulent transactions.

The digitalization of financial services, and today’s high-speed, high-volume transactions have rendered manual monitoring and rule-based systems inadequate in the fight against modern fraud techniques. Identity theft, malware attacks and phishing are difficult to detect with conventional tools, so banks and financial institutions are having to overhaul their security systems to identify fraud in real time, while finding a convenient and secure way to facilitate the customer experience.

AI and machine learning, biometric authentication methods, and advanced encryption techniques are methods being used to aid fraud detection and ensure secure transactions.

5. The increasing collaboration between fintechs and traditional payment providers

One of the fastest growing payment trends is the growing collaboration between traditional financial institutions and fintechs. While it's an inevitability, it's also a benefit to all entities.

Fintechs

Fintechs can leverage the global reach and regulatory expertise of banks to navigate legal complexities, reduce risks, foster smoother market entries, and ensure compliance and trust. Partnering with larger financial institutions gives fintechs an inroad to expand their services across multiple geographies and tailor their solutions to meet the diverse needs of customers in different regions

Banks

Banks can leverage the agility and scalability provided by fintechs' modern architectures, offering a way for banks to enhance their operations and stay competitive in the digital era. Fintech firms by nature are in the business of swiftly developing and deploying innovative solutions without the constraints of legacy systems that often burden traditional banks.

This agility is a huge benefit to banks, who can then respond more promptly to market trends, customer needs, and regulatory adjustments.

6. Developments in Central Bank Digital Currencies (CBDCs)

CBDC is a relatively new development in the world of finance, and its emergence has created several opportunities, and some debate in the payment solutions market.

CBDC is a digital form of fiat, or money that is issued by central banks as a digital representation of the country’s physical currency. Unlike cryptocurrencies like Bitcoin or Ethereum, CBDC has government backing, and is considered legal tender.

The aim of CBDC is to improve payments efficiency, reduce printing and storage costs and alleviate the need to transport physical cash.

Central Bank Digital Currencies is forging a new path in the current payment landscape. Central banks are exploring digital currencies and digital assets as a potential solution to major issues like low financial inclusion, money laundering and unregulated cryptocurrencies.

7. A2A payments set to challenge cards

The Account-to-Account (A2A) payment method allows digital payments or transfers between two bank accounts. A2A digital transactions connect bank accounts directly, eliminating the need for credit or debit card providers to be involved in the payment process.

In eCommerce, this also means that A2A payments are completed without leaving the merchant’s page, allowing for more frictionless payment processing.

According to the Global Payments Report 2023, A2A payments represent around $525B (or roughly €487.5B) in total eCommerce transaction value alone.

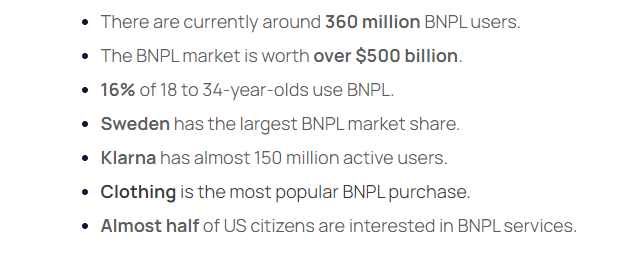

8. The continuing popularity of Buy Now Pay Later (BNPL)

The delayed payments platform, BNPL has vaulted into the mainstream payments industry so rapidly that it's become a first choice for a significant proportion of online shoppers globally.

According to latest research, half of UK adults had used BNPL digital payment methods by the start of 2024, up from 36% from the previous year.

The number of BNPL users in the US is expected to reach 82.1 million this year, and will exceed 100 million in 2025.

Globally, the figure is forecast to hit 900 million by 2027.

Image source: Exploding topics statistics

To process payments made through BNPL solutions, it's vital for businesses to have payment processors to handle these types of eCommerce transactions.

Some businesses have their own payment processor, while others integrate with different payment processors for more wide-reaching payments coverage

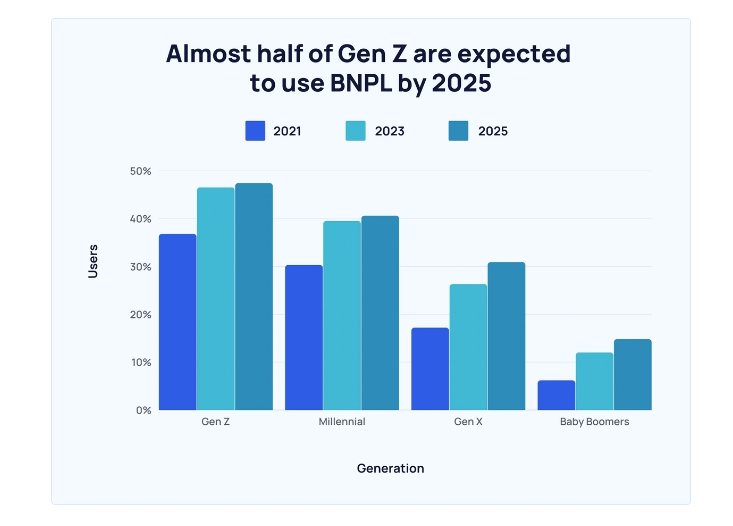

Benefits of BNPL for consumers

Increasing BNPL payment trends have taken the consumer payments space by storm, as it allows flexibility, and for many, a better control of finances.

BNPL providers give customers the option of buying items which they can receive immediately, but pay for them with flexible terms ranging from 3 months to multiple years, depending on the provider. Payments are interest free and sign-up is much faster than for credit cards.

Giving customers the option of dividing the cost of purchases into more affordable monthly installments, can make them more likely to purchase higher value items, or increase the quantity.

Image source: Exploding topics statistics

Retailers

The BNPL model can significantly increase customer conversions and cart size, offer value to existing customers, and also reach new customers. For example, providers such as Klarna claim that by adding the BPNL feature, client sales at Gymshark increased by 33%.

However, when a customer uses a BNPL provider to make a purchase, the provider charges the business a fee, which is usually between 2% and 8% of the total transaction. This means businesses need to factor in these additional costs, and if the BNPL method becomes their preferred mode of purchase, it could potentially have a negative impact on cash flow.

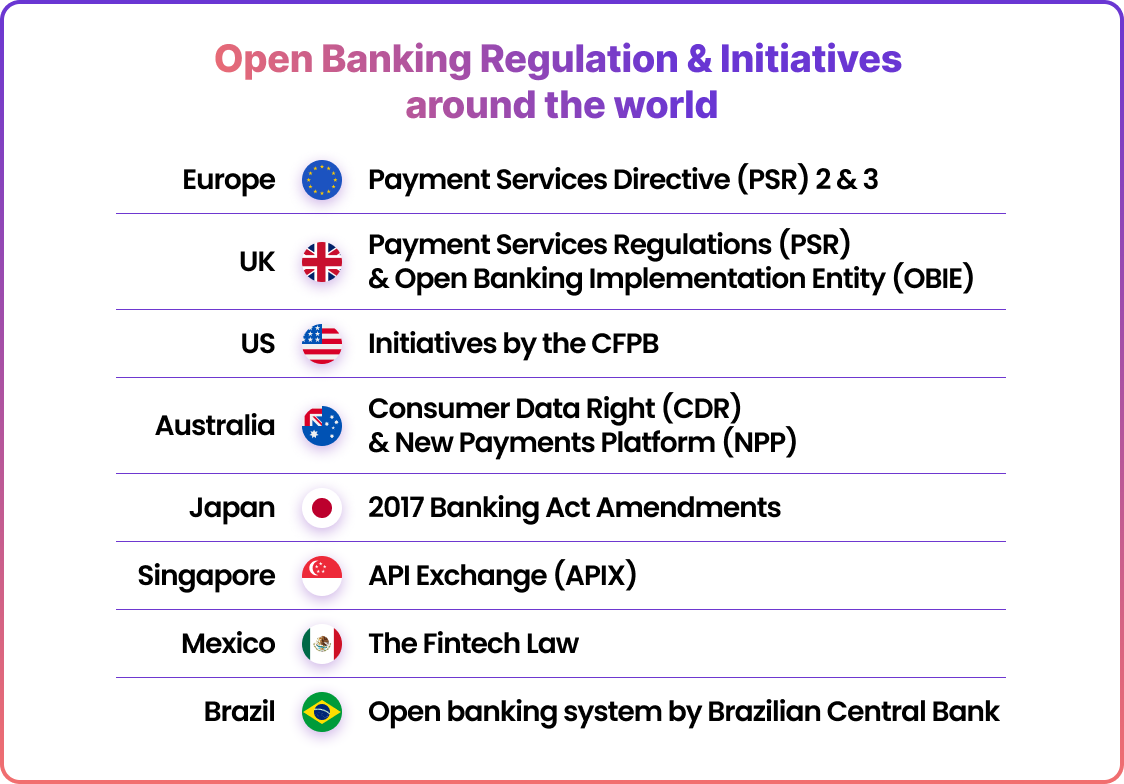

What is open banking?

Open banking is an initiative first introduced in the UK in 2018, that allows consumers (with their permission) to securely share their financial data with third-party organizations, such as fintech companies.

It represents a significant shift in the global financial services industry globally, offering a potentially huge scope of opportunities to enhance customer experiences, encourage competition, and ignite innovation.

Open banking acts as a conduit between banks and third-party providers, enabling the exchange of consumer banking data through secure Application Programming Interfaces (APIs).

However, there are many questions about the types of data shared with third parties and how that trust-based relationship can benefit all parties involved.

Security is the first and foremost concern, and banks need to fortify their infrastructure for their customers’ financial data to be shared more securely with third parties. Open banking doesn't mean that banks are allowed to easily sell their customers' data without their knowledge. Data sharing can only take place with customer authorization, and adhering to strict regulations.

Image source: Noda

Who benefits from open banking?

-

Financial service providers. Financial service providers can significantly innovate and tailor their product offerings to businesses.

-

Large and small businesses. Innovations by financial service providers will mean that businesses will have a more streamlined payments system. This could involve more automation, less time wasted on manual processes, and ultimately cost savings.

-

Customers. Open banking provides more efficient ways to control their spending, borrowing, and investing.

For merchants who wish to expand their business reach globally, or need to cater to regional markets, open banking offers additional flexibility in their digital transactions. It allows them to integrate new payment methods as demand emerges and to streamline payments as consumer preferences and digital platforms change.

Security of contactless payments

As a digital payment process, contactless payments (tap-and-go) continues to increase, but ensuring the security of transactions is a number one concern. This has always been a delicate balancing act for payment providers, because adding authentication steps can severely impair the user experience and consumer demand for speed and convenience.

Built-in biometrics, incorporating fingerprint, face and iris scanning sensors are already widespread in mobile devices, so adapting biometric payments for mobile payments and banking platforms is not a huge leap in facilitating transactions, and keeping them frictionless.

Image source: Visa

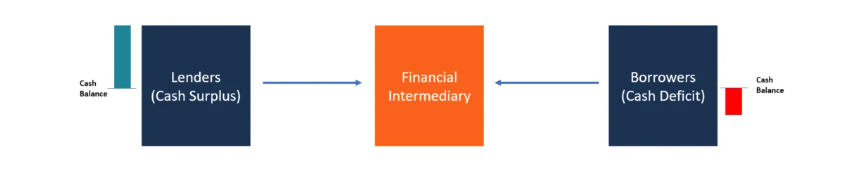

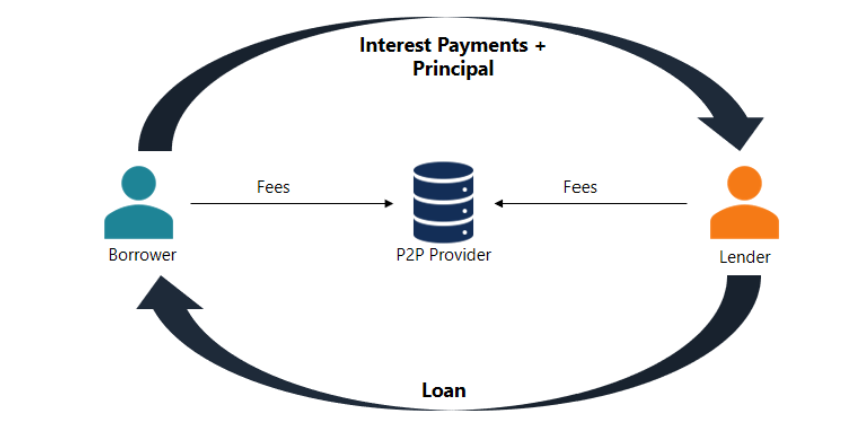

What is Peer-to-Peer (P2P) lending?

Peer-to-peer lending is the process of lending money to businesses or individuals without traditional payments providers or a traditional financial institution being involved. P2P lending is generally facilitated through online platforms matching lenders with potential borrowers.

Image source: CFI

How does Peer-to-Peer lending work?

In peer-to-peer lending, transactions are carried out through a specialized online platform with the completion of a loan application.

The platform assesses the application, risk and credit rating, and the available loan options and interest rate is assigned. The applicant is responsible for paying monthly interest payments, and repaying the principal amount at the agreed maturity date.

The company that maintains the online platform charges a fee for both borrowers and investors for the provided services.

Image source: CFI

The focus on Digital Identity Infrastructure

Consumers are demanding added security and protection of their financial data from payment fraud and identity theft in the modern digitally connected payment world.

Throughout the payment industry, the payment authentication process, once fragmented and inconsistent, is undergoing a global restructure. Biometric payments, two and three factor authentication (2FA & 3FA), facial recognition technologies and other security measures are better protecting online payments and customers.

According to a study by KBV Research, the global contactless biometrics technology market size will reach $18.6 billion by 2026. This represents 19.1% compound annual growth during the forecast period.

Real-time payments

Real-time payments (RTP) is one of the fastest-growing sectors in the global payments landscape today. Since 2021, its market size value has increased by approximately $3 billion with the upward trend expected to continue.

To facilitate the growth of RTP, there has been an increase in cloud-hosted Payments-as-a-Service (PaaS) solutions, and it's predicted that by 2025, 8 out of 10 financial institutions will use outsourced cloud and platform infrastructure.

The agility, flexibility, efficiency, lower upfront costs and scalability of PaaS cloud solutions are providing banks with the springboard they need to respond to the demand for real-time and cross border payments faster in the years to come.

Watch our real time payments webinar for more information

Data-based API business models continue to rise

With traditional revenue models becoming alarmingly less profitable, generating new revenue streams from financial and non-financial partnerships means that every bank and financial institution will need to build a strategy to leverage data-based APIs and open banking.

More streamlined APIs and the monetization of data are top considerations, as banks are being forced to invest in new data-led services. Less capital expenditure increases flexibility and the ability to offer new functions, payment schemes and clearing access, and to launch new products faster.

For example, Klarna, a Swedish FinTech offering payment plans (popular with younger Consumers), social shopping and finance, recently partnered with Simon, the largest shopping center operator in the U.S. , giving Simon shoppers access to Klarna's unique in-store payment solutions.

Consolidation is driving payment services and financial institutions to expand

Over the past 10 years, the payment industry has undergone massive waves of Mergers and Acquisitions (M & As). Payment firms are realizing the need for consolidation to increase their scale of operations, expand portfolios, extend geographical reach, and save costs.

For example, Ireland-based financial service company Stripe acquired Bouncer, a fraud-fighting authentication firm in May 2021, to enhance Stripe's fraud prevention tool.

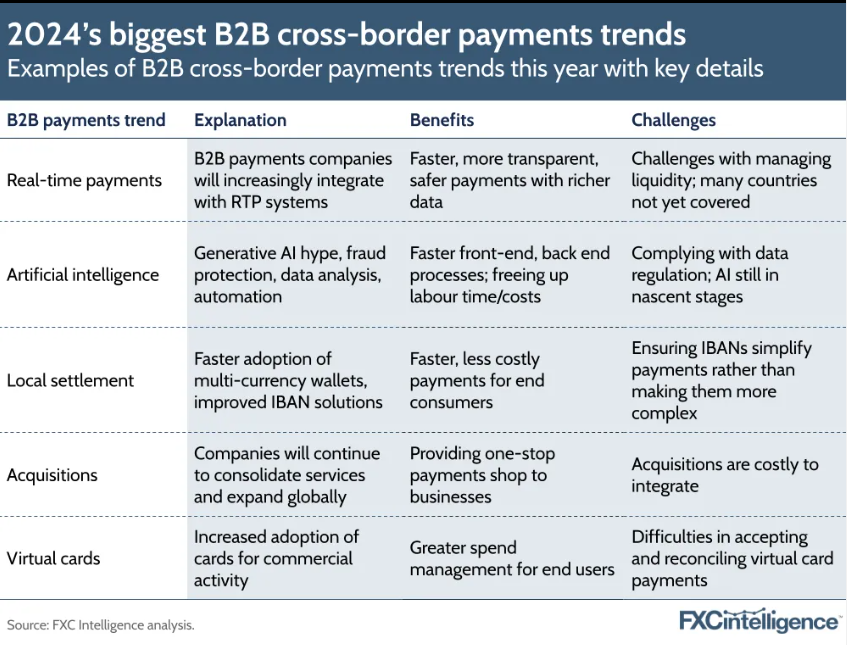

The challenges for Business to Business (B2B) digital payments

The cost and complexity that comes with overhauling the infrastructure used to process transactions are partly to blame for slower innovation in the B2B payments sector.

These types of transactions are typically high in volume but low in value. However, with the significant improvements in digital adoption across the payment ecosystem, global trade is increasing, with cross border business transactions globally could total $56.1 trillion by 2030, driven by growth across large enterprises and SMBs, as well as increased digitization.

Despite this, in some regions such as the United States, paper and offline-based transaction methods are still preferred payment methods for B2B transactions.

Image source: FXC Intelligence

The digitization of payments isn't just contained to retail. With real time mobile P2P transactions, digital remittances, and digital business payments continuing to blossom as change spreads through the ecosystem.

The importance of business data in the payments industry

Payments data is important because it identifies trends and patterns and creates actionable insights which can shape future business decisions. It allows businesses to operate in real time and can uncover actionable insights that can increase revenue and improve ROI.

Image: McKinsey

A major obstacle for FIs and other banks has always been the difficulty of accessing the right data in real time, due to disparity, lack of transparency, and speed.

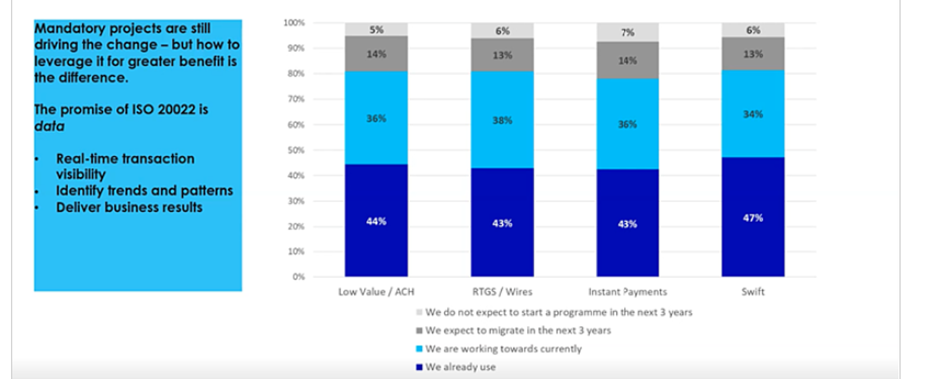

The massive adoption of ISO 20022 gives organizations the ability to access and analyze the data, not only in a message, but the ability to look across all the messages in a single data set and create analytical value from it.

“The information about a payment is as important as the payment itself,” Gareth Lodge, Celent

Real-time payment analytics are vital to measure, view growth and make decisions all the way through the payment chain, and across each different platform. This is even more important now with the impending global ISO 20022 migration.

For more information, read our informative summary, and watch the webinar.

The Payments Glacier - The slow and steady move into 2024

Observability

In the face of change, it’s more important than ever that financial organizations can stay on top of their environments.

There will be a key focus on real-time observability as a mechanism to break down silos across teams, optimize payment systems, improve proactive problem resolution, and ensure reliability throughout.

In 2024, even the most minor movements in the payments landscape will have profound changes on the way both organizations and their customers transact. This presents challenges, but also many opportunities for those well-placed to capture them.

Observability will be critical to maintaining consumer confidence, winning new business, harnessing innovation, and ensuring sustained success in the long term.

Optimizing and protecting your payments systems with IR Transact

IR Transact is a third-party payments transaction monitoring solution that's non-intrusive, and integrates seamlessly into the existing enterprise environment.

Transact brings real-time visibility to your entire payment ecosystem. It collects data from all silos across the payments system, filters, correlates and analyzes this information and brings it into a single application.

Keeping on top of emerging technologies, regulatory changes, cyber threats, and the introduction of new international payment standards is challenging. With ISO 20022 migration imminent, turning information into intelligence will assure the safe, efficient operation of payments systems worldwide.

Find out how building a resilient payment infrastructure can be a game-changer for businesses.

Download a PDF of our guide to Managing Your Changing Payments Business