.png?width=141&height=141&name=Transact%20(1).png)

Real-Time Gross Settlement (RTGS) is a payment system provided by the banks, that enables the instant and complete electronic settlement of funds from one bank to another and from one place to another. RTGS systems work on an individual order basis, meaning that transactions are settled at the same time when they take place and so there is no waiting period.

Once the transaction is completed, real-time gross settlement payments are final and irrevocable. In most countries, real time gross settlement systems are managed and run by their central banks.

How RTGS works

As the term suggests, real time means the settlement happens as soon as it is received from the sending bank. Gross settlement means transactions are handled and settled individually. This is the basis of a real-time gross settlement system.

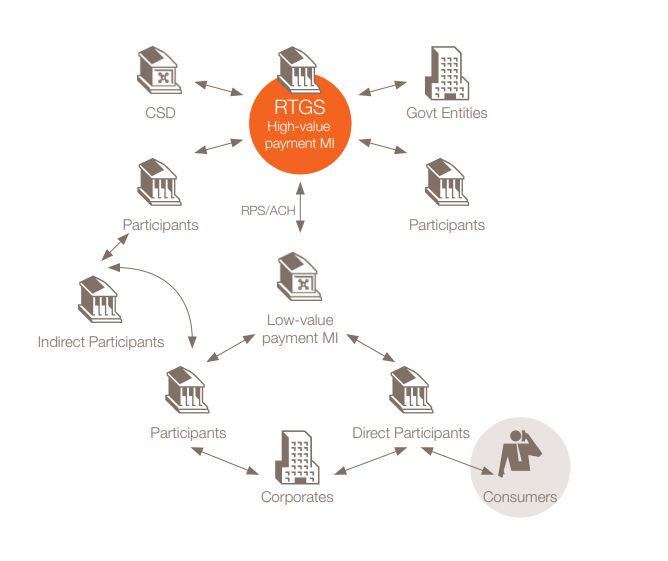

An RTGS system is generally used for wholesale, or high value interbank electronic funds transfers, often referred to as High Value Payments Systems (HVPS) or Large Value Payments Systems (LVPS). Real time gross settlement is operated and organized by a country’s central bank.

Image source: Bank of England

How RTGS is changing the global financial landscape

The first system resembling a real-time gross settlement system was the U.S. Fedwire system, which was launched in 1970. That system was an evolution of a previous telegraph-based system, which was used to transfer funds electronically between U.S. Federal Reserve banks. In 1984, the United Kingdom and France both implemented RTGS type systems.

Today, other countries have introduced their own RTGS-type systems:

- The British system is called the Clearing House Automated Payment System (CHAPS), and is currently run by the Bank of England.

- France and other Eurozone nations share a system called Trans-European Automated Real-time Gross Settlement Express Transfer System (TARGET2)

- In Hong Kong, it's called Clearing House Automated Transfer System (CHATS)

- Australia has Reserve Bank Information and Transfer System (RITS)

Image source: SWIFT Mirs White paper

Benefits of real time gross settlement vs DNS

RTGS lessens the possibility that one or more parties will fail to deliver on the terms of a contract at the agreed time. RTGS payment settlements occur in real-time throughout the day, instead of all together at the end of the day, as happens with a Deferred Net Settlement (DNS).

Although most financial institutions offer exceptionally high levels of security, cyber threats are constantly evolving, so it's imperative to have the most secure funds transfer system possible in place.

Real time gross settlement payment systems allow for a much smaller window of time within which sensitive financial information is vulnerable. This can be a serious mitigating factor against financial crime, helping to keep transactions safe and secure from the dangers posed by hackers or cyber criminals. With so much less time to work with, it’s far more difficult to exploit vulnerabilities, making RTGS bank transfer systems one of the most secure payment forms in the world.

DNS and the Herstatt risk

DNS is a net settlement system where final settlements occur between participating banks at the end of a predefined settlement cycle when the net obligations between participants are calculated and presented for settlement. This type of settlement system in high value payments can come with risks.

Another reason that real time gross settlement systems are a boon for global finance is the Herstatt risk, also known as settlement risk or cross-currency settlement risk.

The name is derived from the German Herstatt bank, which was closed down in 1974 for insolvency, when the bank's operations were suspended in the middle of a foreign currency exchange transaction. Because bank operations were suspended, individuals who had transferred currency (Deutschmarks) to Herstatt Bank never received the agreed upon exchange currency (US dollars), so the term Herstatt risk now refers to the transactional partner not settling the currency exchange.

With RTGS, the threat of a failed settlement is all but eliminated, as processing of funds happens within milliseconds.

Is your organisation adapting to emerging payments technology?

Why RTGS is vital for High Value Payments

The purpose of every real time gross settlement system is to provide final, and irrevocable settlement of transactions in a specific currency, through the transfer of the reserves held by central banks. They act on payment instructions, and settle each transaction by debiting the account of the paying bank and crediting the account of the receiving bank simultaneously.

Reserves are a vital tool of monetary policy. They are the cash balances that banks are required to hold at central banks. This limits the ability of banks to lend deposits without limit, and guarantees the stability of the financial system by ensuring banks can always settle their obligations to each other.

This makes RTGS systems essential for every central bank in managing the stability of the financial system, enabling a way to inject and withdraw liquidity.

But the benefits of credit risk mitigation through RTGS systems extend to all participants in financial markets, whether they are active in the money or securities markets, and whether they are linked to the RTGS system directly or indirectly

Image source: Swift Whitepaper

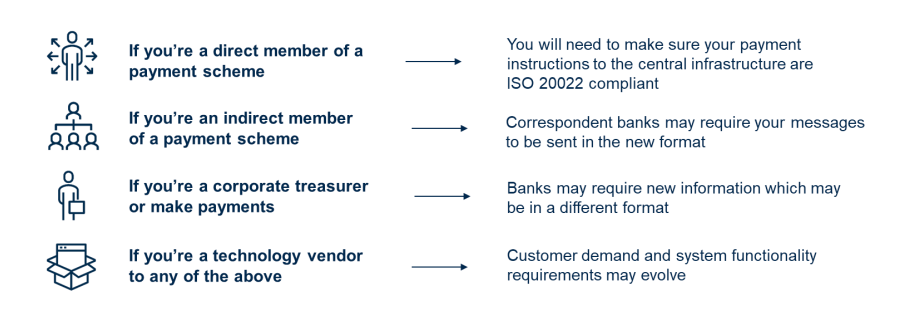

ISO 20022 standardization and why it's important for RTGS

The move to ISO 20022 by all major RTGS and high value payments systems globally is one of the most far-reaching initiatives in the financial services industry. ISO 20022 is now universally recognized as the “global, common language of financial communications” of the future. According to SWIFT, the proposed migration of all large value payments systems should be complete by 2023.

ISO 20022 payments message carries much richer information than the SWIFT MT messages and other legacy formats commonly in use today. Also, the information in an ISO 20022 message can be grouped together based on common data components from different payments methods and can be further reused, resulting in increased interoperability.

Image source: Bank of England

ISO 20022-based transactions provide additional functionalities too. They follow XML-based approaches, support non-Latin alphabets and offer improved remittance. This standard harmonizes formats that previously weren't compatible, and improves efficiency, as well as reducing cost and risk. Banks can now even leverage ISO 20022 and APIs as the standard for data exchange in payments within the applicable regulatory and compliance requirements.

Image source: Bank of England

The adoption of ISO 20022 improves data quality, enhances STP and reconciliation, encouraging higher automation and reduced cost. This improves operational resilience, and provides the ability to develop value-added services, and more effective fraud detection and prevention measures.

The consequences of RTGS failure

RTGS systems are vulnerable to the failure of technical components, and this threat is increased if back-up facilities are based on the same technologies as primary and secondary sites. Threats like cyber attacks, data corruption, hardware or software failure, even natural disasters can impact RTGS systems.

Image source: SWIFT MIRS whitepaper

Even a brief disruption to an RTGS system would be costly, but a prolonged failure would be catastrophic. When banks are unable to carry out real time gross settlement transactions, the commerce of entire economies can slow down, and even stop altogether. The money and securities markets, in which governments finance their expenditure, would also slow down and potentially dry up as the reintroduction of credit risk led to a loss of confidence.

The equity markets would freeze, and confidence in the economic health of any country affected by the disruption of its continuous RTGS system would evaporate, potentially resulting in the collapse of its currency.

The High Value Payments system taskforce

SWIFT, along with major global banks and market infrastructures have formed the HVPS+ (High Value Payments Plus) market practice task force. With the impending implementation of ISO 20022 standards, the task force has created a road map to harmonization for real time gross settlement and high value payments. Although it will provide a common foundation, the requirements of high value payments systems and providers are complex.

"Harmonizing messaging standards across High Value Payments Systems will create efficiencies for payment system participants and establish the foundation to develop new services.” Michael Knorr, Head of Payments & Liquidity Management, Financial Institutions Group, Wells Fargo Bank

High value payments systems play a crucial role in international finance as the ultimate settlement mechanism for cross-border markets and RTGS in multiple currencies. So it goes without saying that monitoring these large value payments systems with the right monitoring solution is critical.

What can payment analytics do?

Analytics gives us access to a mixture of traditional payment data as well as insight into what's happening inside an organization's payment system. Combining data about how a system is working with ad hoc reports, gives better insights into transaction data.

The power of data management and analytics comes from finding correlations between different points of data. This can help identify threats and fraud attempts. The ability to observe patterns within systems, and study related metrics, enables the detection of abnormalities.

How IR Transact can help your payments system

Whether it’s tracking card performance across all banking channels, looking for unusual transaction activity, or gaining a deeper understanding of customer behavior and channel profitability, all these processes require real time performance monitoring and data analytics.

If you want to grow your business, payments analytics tools are important in every sector of the payments space. The proper monitoring platform can make a difference to the revenue of any business. IR's solutions can help strengthen your business by providing in-depth payment analytics, insightful reports and clear visibility of your entire payments ecosystem.