.png?width=141&height=141&name=Transact%20(1).png)

Since the onset of the COVID-19 pandemic, the digital payments market has burgeoned, and the payments industry is experiencing increasing pressure due to the influx of new and emerging technologies. In a changing world influenced by external drivers and shifting consumer behavior, expectations of omni-commerce is emerging at lightning speed.

Some of the statistics relating to digital payments show a growth that doesn't look like slowing down any time soon.

- Total transaction value in the Digital Payments segment is projected to reach US$6,752,388m in 2021.

- Total transaction value is expected to show an annual growth rate (CAGR 2021-2025) of 12.24% resulting in a projected total amount of US$10,715,390m by 2025.

- The market's largest segment is Digital Commerce with a projected total transaction value of US$4,176,874m in 2021.

- From a global comparison perspective it is shown that the highest cumulated transaction value is reached in China (US$2,892,494m in 2021).

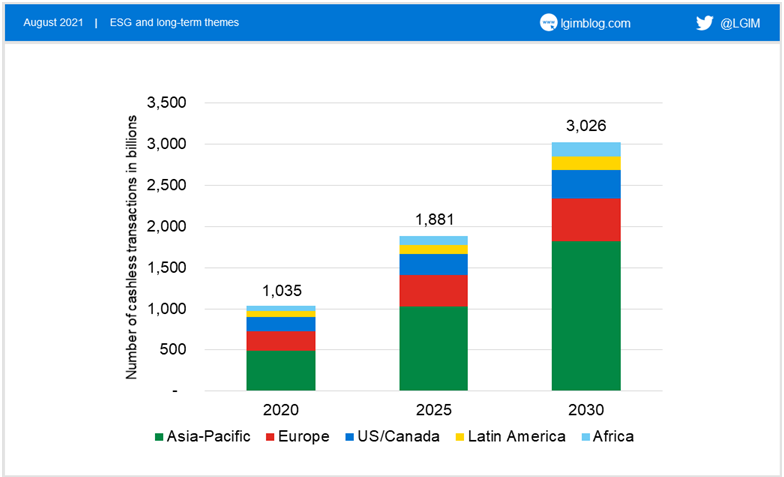

Image source: The LGIM blog

A cashless society?

Another highlight of the economic effects of the pandemic is the 'war on cash' vs 'cash is king' debate, and the move to make India and other countries cashless economies. There is a general trend among policymakers worldwide to move the economies of the world to a digital and information-driven paradigm.

The emphasis on digital payments and the digitization of commerce, however, has implications for individuals, small business, large enterprises and governments.

'Cash possesses unique attributes, which are mostly unmatched by alternative payment instruments. Cash also generates benefits for society that are not directly linked to its payments function'

While some of the banks and other institutions in more developed economies implemented a cashless payment infrastructure based primarily on credit cards several decades ago, those legacy structures are now becoming outdated and difficult to manage with the widespread adoption of digital technology.

When it comes to global payments, the 'Western' markets are now much slower to adopt new digital payments solutions than growing economies like China, India, or Eastern Europe. A large proportion of the population in developing economies of Asia, Africa, and Latin America has also been behind in adopting digital technologies for their global payments. But now, with the rise of mobile payment and digital wallets, these economies are now coming to rely on accessible mobile technology.

It's important to understand what digital payments are, how they work, and how they benefit the global economy as well as the associated problems that accrue from using these types of transactions and commercial dealings.

Defining digital payments

A digital payment, sometimes called an electronic payment, is the transfer of value from one payment account such as a bank account to another. A digital payment is made using payment processing software, and a digital device such as a mobile phone, POS (Point of Sales) or computer, digital channel communications such as mobile wireless data or SWIFT (Society for the Worldwide Interbank Financial Telecommunication).

Digital payment methods include bank transfers, wire transfers, cross border payments, mobile payments such as digital wallets like Apple Pay, and contactless payments using payment cards like credit, debit and prepaid cards.

It's difficult to create a universal definition of digital payments because digital payments can be partially digital, primarily digital, or fully digital.

For example, with a partially digital payment, both payer and payee use cash via third party agents, with providers making digital bank transfers in the back end. A primarily digital payment might be one in which the payer initiates a digital payment to an agent who receives it digitally, but the payee receives the payment in cash from that agent.

The benefits of digital payments

In the world of global payments, digital payments methods offer significant benefits to individuals, companies, governments, or international development organizations. The benefits of going digital include:

Cost savings

The efficiency and speed that digital payments provide leads to huge cost savings. For example, a recent report by the Better Than Cash Alliance and the Inter-American Development Bank shows that the Government of Peru could save US$96 million by shifting all government payments to more efficient digital options currently available in the market.

Financial inclusion

Digital payments are of great benefit to the world economy by increasing access to a range of financial services, including savings accounts, credit and insurance products. For example, in a densely-populated nation like India, it's not possible for banks to be omnipresent, or for traditional bank accounts to sufficiently cater to the needs of all the people. This is where digital payments can prove to be a great way to provide financial services to the far-flung.

Transparency and security

Security concerns can be addressed with digital solutions. Digital payments enhance traceability and accountability, reducing corruption and theft as a result. Secure digital payments also ensure a greater degree of transparency and accountability. Although cash has been used for centuries, there is little transparency in its usage. Further, it can be a complex task to keep track of your cash transactions, leaving you vulnerable against theft and losses.

Secure digital payments through a reliable digital payment system ensure that transactions can easily be traced. Similarly, secure gateways are harder to tamper with, thereby providing an extra layer of security.

Convenience and ease of use

The convenience that digital payments offer is another major benefit. Individuals and organizations want immediate payment solutions and quick confirmation messages. The advent of secure digital transactions provides this and more.

Modern-day digital payments have become so efficient that they're completed within a matter of seconds. Further, digital payment transactions are highly secure, which ensures that with electronic payments, the payment process provides security and peace of mind.

Lower costs of transactions

Secure digital payments systems can also help all stakeholders keep transaction costs to a minimum. This happens because these systems are protected against unauthorized access. As each digital payment method evolves and becomes more efficient, transaction costs are likely to reduce even further. This could prove to be a major benefit for consumers and merchants, as well as financial institutions.

The resilience or reliability of digital solutions and infrastructure is equally crucial. System outages might unreasonably prevent users from accessing their funds, therefore, it is imperative that providers keeping funds safe – that robust steps are taken to ensure network reliability and system capacity, as well as a payments channel secure from fraud, hacking, and any other form of unauthorized use.

Innovations and technology driving the digital payments sector

The pace of digital innovation is resulting in new business models and a more competitive environment as new players emerge. These are some of the innovations:

Contactless payments

Contactless payments are made possible using a credit, debit or smartcard enabled by Radiofrequency Identification (RFID) or near-field communication (NFC). This allows speed and a seamless experience using mobile money, and is being rapidly picked up in the U.S.

Open Application Programming Interfaces (API)

A publicly available API that provides developers with programmatic access to a proprietary software application or web service. Open APIs allow new providers to build services on top of existing infrastructure. This lowers barriers to entry for new financial technology players, encouraging innovation and enabling the rise of seamless digital payments services for the end-user.

Distributed ledger technology (DLT)

A database that is shared and synchronized across multiple sites, institutions or geographies. This database architecture solves the problem of trust among multiple stakeholders and the so-called “double spend”, which refers to the dilemma of ensuring a digital asset is not spent twice. Since all members of the network hold a copy of the ledger at all times, DLT allows for decentralized digital payment systems that do not rely on a single central authority, such as traditional banks, or a public institution.

QR codes

Since the onset of COVID-19, QR codes have gained widespread usage. A two-dimensional Quick Response bar code or square-shaped code that contains data is a quick and easy way to exchange information and has the potential of substantially reducing payment acceptance costs. Payment is made with a digital device and a camera linked to an account.

Biometric Payments

Biometric digital payments use Biometric ID as a means of verification and authorization of payments. Biometric ID is any means by which a person can be uniquely identified by evaluating one or more distinguishing biological traits. Unique identifiers include fingerprints, hand geometry, earlobe geometry, retina and iris patterns, voice waves, DNA, and signatures.

Central Bank Digital Currencies (CBDC)

Globally, emerging market economies are moving from conceptual research to intensive practical development. Central banks representing a fifth of the world’s population say they are likely to issue the first CBDCs in the next few years.

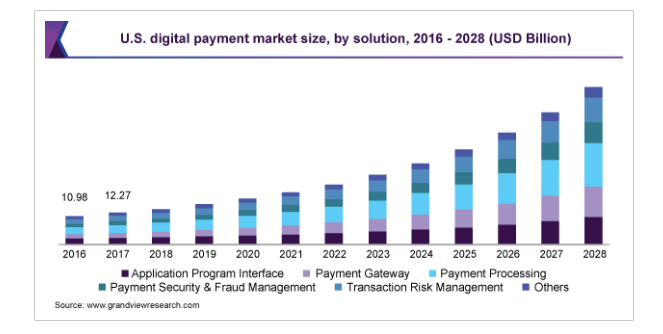

Below is a graph showing historical and projected data of the U.S. digital payment market size by solution.

Image source: Grandview research

The importance of payment analytics

The digital payments process is complex machine with many components. As with all machinery, the more components, the greater the chance of an operational glitch. This is why full visibility into your payments environment is crucial

Payments transactions pass through numerous application stages – or ‘hops’ – before they’re completed. They move from an ATM, POS, mobile or internet banking application through a complex processing environment. This consists of data centers, multiple switch servers, several backend databases and sometimes third-party services like Visa and Mastercard.

Read our comprehensive guide to managing your changing payments environment here

As the global economy changes, and digital banking solutions increase in complexity, payments infrastructures rely more and more on technology, so too does the importance of monitoring transactions. But it's not just monitoring, but analyzing payment data that enables a business, bank, or other financial institutions to keep on top of problems and guarantee the safe, seamless completion of transactions.

Full visibility into these complex payments systems means you can see where payments are being processed successfully, or where transactions are being declined. Data such as request and response timings, transaction dollar values, error codes and network address information needs to be clearly visible to investigate where and when a problem occurred, so that you can quickly determine why issues happen and how to resolve them.

One important consideration, however, is making sure that your monitoring solutions don’t impact the ability to run your payments system at full efficiency. This usually won’t be an issue during non-peak times, but it could impact your payments system during peak times or when the system is under full load.

Read more on the role of wholesale payments in the global financial landscape here

IR's Transact suite of payments solutions

IR's Transact suite of solutions, built on the powerful Prognosis platform, simplify the complexity of managing modern payments ecosystems. Transact brings real-time visibility, more control and better access to your entire payments environment, helping streamline the digital payments experience, turning data into intelligence, and assuring the payments that keep you in business.

Businesses can gain unlimited access and insights into customer usage data, end-to-end transaction performance metrics, and with dynamic visualization tools, businesses easily get a clear view of all this information to make proactive management decisions. With Transact as part of your payments solutions, the benefits are many.

Earlier this year, at IR, we extended our partnership with ACI Wordwide to enrich omni-channel payment analytics capabilities that are part of the ACI Omni-Commerce solution.

In the evolving world of digital payments, IR Transact brings real-time visibility to your entire payments environment, unlocking unparalleled insights into transactions and trends, streamlining the payments experience, from end-to-end.