.png?width=141&height=141&name=Transact%20(1).png)

Payment processing services have come a long way since the days of simply cash or card payment.

Payment lifecycle is a process which involves various steps during a payment transaction when making digital payments. Just one technical fault with payment data, or a missed step along the payment channel can make your transaction vulnerable.

In this blog, we'll talk about the steps in the payment lifecycle to gain a better understanding of how money moves.

Find out how using payments data can give you unparalleled insights and simplify complexity in your payments systems.

A basic payment transaction involves:

A payer - Push Payments,

A payee - Pull Payments

How Online Payment Processing Works

From credit cards to technologies like digital wallets and real-time bank transfers, consumers these days have a multitude of choices when it comes to paying for goods online. Offering a range of locally preferred payment methods is important for businesses, and is a crucial part of delivering a great user experience.

Very simply, an issuing bank issues credit cards or debit cards to customers. Customers can then use these cards to purchase from a merchant. The merchant's bank, in turn, is the acquiring bank. And, the card networks (VISA, Mastercard, etc.) are the medium facilitating this entire process.

Making an online payment is an everyday part of life. The process probably seems simple to consumers as they shop, but there are a number of different steps that go on behind the scenes:

-

Buyer selects payment method at the checkout page (card payment, digital wallet, bank transfer)

-

Payment details are encrypted via a payment gateway and sent to the payment processor

-

The issuing bank is requested to authorise the payment to the acquiring bank

-

If there 's a sufficient balance, the transaction is approved by the customer’s card issuer, issuing bank or digital wallet

-

Funds are sent to the merchant bank, less the payment processing fees

Below is a very basic illustration of the payment process.

Image source: Rapayd

The image below depicts the complexity of the payment process in more detail, from a buyer's point of view.

Image source: PayZen

How do payments end up where they need to go?

Essentially, the card schemes (such as Mastercard and Visa) operate a giant digital ledger to ensure funds end up in the right place. Remember, they connecting participating issuers and acquiring banking players. At the end of the business day, merchants send their card transactions to their acquirer, either directly or via a payment gateway. The acquirer sends these on to the relevant card scheme.

The payment authentication and authorisation process

The completion of an online payment has two phases that validate a payer's credentials. Authentication and authorisation.

In online and mobile commerce today, the need for transaction authentication has never been greater. eCommerce spending globally reached $4.2 trillion in 2020, a growth of almost 28%. But losses from illegal purchases using stolen credit card numbers are growing almost as fast.

Image source: Corporate Finance Institute

Payment authentication and authorisation are the steps taken to of make sure a cardholder’s card number or other personal payment data from their account isn’t being used to make payments without their knowledge.

In short, payment authentication validates who a user or cardholder is, whereas payment authorization gives the user access to a specific resource or functionality.

Banks and card issuers, merchants, and payment processors typically use a combination of authentication factors to confirm a person's account details throughout the payment channel, such as:

-

Information unique to the person making the payment, for example, a password or PIN.

-

How you will pay, such as a debit/credit card, USB token, smartphone, etc.

-

A specific trait unique to a person, using advanced technological solutions like biometrics, retinal scans, voice recognition, etc.

Payment authentication methods

Choosing authentication methods and tools throughout the payment lifecycle depends on your business model as well as laws and regulations in a country or region - and the means to finance and implement technically advanced solutions. Here are some common payment authentication methods:

3D Secure

The 3D Secure protocol is one of the most widely used authentication methods for online payments across a payment network. The three domains (3D) refer to the authentication performed by:

-

The issuing bank (the consumer's card network).

-

Payment acquirers such as payment gateways, merchant plugins, and banks receiving the payment.

-

Directory servers, authentication history servers, and other interoperability solutions.

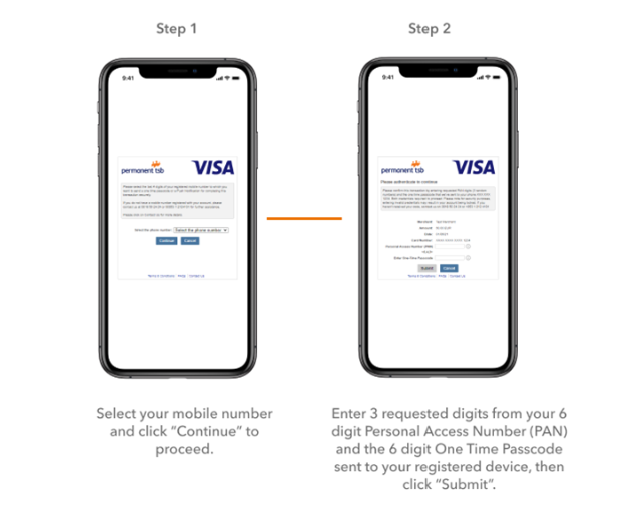

These three domains work together to cross-reference the data and get confirmation of the identity of a person through biometrics, or One Time Passwords (OTPs). The OTP is sent by the customer’s bank (or outsourced provider) using an SMS or Push notification. The notification is delivered to the phone number or email registered to the customer’s bank account.

Image source: Permanent TSB

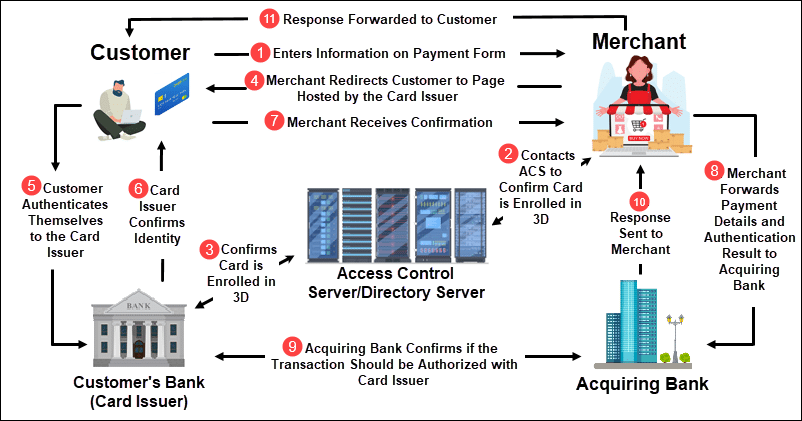

During a payment transaction, the merchant uses the authorisation process to obtain the approval from the buyer's financial institution on issuing the payment.

Image source: CCBill

Benefits of 3D Secure

3D Secure is the most efficient and safe ways to authenticate transactions, as the customer needs to have their card details and access to their mobile phone to complete the payment.

OTPs are valid only for a limited period and cannot be used for other transactions, meaning the merchant or merchant bank does not need to store or protect long term customer passwords.

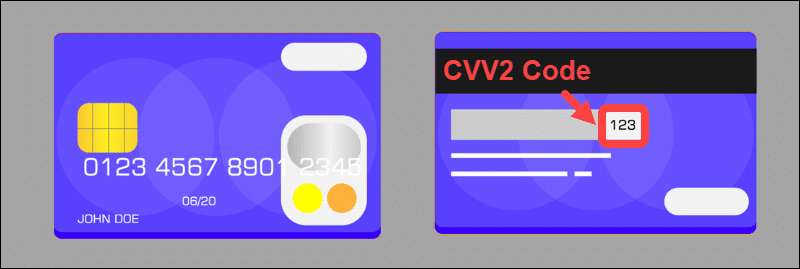

Card Verification Value (CVV)

The Card Verification Value method requires customers to enter their CVV code on a payment form.

The CVV code is a 3-digit or 4-digit code located on the back of a customer’s card, and only works in conjunction with other details from the same card.

Image source: CCBill

CVV2 is an advanced version of CVV with added security that makes it more difficult to guess the combination of digits. Larger credit card institutions have adopted the CVV2 standard.

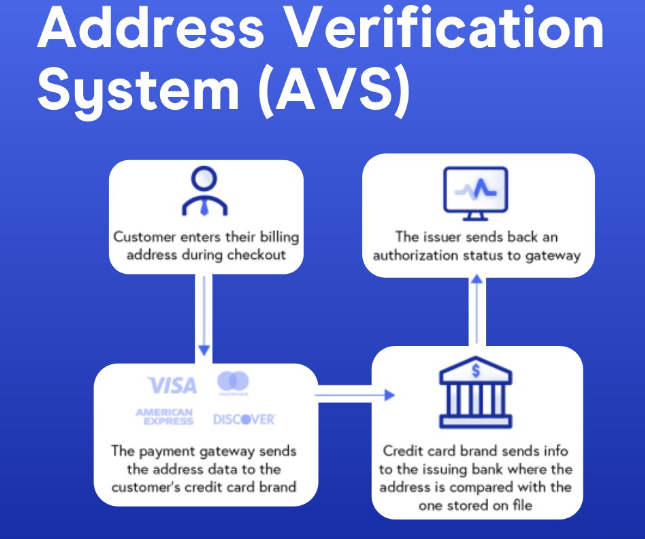

Address Verification Systems (AVS)

An AVS check compares the address a customer enters on the payment form with the address on file for the cardholder.

The AVS is useful as an indicator that there might be an issue with the transaction. Most non-face-to-face card payment processors use this method by default. Address checks focus on the numeric elements of the address, such as the ZIP/Postal code.

Image source: Ebizcharge

Payment reversals

There are basically two payment legs in the payment lifecycle. The actual payment (a forward leg that deals with the original payment) - and a reversal or chargeback (a backward leg that deals with associated refunds).

A payment reversal is also referred to as a "credit card reversal or "reversal payment", and happens when the funds a cardholder uses in transactions are returned to the cardholder’s bank for whatever reason.

Payment reversal type 1: Authorization reversal

Authorization reversals reverse the transaction before the payment transmits

The further a payment gets along the payment channel to completion and the more entities it communicates with (issuing banks, card issuers, etc.), the more difficult it is to take back.

If you notice something incorrect immediately after submitting the authorization request, you can ask your bank to stop the transaction from occurring. This process is highly preferable over a future chargeback or refund, as they are better for the customer, won't impact your real time payment data, and cost less in fees.

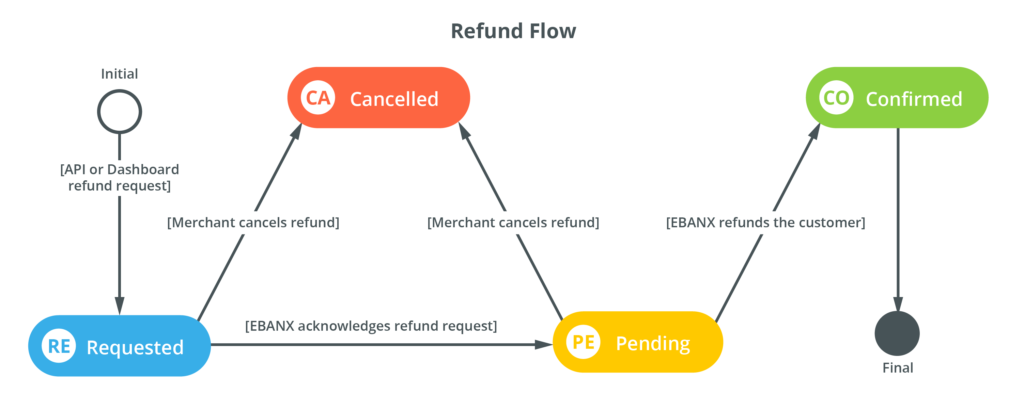

Payment reversal type 2: Refund

Refunds reverse a payment after the transaction has completed but before the customer has filed an official dispute, for example when something is wrong with the product or purchase and they contact your business to get their money back.

Instead of just canceling the transaction like an authorization request, a refund completes the transaction in reverse. In effect, the acquiring bank is now paying the cardholder instead of the other way around. It’s treated like a new, separate transaction.

Image source: ebankx

Payment reversal type 3: Chargeback

Chargebacks occur when customers call their bank and file a dispute against your transaction.

Not only do chargebacks constitute lost revenue on the product, the fees, the shipping, etc., but there are also extra, chargeback-specific fees. If you incur enough chargebacks, you may be flagged by the card networks and be unable to accept credit cards, creating a sustainability and reputational threat within each chargeback.

Image source: Vacationrentpayment

The importance of monitoring your payment network

Organizations are dealing with managing booming transaction volumes, the shift to cashless payments, new payment schemes and technologies, and higher customer expectations to remain successful in a competitive market.

It's vital that financial institutions and payments processors have advanced payment monitoring solutions in place to keep track of every payment process.

It's equally as important to leverage the data they have to provide real-time insights into the validity and status of all transactions. Payment analytics allow a business to take historical data and apply it to things that are happening to a business right now. This applies to sales and payment processing or any online services in the payment space.

Read our guide to real time payments analytics here

How IR Transact can help manage your payment lifecycle

With IR Transact, you can simplify the management of your payment lifecycle by using one tool to monitor and manage multiple vendor solutions, across on-premises and cloud deployment models. With over 24 million transactions managed daily, we can help you optimize your entire payments infrastructure. Here's just some of what our Transact payment solution can offer:

-

Real-time visibility of your transactions, no matter what vendor you’re using

-

Complete control of your payments ecosystem with dynamic thresholds and alerts

-

Reduced downtime and optimize service levels

-

Successful deployments and optimal performance across all payment types

-

Customizable dashboards to view the information most important to you

-

Translating complex data sets into straightforward, digestible representations

Find out how using payments data can give you unparalleled insights and simplify complexity in your payments systems.

Watch the webinar.