.png?width=141&height=141&name=Transact%20(1).png)

There's no doubt that the world has entered a new era in payments. The digital age is ushering in an abundance of choice, convenience, speed and efficiency with the reinvention of the global payments ecosystem.

Find out more about how you can protect and manage your payments business with our guide today.

The days of doing business using cash, checks, ACH and wire transfers are disappearing. More and more customers expect instantaneous, high tech payment methods of using their money, and flexible product features, either online or from mobile devices.

But major credit bureaus and financial institutions are now having to tackle the ever-increasing problem of fraud prevention, as fraud continues to stand in the way of safe, secure transactions. And the cost to companies and consumers is staggering.

Monitor to manage risk

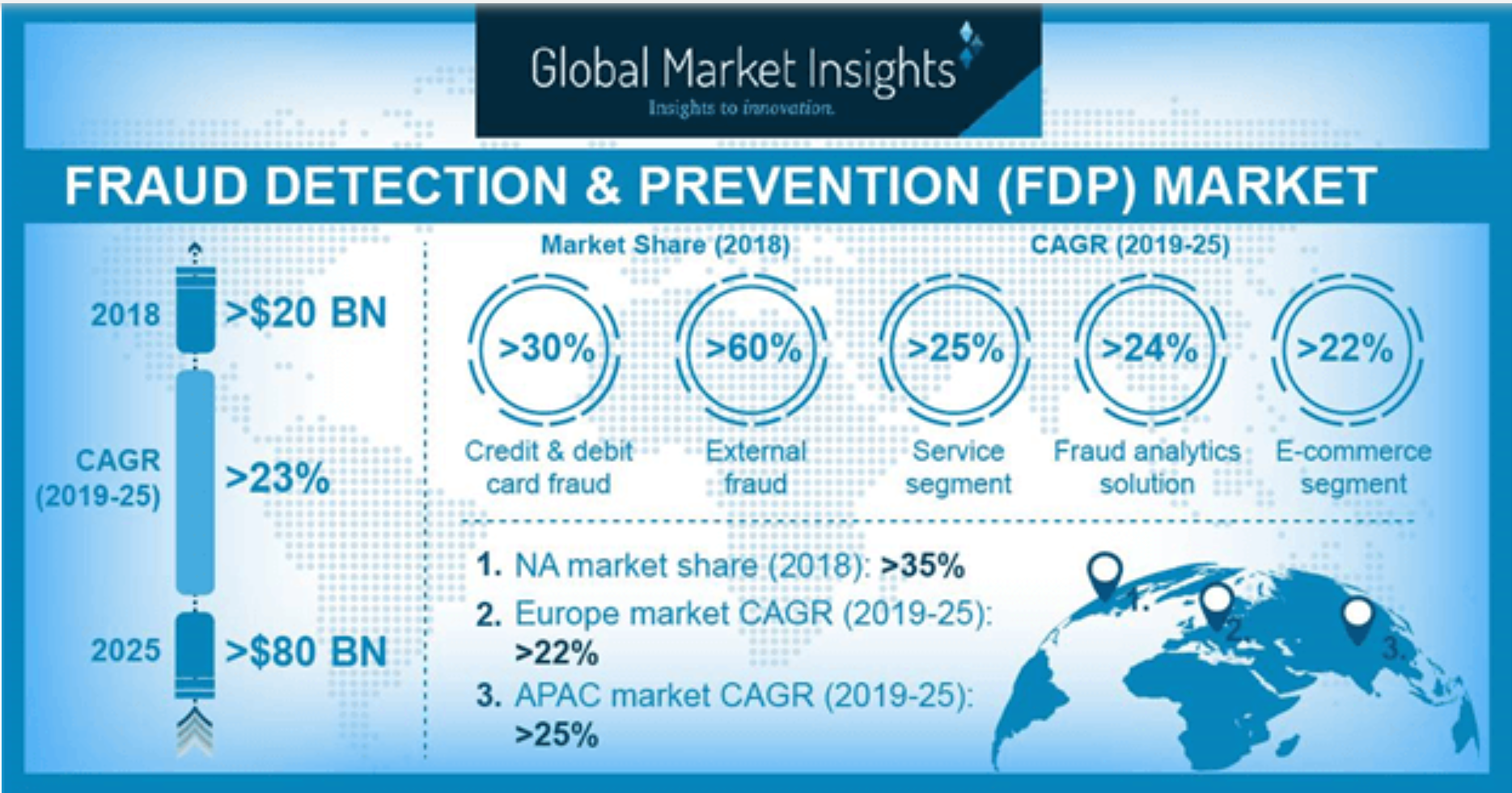

The Fraud Detection & Prevention (FDP) market is growing. Financial & government institutions are increasingly embracing fraud monitoring solutions to mitigate both external & internal frauds, contributing to the regional & global economy.

Let's look at why fraud monitoring is absolutely vital to keep on top of fraud detection issues like identity theft and suspicious behavior, digital security, and the challenges of keeping transactions secure for customers, merchants and financial institutions.

Image source: Global Market Insights

New convenience brings new risk

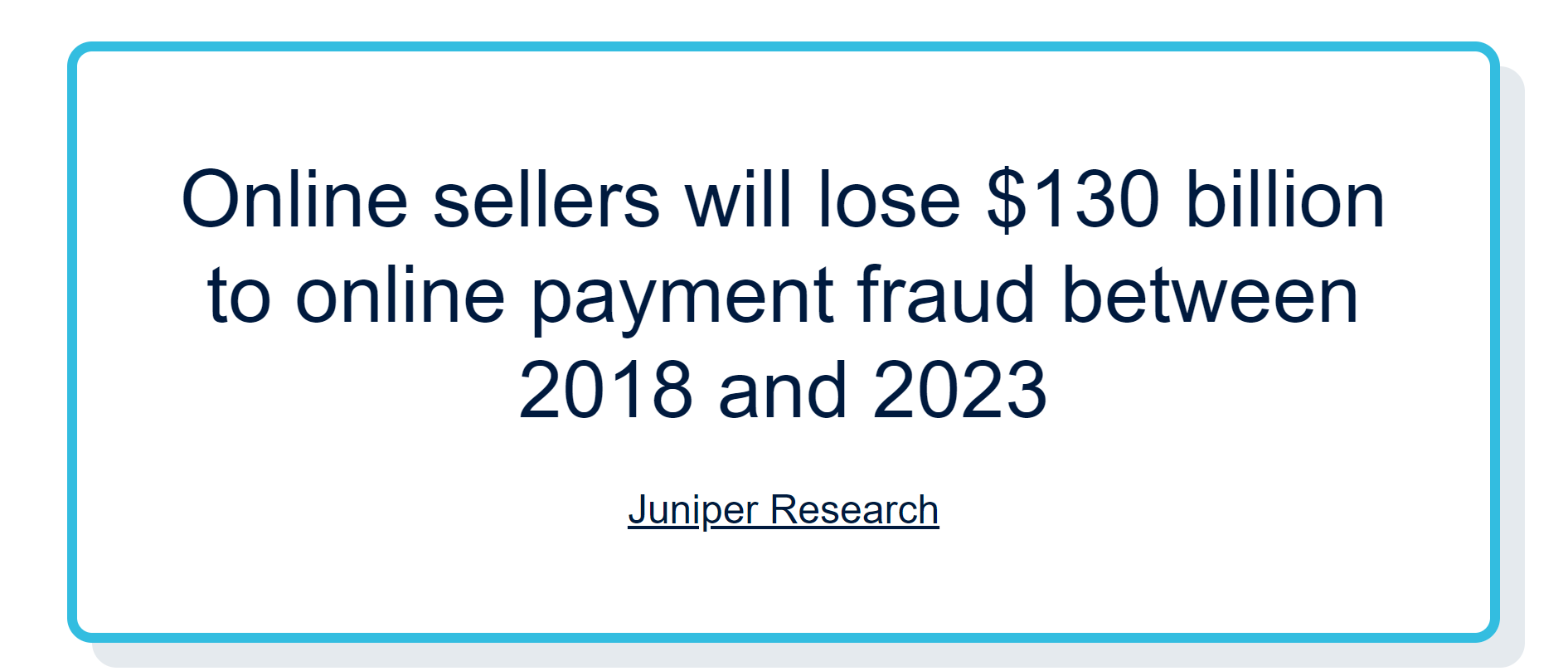

Due in large part to the COVID pandemic, online shopping has taken the world by storm. The global eCommerce market is predicted to grow to 4.9 trillion US dollars by 2021. By 2022 online sales will make up 17% of all global consumer sales.

The new ease and speed of digital transactions means that consumers are more likely to purchase, and this is great for financial institutions and businesses, but it also brings new opportunities for all kinds of online fraud and suspicious activity.

According to a report from TransUnion, the incidence of online fraud rose 25.07% in the first four months of 2021, compared to the last four months of 2020.

Establishing security

From identity theft to phishing and vishing attempts, as well as freebie, home-buying scams, authorized payment scams and more, financial institutions and banks are now faced with the increasingly serious issue of security. In order to protect their users, their first priority is implementing fraud protection.

As well as the broad range of ID theft (stolen identity) issues, fraud monitoring can help curtail other fraud related issues, and there are hundreds of them in constant circulation. For example:

- Debt collection fraud

- COVID-19 scams

- Mortgage fraud and home title monitoring

- Insurance fraud

- Bogus 'interest rate reduction' robocalls using artificial intelligence

- Prize and lottery fraud

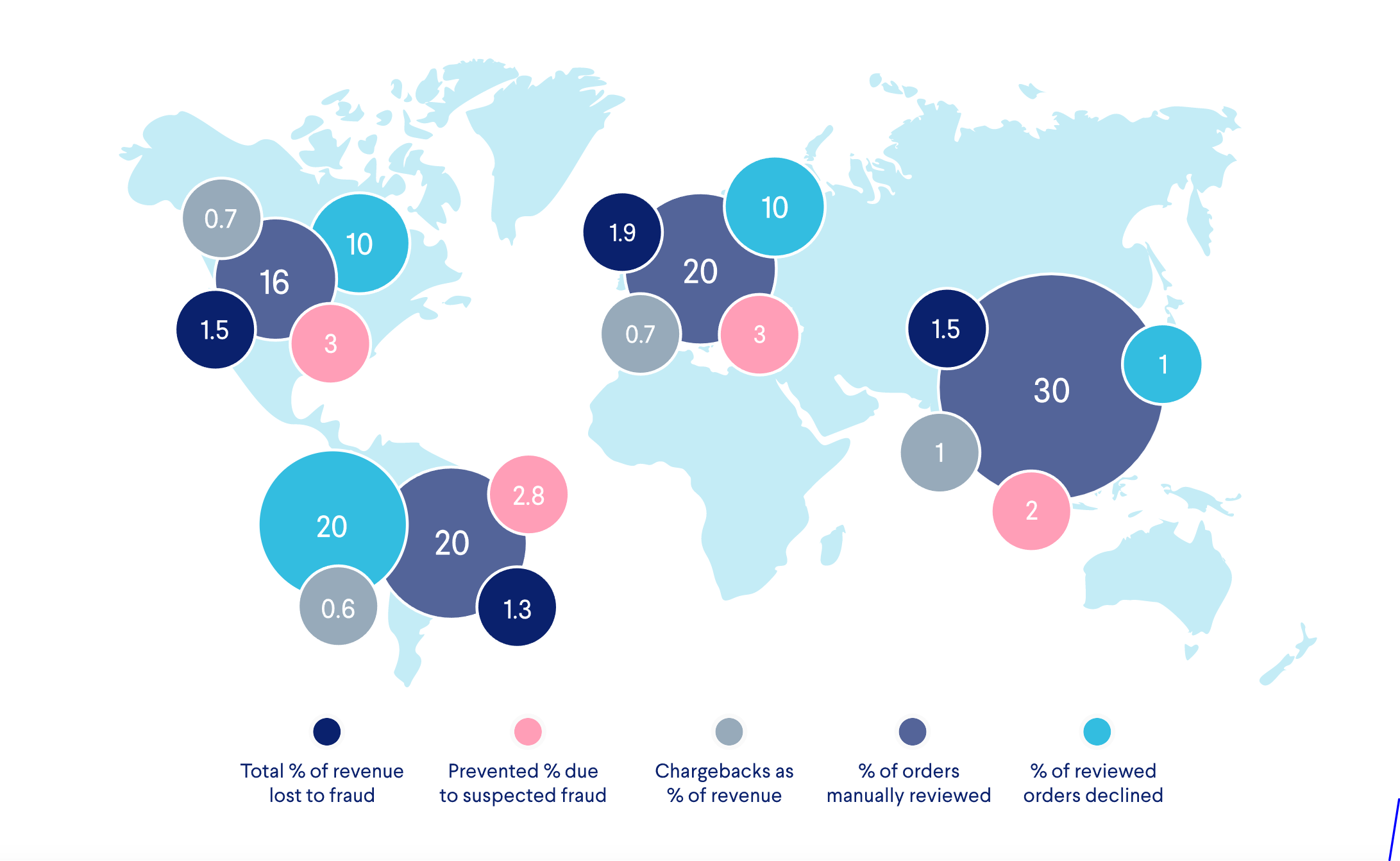

Image source: Ravelin

How online payment fraud happens

A significant proportion of online payment fraud occurrences involves identity theft, and can happen something like this:

- Criminals steal customer information by skimming payment pages, or purchasing customers bank account information, social security number, credit card or debit card information or other banking details on the Dark Web.

- Identity thieves use the stolen card or bank details to impersonate respective owners and in turn use stolen funds to purchase things online.

- The purchase appears valid to the online seller, who processes the payment, and send the goods to the thief.

- The cardholder notices the unauthorized transaction charges, contacts their bank, and most often, the online seller is landed with a charge-back plus fees.

Image source: Kount

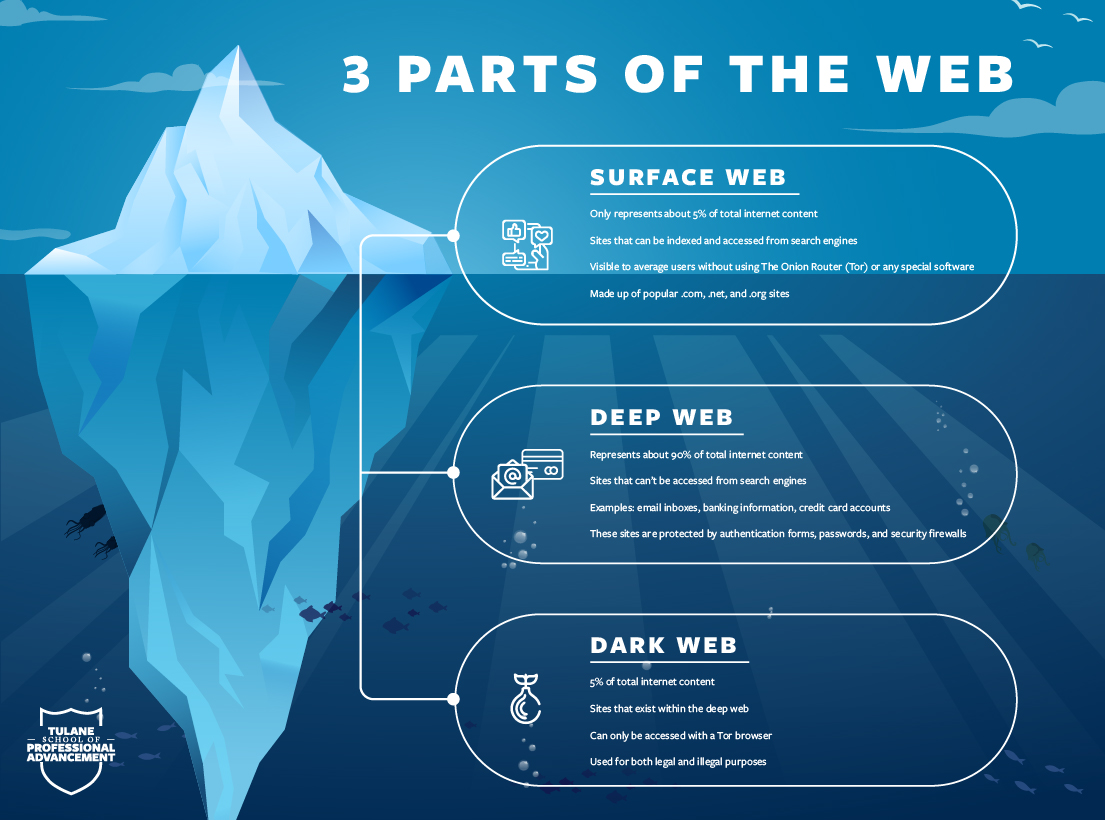

Shedding light on the Dark Web

The dark web is a murky corner of the internet where a vast, decentralized network of criminals can pool all their resources and interact without being traced. It's a place where fraudsters buy and sell debit and credit card details, collect personal data, and share information about how to go about committing fraud, what resources to use etc.

For the average online thief, buying customers card details and additional important information on the dark web is the easiest and fastest way to get large numbers of card details. The Forge Rock Consumer Identity Breach Report reveals that over 14 billion data records have been stolen and leaked, and used to commit online fraud since 2013.

The many facets of fraud monitoring

Fraud monitoring is an essential if not obvious fraud prevention strategy. Continuous fraud monitoring is the process of constantly monitoring all actions on a customer's bank account to detect anomalies or suspicious transactions. From the initial login to subsequent financial transactions such as payments and funds transfers, monitoring looks at all actions and events, whether they are monetary or non-monetary to fortify the process of fraud detection and identity theft protection.

By collecting and analyzing data, fraud monitoring can detect things like changes to an account owner’s profile, adding a beneficiary or payee, device registrations and many other actions that can create fraud alerts. Fraud prevention monitoring looks at data related to:

- Online and mobile banking sessions

- Devices

- IP addresses

- The activities and financial behavior of customers

Continuous fraud monitoring

Fraud detection involves ongoing monitoring in two key areas. Fraud analysts, fraud managers, and other professionals involved with fraud detection generally use two common terms to describe how they approach security and protect customers from identity theft:

- Continuous transaction monitoring

- Continuous session monitoring

Continuous transaction monitoring

To detect risk, continuous transaction monitoring will use analytical resources to look at all user actions – monetary and non-monetary, sensitive and non-sensitive, and will monitor each step from the login attempt to the transaction.

As part of this continuous monitoring, the anti-fraud system looks at actions and events like making changes to personal information like an account owner’s profile, adding a new beneficiary or payee, and registering a new device.

The fraud prevention system analyzes data related to the attempt and the outcome, either successful or failed. This builds a historical profile for each customer action before, during and after the action takes place. Creating this detailed historical profile helps the system identify anomalies (behaviors inconsistent with the account owner’s typical banking behavior) that alert financial institutions that fraud may be occurring.

Continuous session monitoring

Fraud detection through continuous session monitoring only applies to the banking session. It analyzes all events across all channels and devices to identify potential risks. For example, if the banking session started on a PC but was authenticated with a mobile device. Or, if the user initiates a payment from one country and authenticates it in another, the financial institution can help prevent fraud by forcing authentication with the device that was used to initiate the session.

Download our guide to managing and optimizing your payments business with payments monitoring.

The role of machine learning in fraud detection

Machine learning is a type of artificial intelligence (AI) and is one of the most important resources in the process of fraud monitoring and fraud detection. Unlike humans, it can analyze massive volumes of data in real time.

Most online fraud detection and prevention systems used by financial institutions rely on fraud rules. In fraud prevention, machine learning works to supplement the role of the rules engine, and works by using data to contrast normal behavior against suspicious behavior, such as the behavior of a bot or attacker.

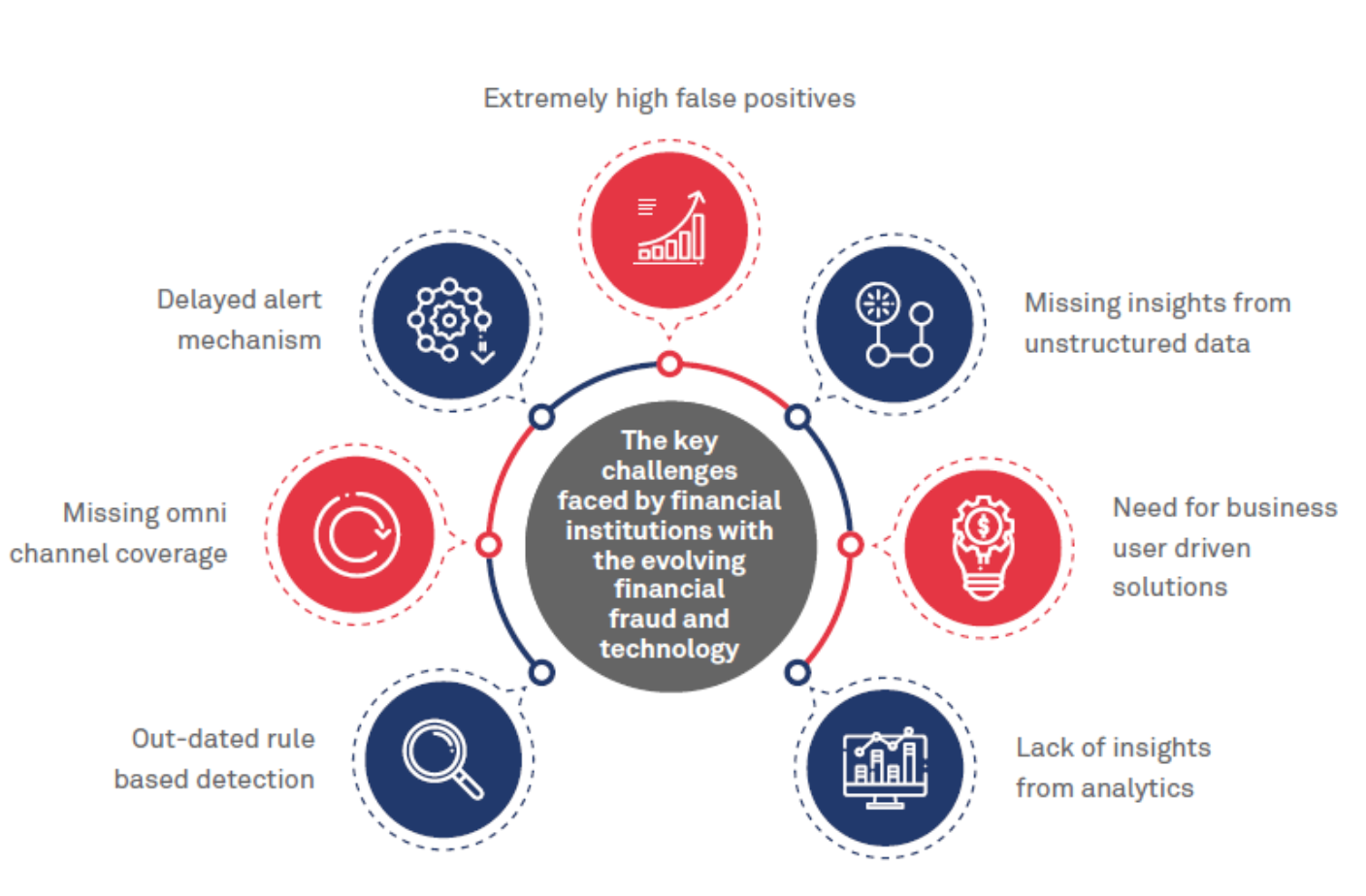

Challenges of fraud detection

Since criminals are always on the lookout to find new and innovative ways to get around systems and steal personal information to commit fraud, there are some of the challenges that complicate the fraud detection process.

Image source: Wipro

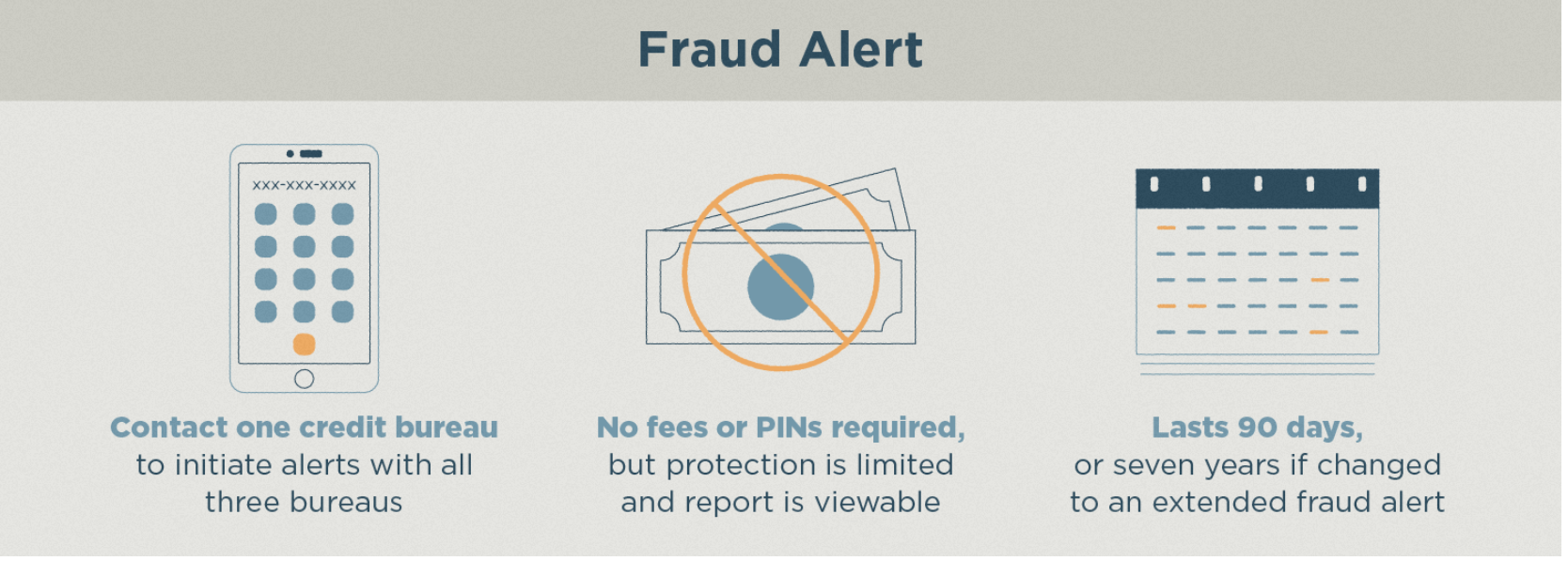

Initiating a fraud alert

Your credit score is important to your future ability to obtain credit. In the case of fraud, including identity theft, fraud alerts are notices placed on credit reports to alert credit card companies that a user may have been a victim. A fraud alert doesn't affect credit scores, but alerts creditors to take extra action to verify a customer's identity before doing business with them.

Credit monitoring

Credit monitoring, through credit services companies like Equifax can be a helpful tool in credit monitoring and spotting fraud, but doesn't prevent identity theft.

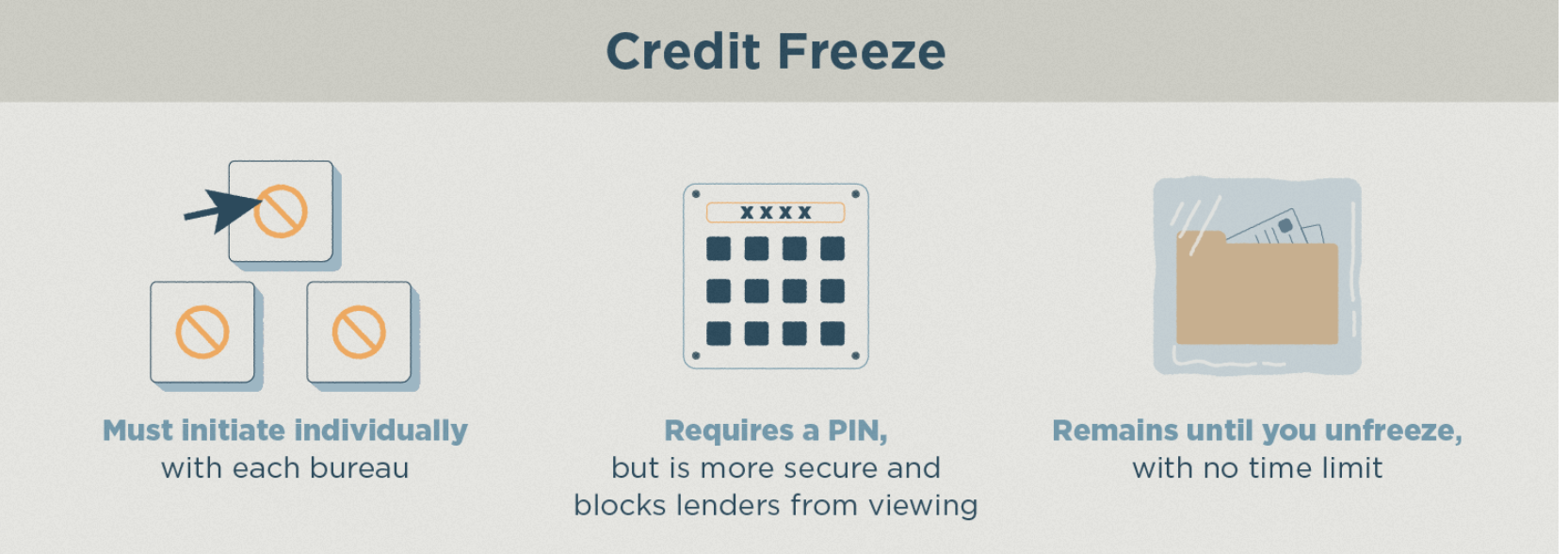

Preventing risk with a credit freeze

An effective resource to use against thieves taking advantage of stolen personal information is to enable a credit or security freeze at credit reporting services like Equifax, Experian, and TransUnion that stops these agencies from releasing your credit report.

Unlike credit monitoring, this is a proactive approach to ensure your information is not used to open fraudulent accounts. Even if a hacker does have your personal information, a credit freeze will likely help prevent them from using it to get loans or credit.

Image source: Lexington Law

Image source: Lexington Law

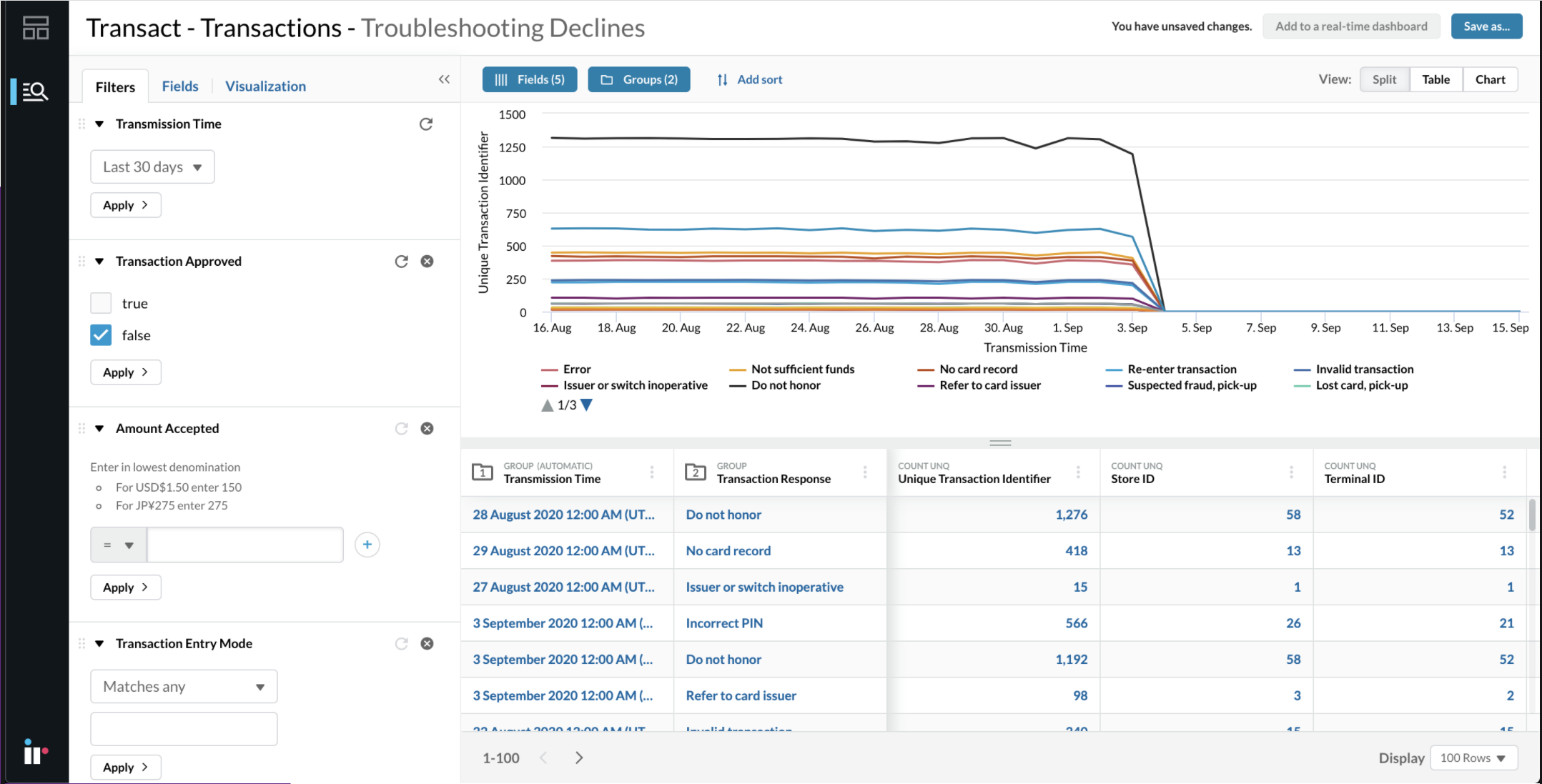

The importance of transaction analytics

The right analytics tools help give organizations visibility into their entire transaction and payments environment, providing valuable resources to grow business, increase security and fight fraud.

Analytics tools like IR Transact enable a better understanding of transactions, and system performance through resources like historical data, tying it back into real time transaction flow and reporting.

Find out more about how you can protect and manage your payments business with our guide today.