With new players emerging in the world of payments, along with rapidly changing customer demands, the pressure is on to collaborate and develop faster, more efficient, innovative and transparent cross border payment solutions.

Business models are changing, and the process of international remittance payments is undergoing a much anticipated overhaul that will affect payment providers, and all the various entities involved in international trade.

In this guide, we'll look at:

- The challenges currently facing financial institutions, payment recipients and other relevant international organisations in the cross border transaction process.

- The trends that are influencing emerging changes in the cross border payments landscape.

- What it takes to transfer funds from one bank account to another from different perspectives including Business to Consumer (B2C), Business to Business (B2B).

- How cross border payments work today and the widespread benefits of delivering changes that will enhance cross border payments efficiency.

Enhancing cross-border payments has been a priority for the G20 for a number of years. In October 2022 they released a progress report on their roadmap, indicating the advancements made since announcing their focus in 2020.

Download our guide to managing your changing payments environment

What are cross border payments?

Cross-border payments refer to transactions involving individuals, companies, banks or settlement institutions operating in at least two different countries and are international transactions. These payments are inclusive of retail and wholesale transactions. Experts predict that global cross border payment flows are expected to reach US$156 trillion by 2022.

The cross border payments market has always been fraught with pain points and inefficiencies from both a cost and time perspective, resulting in expensive transaction fees and complicated, lengthy payment processing methods.

The global move to improve cross border payments strategies will see businesses achieving a better ROI and gaining more control over international payments and payment security.

Cross border payment challenges

Cross border payments are at the core of international finance and economic activity. However, this is in direct conflict with four long-standing key challenges that face cross border transactions:

- High costs

- Low speed

- Limited access

- Lack of complete transparency.

Enhancing cross border payments by making them faster, cheaper, more transparent and inclusive would have widespread benefits for supporting economic growth, global trade, development and financial inclusion. But delivering change is a slow process, and practical implementation of new competitive cross border payment strategies across all countries requires worldwide cooperation.

The trusted and tested correspondent banking approach has encountered challenges from emerging alternative solutions, and new players are making huge waves across some of the cross border payment systems fundamentals.

The changing shape of cross border payments

There are several trends increasing the demand for a better global international payments system and intensifying the need for end users to have access to cross-border payment services as efficient and safe as comparable domestic payments services. As a result, innovative new business models and participants are emerging. First let's look at some of the growth-influencing trends.

Trend 1: Changing consumer demands

The increased pace of change in the cross border payments market is closely connected to rapidly changing consumer demands. Consumers are aware of the growing choices they have, and are less willing to pay for costly banking services. At the same time, they expect their international payments process to be fast, secure and intuitive. The increasing penetration of smartphones, and popularity of digital access points like alternative payments methods (APMs) for remittances, have created new demands that incumbents are struggling to meet. Alternative solution providers that offer faster, cheaper, and more transparent cross-border payment solutions can gain a competitive advantage over banks.

Trend 2: Increasing trade with emerging markets

As their share of international transactions increases, another major trend within cross border payments is the growing focus on emerging markets in Africa, Latin America, and Asia. Global cross border trade growth is being stimulated by initiatives like the African Continental Free Trade Area and China’s Belt and Road Initiative. In contrast, protectionist policies in developed markets, including Brexit and US trade tensions, are expected to slow growth.

Trend 3: Accessibility of mobile phones and ePayments

The increase in smart phone ownership across the world has given people almost limitless access to banking services and ePayment solutions, with mobile wallets showing significant, steady growth. Global mobile wallet usage in eCommerce is forecast to grow to around 52% in 2023 (Worldpay). This growth is increasing cross-border commerce volumes.

Other important factors influencing the growth of cross border payments include

- Manufacturers expanding supply chains across borders

- Cross border asset management and global investment flows

- Increasing international trade and e-commerce

- Migrants sending money via international remittances

How cross border payments work

International transactions are far more complex than transferring funds in a domestic payments situation. Often, multiple banks are involved in the transfer of funds from one country to another, attracting significant bank fees at each payment gateway. Also, exchange rates between different currencies and local taxes for each country are big considerations.

Some of the most common cross border payment methods include bank transfers, credit card payments and alternative payment methods such as previously mentioned, eWallets and mobile payments.

Bank transfers

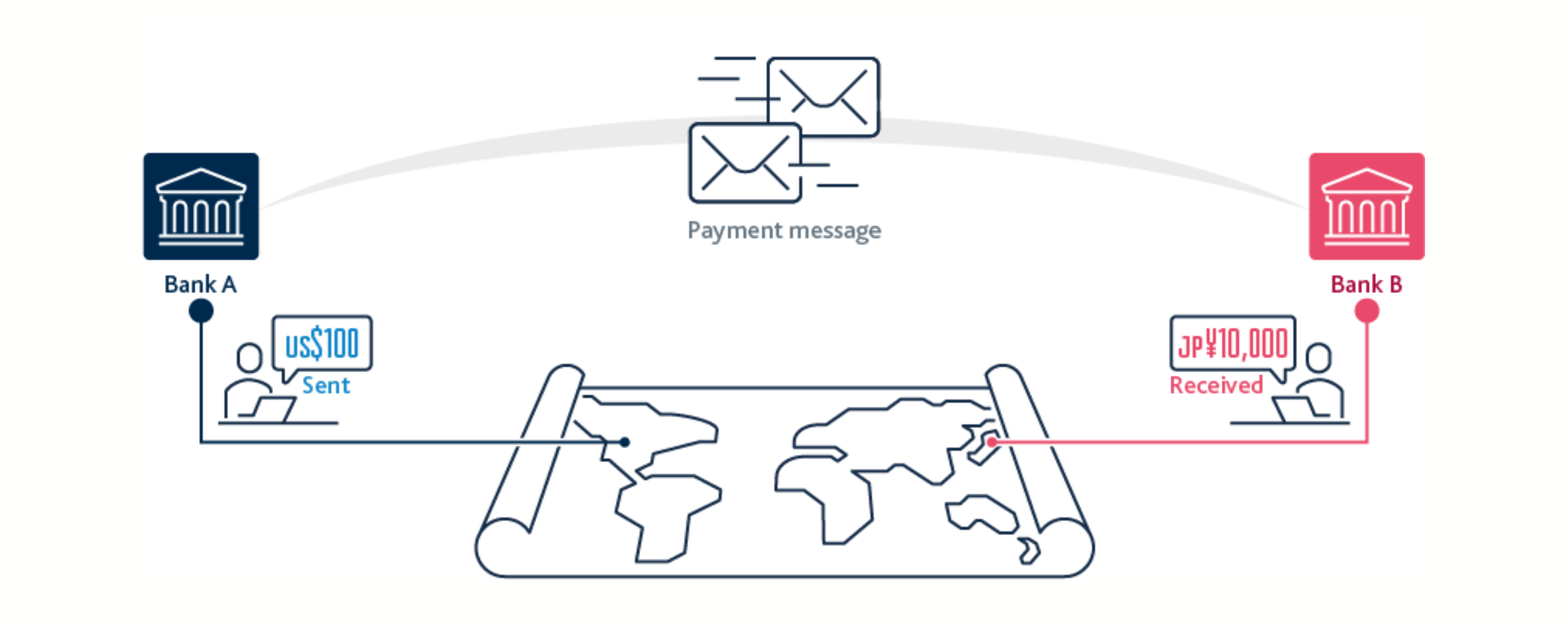

Also referred to as wire transfers, a simple cross border transaction using accounts held at each bank would involve a payment message sending an instruction to debit an account in Bank A and credit an account in Bank B.

Image source: Bank of England

Image source: Bank of England

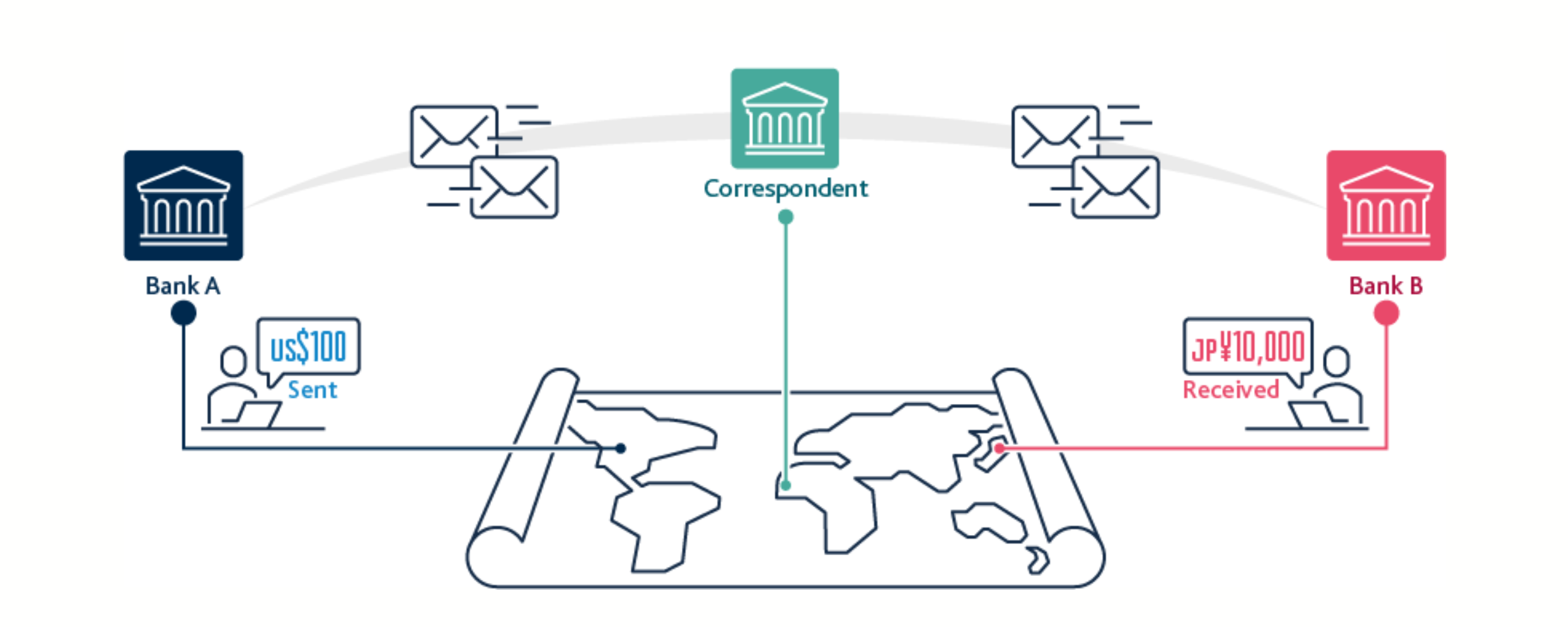

However, not all banks have a direct relationship with each other, so sometimes they need to transact via an intermediary, or a correspondent banking network. A correspondent bank provides accounts for Bank A and Bank B, enabling the transaction. The correspondent bank is an essential component of the global payment system for cross border transactions.

Image source: Bank of England

Image source: Bank of England

Credit card payments

Credit cards play a significant role in cross border payments, and are a preferred option for many consumers. From the consumer’s perspective, they simply enter their card details and wait for the transaction to be verified. Behind the scenes, as with any payment process in the global financial landscape, there is more going on. Cross border payments require more work from the involved credit card networks and acquiring banks as they need to convert between two different currencies. This additional workload results in extra fees that are passed down through the payment chain.

eWallets

Commonly available through apps for smart devices, eWallets like PayPal, Neteller, Alipay, Apple Pay and Google Pay allow users to safely store their payment cards of choice so they can pay for goods and services. Some eWallets support multiple currencies and the ability to place orders across borders. Although wallet to wallet transactions do not technically count as cross border transactions, they do help facilitate the transaction.

Types of cross border payments

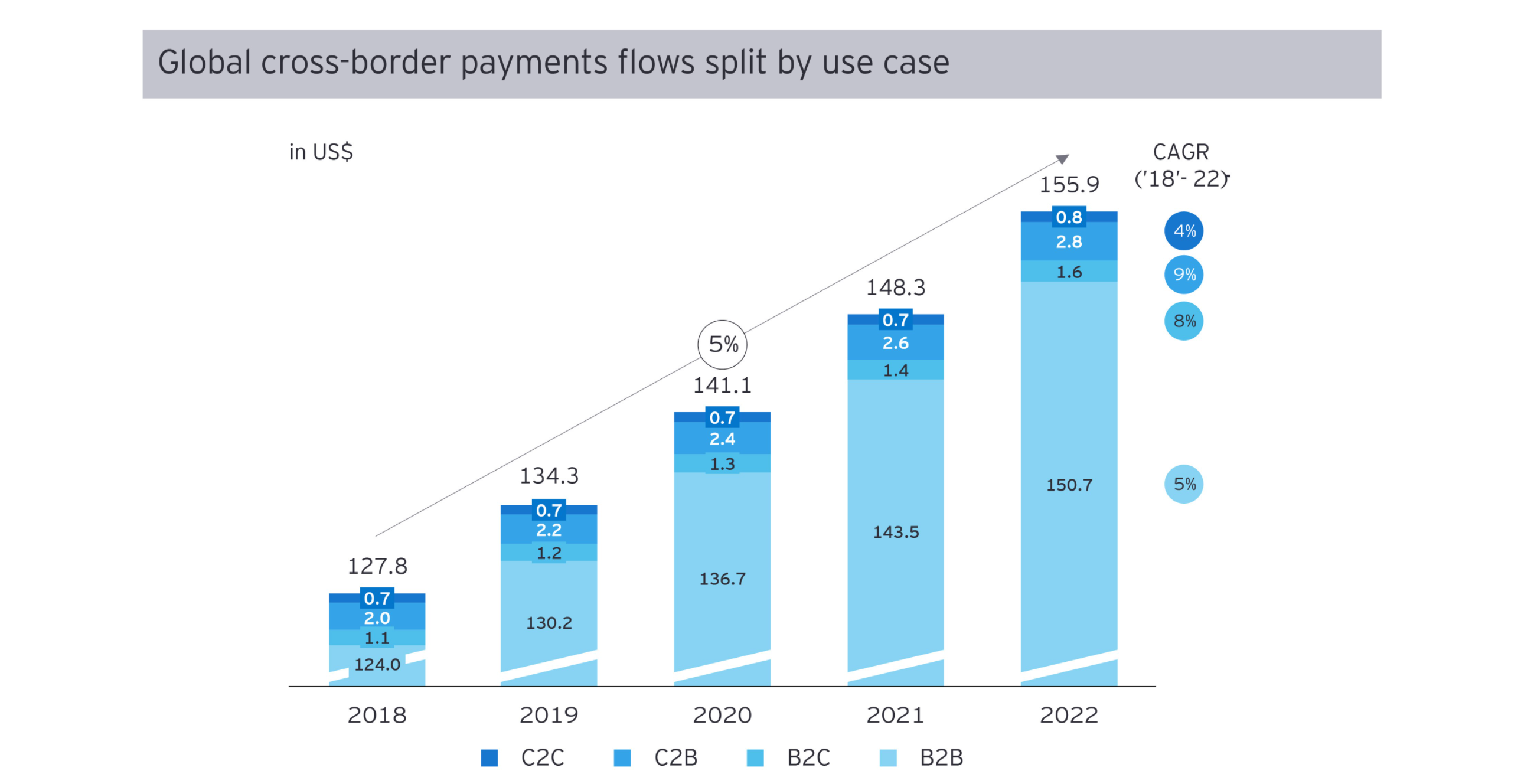

The size of the international payments market growing at a rate of 5% (CAGR) a year, with a transaction breakdown below:

- Business-to-Business B2B) transactions make up the largest share by far, expected to account for US$150t.

- Consumer-to-Business (C2B) transactions, such as cross border eCommerce and offline tourism spend, are forecast to reach US$2.8t.

- Business-to-Consumer (B2C) transactions, which include wage salaries or interest payments, are expected to amount to US$1.6t in 2022.

- Consumer-to-Consumer (C2C), or remittance payments, contribute the least – expected to reach US$0.8t in 2022.

Image source: EY

Image source: EY

International transfers can be categorized into two key sections:

Wholesale cross border payments

Wholesale payments are cross border transactions are typically between financial institutions, either to support their customers’ activities, or their own cross border activities (such as borrowing and lending, foreign exchange, and the trading of equity and debt, derivatives, commodities and securities).

Governments and larger non-financial companies also use wholesale cross border payments for larger transactions generated by the import and export of goods and services or trading in financial markets. You can find out more about wholesale payments here.

Retail cross border payments

These are typically between individuals and businesses. The key types are person-to-person, person-to-business and business-to-business. They include remittances, most notably money that migrants send back to their home countries.

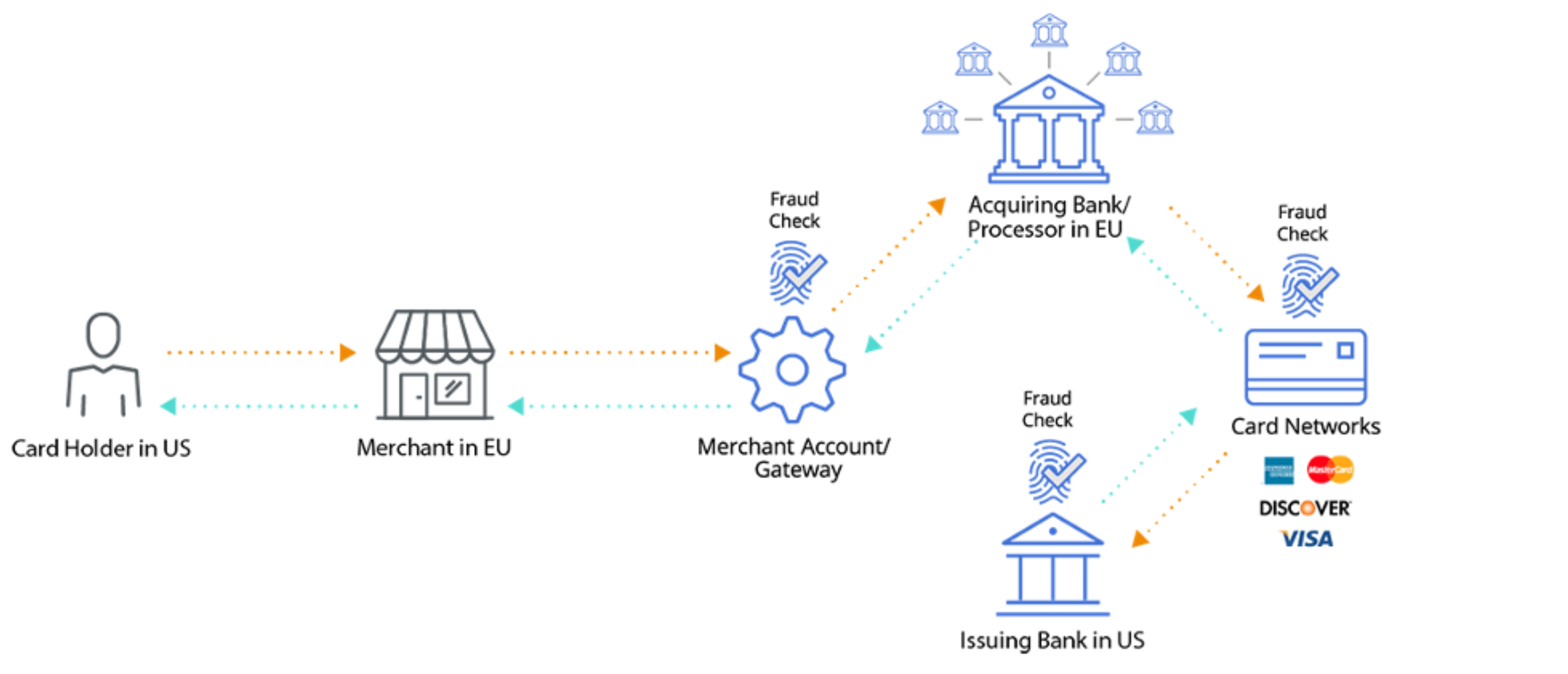

What is local acquiring?

eCommerce sellers are often faced with hefty fees that could be avoided with the right connections to local banks in each geography where they have a local presence. Local acquiring is when the seller’s acquiring bank and the shopper’s issuing bank are both in the same region or country. When the banks are in different regions, international transactions are more likely to be declined because of the higher rates of fraud in these types of transactions.

Image source: Bluesnap

Image source: Bluesnap

How cross border payments are changing

New entrants are challenging incumbents with innovative business models. Historically, banks have monopolized the cross border payments market. Dominant global correspondent banks faced little competition, so cross border transactions were subject to pain points for both private consumers and businesses, including a lack of transparency, long settlement periods, high transaction costs, and limited accessibility.

While these factors are less likely to be an issue for transactions within liquid currencies (e.g., USD/Euro), they are particularly prevalent in cross-border transactions of exotic currencies. For example, transaction fees from bank accounts held in France to bank accounts in Senegal could be more than 100€, depending on the transaction value - and could take up to seven days to settle. And even then, the sender would often not receive a confirmation of the transaction’s success.

According to The World Bank, the global average cost of sending $200 was 6.5% in the fourth quarter of 2020.

The rise of the cross border payments specialists

The urgent need to address the pain points, and improve cross border payments has made way for the arrival of two groups of new specialized players: Digitally-enabled money transfer operators and back-end networks.

Digitally-enabled money transfer operators

These specialists deal directly with senders – the consumer or merchant – and offer digital cross-border payments as their core business.

When working with liquid currency pairs (e.g., USD/EUR), these providers typically establish direct banking relationships and net payment flow between the sending and receiving countries. However, in many emerging markets, setting up an international bank account number can be challenging, with payment methods often fragmented and capital controls hindering payment outflows. Conditions in these countries means that digitally-enabled money transfer operators often rely on partners, such as back-end networks.

Back-end networks

These specialists typically do not have a direct relationship with the sending or receiving party, but instead partner with the bank or wallet providers of these parties. By establishing partner networks via direct connections with local banks and APMs in both liquid and non-liquid markets, back-end networks enable interoperability within cross-border payments. For example, a Paypal account can transfer a deposit in Euro to an M-Pesa account in Kenia Schilling. As this is not possible with CBNs, front-end providers are increasingly using these alternative back-end networks instead of using traditional bank rails.

How ISO20022 is enabling change

ISO 20022, first introduced in 2004, is an international standard for relaying electronic messages between financial institutions. It was created to give the financial industry a common platform for sending payments messages and exchanging payments data, using a central dictionary, a standard modelling methodology, and a series of Extensible Markup Language (XML) and Abstract Syntax Notation (ASN.1 ) protocols.

ISO 20022 was designed as a flexible framework providing an internationally agreed business message syntax, where user organizations and developers will use the same message structure, form and meaning to exchange transaction information globally.

Global adoption of ISO 20022 will create a common language and model for payments data. It will provide higher quality data which translates to better quality and faster payments for everyone involved in the payments chain. The implementation of ISO 20022 will create an open standard that can adapt to changing needs and new approaches within the payments industry. As it will not be controlled by a single interest, it can be used by anyone in the industry of financial services and implemented on any network.

Banks and financial organizations globally are set to transition their payment systems from SWIFT payments to the new, highly structured and data-rich ISO 20022 standard. By 2025 it will be the universal standard for high, or large-value payments systems of all reserve currencies, and will support 80% of transaction volumes - and 87% of transaction value globally. In Europe, SWIFT payments will transition earlier, with the European Central Bank announcing ISO 20022 go-live dates of November 2022 for the standard.

Find out more about ISO20022 in our comprehensive guide here

Change is happening fast

With the building blocks for change within cross border payment market infrastructures already in place, cross border payments innovations are resulting in eCommerce transactions that are faster and more transparent, efficient and secure than ever.

Removing cross border payment frictions between separate countries, international bodies and trade partners undoubtedly benefits all parties. Tailoring payment options and the payment experience to meet consumers’ expectations for speed and seamless engagement will drive sales. Supporting these payment solutions and their underpinning technologies and infrastructures across countries will be huge focus areas for merchants in the age of cross border eCommerce.

As cross border payments market grows in both volume and complexity, the need for interoperability is increasing. Many geographic borders are no longer as clearly defined, and markets have regrouped according to industry rather than geographic lines. Financial markets are adapting to reflect these changes by streamlining the way they accept payments.

The growth of cross border payment fraud

The latest issue of Global B2B Payments Playbook, a joint publication compiled by PYMNTS.com and Worldpay B2B Payments finds that 60% of US and UK businesses face cross border payments fraud. Since the advent of remote working, and the use of home networks and personal devices to conduct business, many businesses have struggled to rebuild their cyber security infrastructures. Fraudsters have taken advantage of this, and B2B theft and fraud is on the rise.

Favorite fraud methods

- Invoice fraud: This type of fraud occurs when cyber criminals prey on unsuspecting companies by posing as vendors, billing for work that was never performed. The money is then laundered after being redirected into overseas accounts. Victims are often unaware that they have been scammed until a legitimate supplier subsequently sends an invoice for the same work.

- Capital Scam: This type of fraud, targeting business leaders involves fraudsters impersonating insurance or investment companies, and requesting funds transfers as part of an investment commitment.

- Reshipping fraud: Items are purchased by cyber criminals with stolen credit cards or other stolen funds and are sent to U.S. consumers, who then repackage and ship the items overseas. The re-shippers are often found through bogus work-at-home scams, where they are offered jobs that they believe are legitimate employment positions but that actually involve mailing stolen items.

The importance of real-time payments analytics

A definitive report by Worldpay, on the art and science of global payments shows some interesting payment statistics and insights into world payment trends. Real-time payments analytics are vital to measure and analyze payment data, view growth and make decisions throughout the entire payments chain, and across each different platform including cross border payments. This is even more important now with the impending global ISO 20022 migration.

The power of data management

The power of data management and analytics comes from finding correlations between different points of data. This can help identify threats and fraud attempts. The ability to observe patterns within systems, and study related metrics, enables organizations to detect abnormalities within their systems. Analytics gives us access to a mixture of traditional payment data as well as insight into what's happening inside an organization's payment system. Combining data about how a system is working with ad hoc reports, gives better insights into transaction data.

IR Transact: Third-party monitoring solutions

Monitoring with an outboard, or third-party solution like IR Transact is non-intrusive, and integrates seamlessly into the existing enterprise environment, bringing real-time visibility to the entire payments ecosystem. It collects data from all silos across the payments system, filters, correlates and analyzes this information and brings it into a single application.

Keeping on top of emerging technologies, regulatory changes and the introduction of new international payments standards is challenging. With ISO 20022 migration imminent, turning information into intelligence will assure the safe, efficient operation of payments systems worldwide.

IR's High Value Payments solution

Trillions of dollars move through high value clearing systems around the world every day. These transactions play a critical role in the global economy, making the need for efficient, reliable processing paramount. When problems arise, it not only affects customer relationships and impacts revenue, but can lead to significant financial and regulatory penalties.

Part of IR's Transact payment solutions suite, is our High Value Payments product. This product has been purpose built to provide complete visibility across high value and high priority transactions.

The High Value Payments solution enables real-time insight into the health of high value transaction queues and the status of key accounts to ensure transactions get processed without issue. It enables organizations to:

- Leverage business data to gain visibility into critical accounts, such as settlement or high value customers.

- Easily monitor balance thresholds, flagged accounts, abnormal account usage patterns and project liquidity shortfalls.

- Monitor transaction queue health, volumes, and anomalies to get ahead of potential issues and ensure certain transactions are processed on time.

- View detailed, historical transaction information to investigate and identify the root cause of issues quickly.

“Our global customers are seeking new levels of insight and real-time analysis to help them ensure seamless payments experiences across all levels of the business, and we’re excited to expand our support to the high value payments space.”, David Guiver head of Transact products.