.png?width=141&height=141&name=Transact%20(1).png)

Sustained disruption in the world economic arena has prompted the unprecedented growth of real-time payments. Due in large part to a global pandemic, digitization and transformation that would have taken many years has been accelerated exponentially. The resulting boost to micro-digital economies in just a few short months, is unparalleled in the financial world.

Introduction

Before the COVID-19 pandemic, many countries were working towards a full real-time payments infrastructure at their own pace. In 2020, however, the pandemic accelerated dramatic changes towards a reliance on digital payments in general – and real-time payments specifically. Not only is the future of payments real-time - it’s here now.

COVID-19 has forced changes in business models, shifted consumer behavior, and created the need for increased flexibility, security, and speed. These crucial elements have seen real-time payments become one of the most significant and fast growing financial innovations of the last few years.

In 2015, only 14 countries had real-time payments capability. Today, 56 nations have implemented real-time payments, and the number continues to grow.

In this white paper, we’ll examine in detail the growth and accompanying complexity of the real-time payments market, focusing on emerging payment methods.

We’ll cast a spotlight on the main customer challenges and pain points, and how these can be overcome with the right insights and information.

We’ll highlight how banks and financial institutions are shifting their operational strategies from business-centric to customer experience (CX) and customer retention, facilitated by the adoption of real-time payments.

And we’ll look at how financial institutions can leverage payment data and analytics to mitigate compliance risk, and better understand and track revenue-generating opportunities.

Finally, we’ll summarize some of the key world regions, and biggest players in the burgeoning real-time payments market.

3 key reasons real-time payments are the future

With real-time payments becoming an aggressive global standard, the continued adoption, evolution, and demand of real-time capabilities worldwide emphasize the need to improve infrastructure and offer a more seamless real-time experience. Payment providers who embrace real-time as a priority will realize more value, efficiency, and competitive advantage.

1. Digital payments drive opportunity and growth

There are two critical imperatives for payments participants.

- Modernizing legacy infrastructures for the long term

- Leveraging Software as a Service (SaaS) to keep pace with continued changes in the digital payments space.

Digital payments create new revenue sources and opportunities through open payments and real-time banking. The modern, agile platforms increase efficiency (for example, using bots and AI), and lower the cost of servicing customers.

2. Data becomes currency

Data has quickly become a currency on its own and is the basis of the future of payments. Compared to old card networks, the richness and quality of data resulting from standardization like ISO 20022 has created fast, efficient, modern and flexible payment processing systems. Data adds real value, not only in enhanced customer experience, but also in a streamlining of business processes

3. End-to-end communication and business process simplification

The execution of a payment within a banking system is complex. Real-time payments can benefit financial institutions, merchants, consumers and society by enabling enhanced visibility into payments. By enabling better cash management and helping businesses efficiently manage day-to-day operations, real time payments improve liquidity. This can be incredibly valuable to smaller merchants, positively impacting their cash flow and daily sales outstanding (DSOs) instead of having to wait days for their settlement.

The complexity of emerging payment methods

To keep up with the fast-moving world of digital payments, financial institutions need to promise secure, frictionless real-time payments, while integrating the task of fighting fraud with new tactics, capabilities, and processes.

At the same time, today’s consumers expect to be offered seamless, fast, safe, easy options for money movement – fueling even more complexity on the backend for financial institutions.

Even before the pandemic, emerging digital trends were rapidly infiltrating the payments world. Then the unprecedented need for contactless payment options, faster transaction settlements, increased security and a better payment experience accelerated these trends.

With the enthusiastic adoption of new-gen payment methods like Buy Now Pay Later (BNPL), biometric payments, cryptocurrency and invisible payments, consumer engagement has changed forever. But with the continual growth of new payment solutions, financial institutions and payment firms face some practical dilemmas.

| Emerging payment methods | % of customers who currently use emerging payment methods | % of customers who will use emerging payment methods in the next 1-2 years | % of customers who face significant hurdles in their current payment experience (with traditional payment methods) | ||

| Buy Now Pay Later (BNPL) |

~20% | ~60% | ~40% | Of customers often use credit options for online purchases, strive to avoid high credit card charges, and demand new payment options for better purchasing power | |

| Invisible payments |

<10% | >45% | >30% | Of customers face high friction in payment checkout, both online and in-store | |

| Biometric payments |

~10% | ~50% | >50% | Of customers worry about transaction privacy and need better payment authentication solutions | |

| Cryptocurrency payments |

<10% | >45% | ~35% | Of customers witness increasing cross-border payment needs, concerned of higher transaction fees and lack of standardization in global payments | |

Challenges for banks and payment firms

Uncertainties and unfulfilled customer demands suggest a significant percentage of customers are unhappy with their payments experience. According to Capgemini Financial Services in their World Payment Report 2021,

“…There is a wide gap between what customers expect and what banks and payment firms prioritize. Attractive loyalty and rewards, frictionless

transaction experience, availability of options in alternate payments and sustainable and socially responsible payment products are the key areas in which gaps exist.”

The pressure is on banks and payment firms to rapidly accelerate their transformation efforts close these gaps and meet customer demands.

COVID-19 has exposed the criticality of modernizing legacy payment systems and prioritizing customer expectations. FinTechs are redefining the way organizations, businesses and customers interact and transact.

The growing dominance of mobile wallets, third-party payment platforms and cryptocurrency, has created increasing urgency to implement new, modern data platforms

| Customers’ expectations | Executives’ priorities | Wide gap | |

| 71% | Attractive loyalty and rewards | 43% | 28% |

| 82% | Frictionless transaction experience | 60% | 22% |

| 66% | Availability of options in alternate payments |

50% | 16% |

| 44% | Sustainable and socially responsible products |

33% | 11% |

| 45% | Cheaper and faster cross-border payments |

59% | 14% |

| 36% | Expanded beyond banking offerings |

49% | 13% |

Leveraging payment data to mitigate risk

Attaining a complete view of all message data for payments and trade-related messages across branches and correspondents is a key factor in identifying and quantifying global risk within an institution’s transaction activities.

For those payment firms using the SWIFT network, overlaying data from their in-house networks with SWIFT messaging data provides unique insights into payment flows without compromising data privacy and security.

FIs typically understand who they are receiving payments from but struggle to identify the other banks that are sitting behind the transaction. Monitoring payments traffic across the entire network means a better chance of proactively identifying potential pockets of risk and ensuring that risk policies are being followed throughout the network. These insights can then be used for manual review as part of ongoing AML/CFT AntiMoney Laundering operational processes.

An increasing regulatory focus on originator and beneficiary information means payments data quality should be constantly assessed to help identify problem areas. Monitoring data allows payment firms to ensure that payments meet relevant data quality standards.

The power of analytics

Building and maintaining a robust monitoring and analytics program in-house from the ground up can be a costly and time-consuming exercise. But the adoption of flexible, purpose-built analytics tools that can be configured according to an organization’s changing needs, can improve profitability, cut costs and mitigate risk.

- Analytics are vital to understand customer activity and behaviors, and to provide insights to providers’ risk profiles.

- Analytics allow clear visibility into an entire payments environment to identify anomalies, transaction performance issues and to help detect fraud.

- Analytics tools and monitoring solutions are vital to help businesses measure growth and make decisions throughout the payments chain and across different platforms.

Real-time payments have added another level of complexity to payment environments. This requires detailed, actionable, real-time insights to gain the business intelligence needed for digital transformation. Banks and FIs can utilize location and contextual data to create better customer experiences, create new data-based products and make more informed decisions in complex scenarios. Through effective monitoring and analysis, they can detect even the smallest changes and trigger immediate action.

Data management and analytics reveals correlations between different points of data to help identify threats and fraud attempts. Additionally, the ability to observe patterns within systems, and study related metrics, enables the detection of abnormalities.

How real-time transaction insights drive business growth

To truly capitalize on the opportunity of real-time payments, organizations globally must closely monitor their payments ecosystem and end-to-end performance.

The financial services industry deals with massive data volumes. Successfully planning for the future requires not only access to the relevant data, but the tools to analyze it according to an organization’s operational needs.

Transaction analytics and insights drive sales and provide more streamlined services to customers. For merchants and merchant acquirers, transaction monitoring identifies glitches in payment systems and mitigates the risk of fraud.

Transaction monitoring provides insights on how each payment channel is performing. For example:

For merchants – Identifying poorly performing payment systems leading to queues and bottlenecks, increasing the likelihood of abandoned purchases and poor customer experience

For financial institutions – Allowing FIs to see customer transactions and analyze customers’ historical information based on past and predicted

future activity.

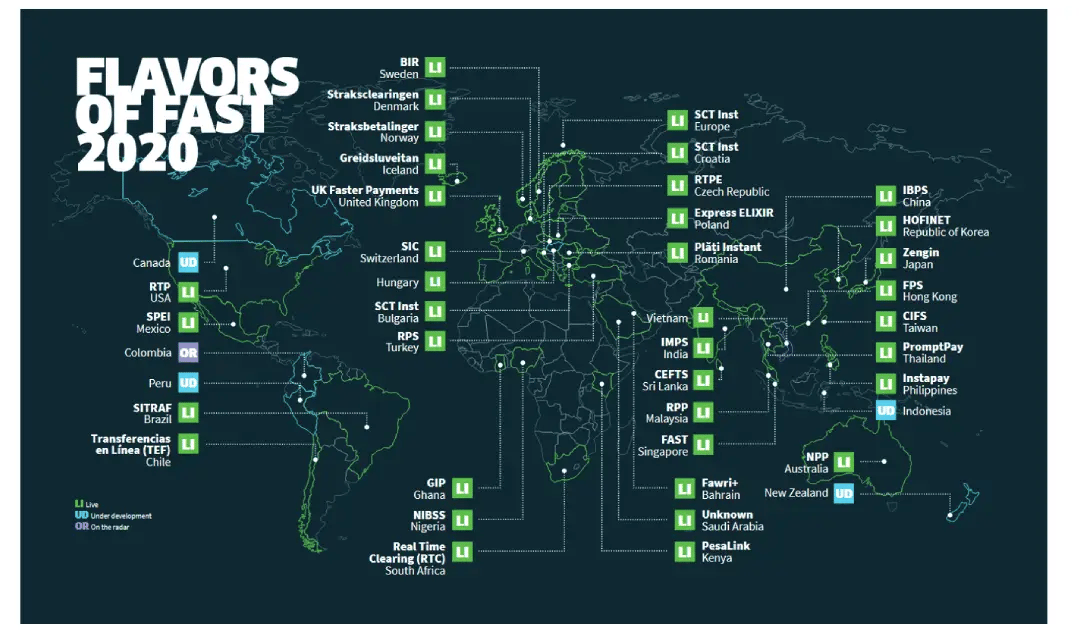

The biggest players in the real-time payments market

Countries with a sturdy digital payments infrastructure have contained the economic impact of the pandemic far more efficiently than

those without it.

There are 56 countries now live with real-time payments, and several more with systems under development and/or on the radar. In this section

we’ll look at a cross-section of the countries considered the biggest contenders.

Image source: FIS Flavors of Fast report 2020

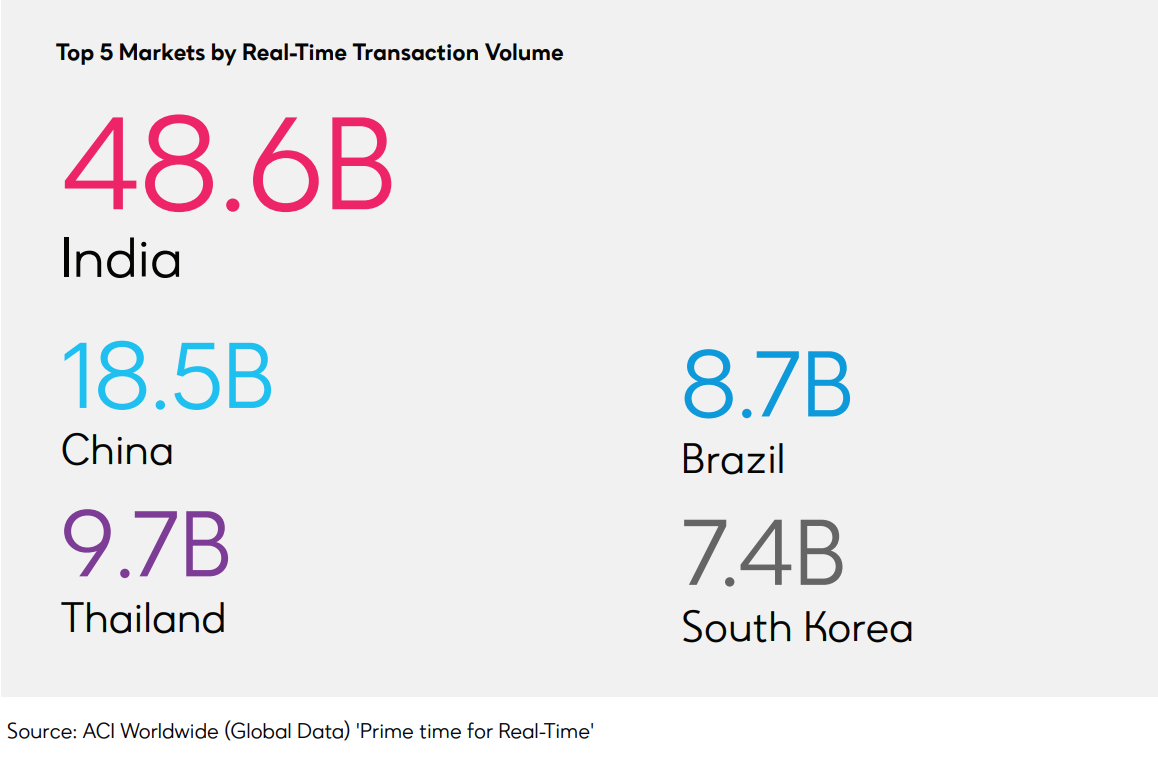

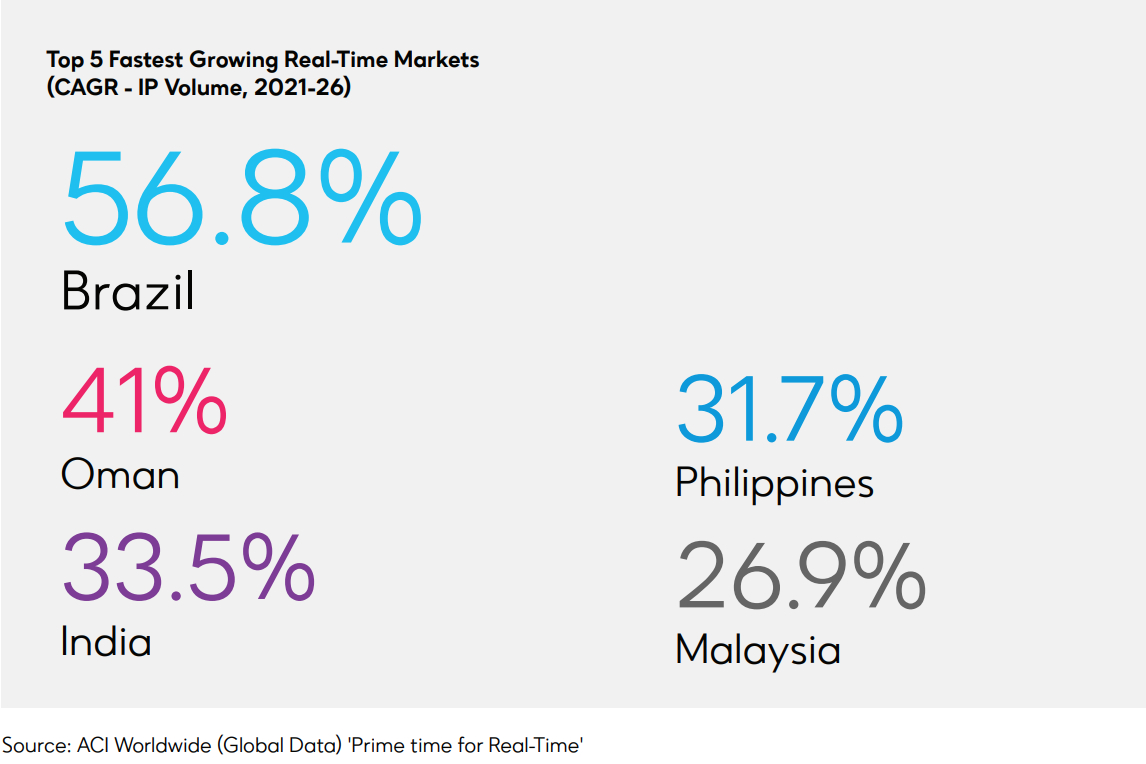

The graph below shows India leads the world as the largest real-time payments market, and financial experts predict most other markets will

follow. Initially, India’s growth came from low-value consumer payments, including P2P transfers and merchant payments, but this growth is expanding quickly into tax, bill and toll payments.

The statistics on the graph below show an overview of the Compound Annual (transactional) Growth Rate by the top 5 countries. The one thing that is clear about this research and analysis is the rate of growth is not slowing. Research shows that while P2P and C2B are driving most of the transaction growth, it’s B2B use cases that promise to drive high margin opportunities and higher values of transactions through real-time payments networks.

Spotlight on real-time payments by region

Although some markets are moving faster than others, the clear trend is a worldwide movement towards mobile and digital dominating the consumer payments mix. Mobile wallets and application orchestrated direct access to accounts are forming a large part of the customer experience. Let’s look at the payments modernization journeys of some key markets.

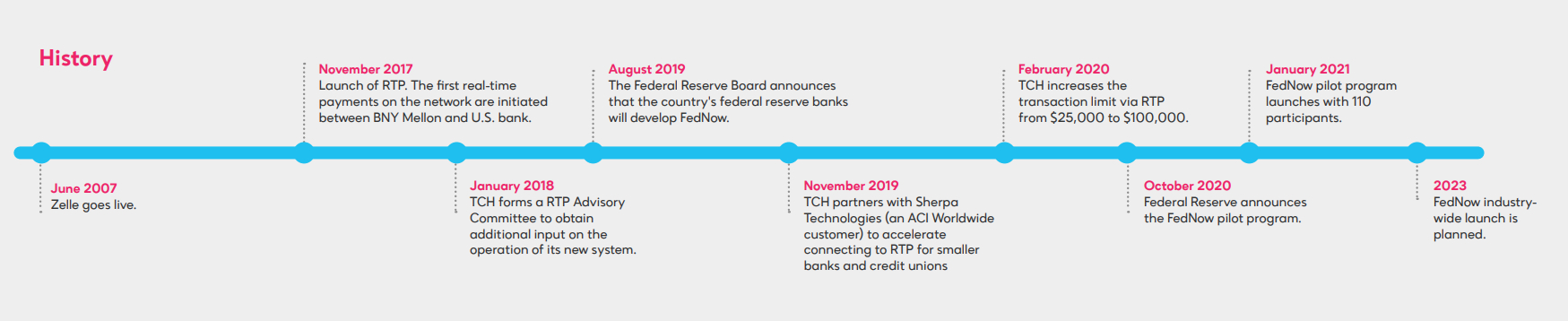

United States

A highly disparate financial landscape and firm rooted consumer payment habits are key reasons real-time payment processes have been relatively slow to take off in the U.S.

However, influenced by the COVID-19 pandemic, there has been a huge uptake and the real-time payments share of all transactions doubled in 2020.

While volumes are still small compared to other payment methods, the forecast for 2020-2025 is for a CAGR of 43.4% - or $6.2 billion.

Until recently, cash and checks firmly remained preferred payments preferences in the U.S., but finally, consumers, businesses and governments are breaking through and embracing digital.

Payments schemes

Real-time payments may have been slower to take off in the U.S. than in other technologically and culturally similar countries, but now they have two schemes live, and another in pilot. This means the U.S will see significant, rapid adoption of real-time payments.

Zelle – Offered by over 750 financial institutions across the U.S., supports individual and business accounts. Funds can be transferred using the Zelle app, participating bank or credit union apps or online banking services.

The Clearing House – A real-time payments network with 24/7/365 access that allows P2P, B2B, B2C, C2B, C2G and G2C payments.

FedNow – A pilot payments scheme due to be launched by the Federal Reserve, The FedNow Service represents an expansive, tech-enabled leap forward, allowing instant transfers any time on any day. While there are 5 banks and 3 credit unions currently testing the program, it is expected to be fully launched in 2023.

Asia Pacific

Asia is one of the most advanced digital payments markets globally, with governments and central infrastructures already many years ahead in digital and real-time payment developments.

When the pandemic forced dramatic worldwide changes in their financial ecosystems, Asia already

had infrastructures in place, unlike many other regions.

The shift towards real-time payments has been dramatically accelerated by changing payment necessities and preferences caused by COVID-19.

Almost a third (30%) of consumers in Southeast Asia have experienced reduced usage of traditional payment methods such as cash, credit cards and debit cards since the onset of Covid-19. As a result, over half (53%) are now using real-time payments more frequently than they were before the pandemic.

Payments Schemes

Malaysia - real-time payments network boasts a robust infrastructure and numerous supporting banks, payment service providers and merchants. DuitNow enables users to transfer funds instantly with a mobile number, national ID card number or other proxy options. It was launched in 2018 by Payments Network Malaysia (PayNet), powered by ACI Worldwide.

Singapore - PayNow, is a peer-to-peer (P2P) instant fund transfer service built on the FAST infrastructure that allows users to transfer funds from one bank account to another using various proxy options such as a mobile number or national ID card number.

Thailand - PromptPay launched in 2016 as part of its national e-Payment initiative. First created to deliver government welfare disbursements, it has rapidly expanded among consumers and businesses.

Indonesia – While still in the developmental stages, Bank Indonesia plans to launch its BI-FAST real-time system as part of the country’s 2025 Payment System Vision.

Integration and harmonized connectivity within SEA

There is a clear trend towards seamless integration and harmonized connectivity with the major SEA markets. This vision for a region-wide, seamless, and interoperable payments ecosystem is looking more achievable, and leading countries in the region are becoming more unified on their technology strategies, and the expert vendor partners that can deliver them.

At first look, the Asian regional market appears too complex cross-border, real-time ecosystems, and the full integration of cloud infrastructures. There is no single currency, no unified regulatory environment, and no formal alignment on economic priorities.

Yet, the Asian regional market remains unencumbered by the legacy payment systems that can impede innovation in mature markets, SEA countries are ideally placed to leverage their robust domestic central payment infrastructures as the foundations for cross-border linkages - an important catalyst for growth and trade.

With a combined population of almost 680 million, this will become dramatically more appealing to the region’s larger individual markets - China, Japan and South Korea.

China

Digital payments are almost a habit in China, with a strong consumer acceptance of mobile wallet partnerships and government initiatives encouraging banks to get involved. So, it might be surprising to some that China’s real-time payments growth was not as aggressive as anticipated in 2020, although the number of institutions offering these payments did see growth in 2020. The expected CAGR over five years is 13.5%, with 29.7 billion real-time transactions predicted for the year 2025.

Reasons for the slower uptake of real-time payments include the domination of the Chinese payments ecosystem by e-wallets like WePay and AliPay.

Also, the country’s digital transformation initiatives have come at a cost to much of the population who lack access to digital services, especially the elderly. This is partly the reason why there remains official government support for the use of cash in China.

Payment Schemes

China’s real-time payments scheme is the Internet Banking Payment System (IBPS)launched in 2010 by the People’s Bank of China (PBC). IBPS offers two types of real-time payments (single instance and recurring), two initiation methods (bank account and/or mobile number) and currently has nearly 350 participants. IBPS is often used to fund e-wallet accounts, that are then used to make the actual payment, so this could also account for the lag in the move to real-time payments.

Hong Kong

The major payment methods in Hong Kong remain Octopus (a reusable contactless stored value card) and credit cards. However, real-time payments surged in popularity in 2020, and by 2025, they are expected to make up over 10% of all electronic payments.

Developments in Hong Kong include Hong Kong Monetary Authority (HKMA)’s plans to expand real-time payments to the Greater Bay Area to improve fund transfers between Hong Kong and mainland China.

Payment Schemes

At its launch, the Faster Payment System (FPS), which supports HKD and RMB currency, was primarily utilized for C2B and P2P payments. At the start of 2019, the average monthly volume of real-time payment transactions was around 3.6M. In 2020, that figure leapt to around 10M and continues to grow.

United Kingdom

The U.K. continues to be one of the world’s leading markets for the modernization of payments systems. Real-time payments have been available

in the U.K. since 2008, and growth has been steadily accelerating, with an expected five-year CAGR of 11.6%.

Mobile wallet usage grew in 2020, and a decline in paper-based payment was sharp, although the country has been trending in that direction for years.

Payment Schemes

The U.K.’s New Payments Architecture (NPA) will enter its build-and-test phase in 2021, with a full rollout planned over the next few years. NPA will replace FPS and include an upgrade to ISO 20022. This new standard will provide many benefits including richer data, greater transparency and frictionless activity for participants and end-users. Additionally, it should also reduce friction and increase the speed of cross-border transfers.

Now is the time for real-time

Real-time payments are revolutionizing global commerce and changing the world's financial landscape, and it's happening now.

Consumers want it, businesses want it – and they’re willing to pay for instant access to funds in an account, in order to get paid more quickly. Speed, choice, and control are driving real time transactions in today’s rapidly changing world.

While real-time payments are still establishing their hold in many countries, dozens of real-time schemes are rapidly being established around

the world, and experts say they are set to at least double over the next year.

Now is the time to consider how you will manage real-time payments to ensure overall payment health, to deliver results that drive optimal business outcomes.