.png?width=141&height=141&name=Transact%20(1).png)

According to financial experts, the world's 1,000 year dependence on paper money may be coming to an end, with a real time alternative that provides a digital equivalent of physical cash by allowing people to pay for things instantaneously.

Real time payments are revolutionizing global commerce and changing the world's financial landscape, and it's happening now.

Interested to learn more about real-time payments? Download our eBook for more information.

What are real time payments?

Real-time payments, sometimes called instant or Immediate Payments (IP) are the ability to transfer funds between individuals, businesses and governments, making those funds available to the payee instantly, and with instant confirmation.

In 2020, a report by leader in worldwide payments, ACI Worldwide found India to be the dominant player in real time payments overtaking countries like China, South Korea, the UK, and the US. With 25.5 billion real-time payments transactions, India comfortably outpaced China's 15.7 billion.

The growth opportunities for the real time payment industry and the displacement it's causing worldwide is phenomenal. The global real-time payments market size was valued at US$10.64 billion in 2020. It’s expected to expand at a compound annual growth rate (CAGR) of 33.0% from 2021 to 2028.

Real-time payments offer faster payments, and a more consistent means of paying compared to some legacy methods, which could take days to reach a recipient. This newer, more seamless way to make financial transactions will affect consumers, businesses and world governments socially, culturally and economically.

COVID-19’s role in Real -Time Payments

Even before the COVID-19 pandemic, consumer-driven changes were happening in the payments world. But the pandemic accelerated the adoption of digital and real-time payments worldwide as a strategy to keep consumers safer and businesses operating.

The COVID pandemic led to a seismic shift in India's payments landscape, upending long-accepted payment behaviors. As social distancing became the norm, contactless payments and their real-time nature were a boon for payment issues faced by consumers.

COVID-19 has also driven consumers and businesses to question the use of cash. While there is no real evidence to support it, the WHO has recommended the use of contactless payments to reduce the chance of transmission. Some experts predict this is a trend that’s expected to continue towards what could mean an eventually cashless society.

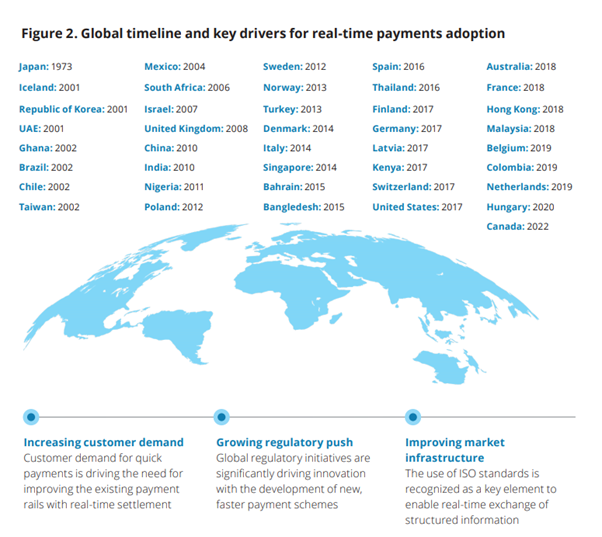

In 2015, only 14 countries had real time payments capability. Today, 56 nations have enabled real-time payments — still less than one-third of the world’s nations.

Source: DeLoitte Analysis

Source: DeLoitte Analysis

With financial markets around the world in differing levels of maturity, the uptake of real-time payments is facing some challenges.

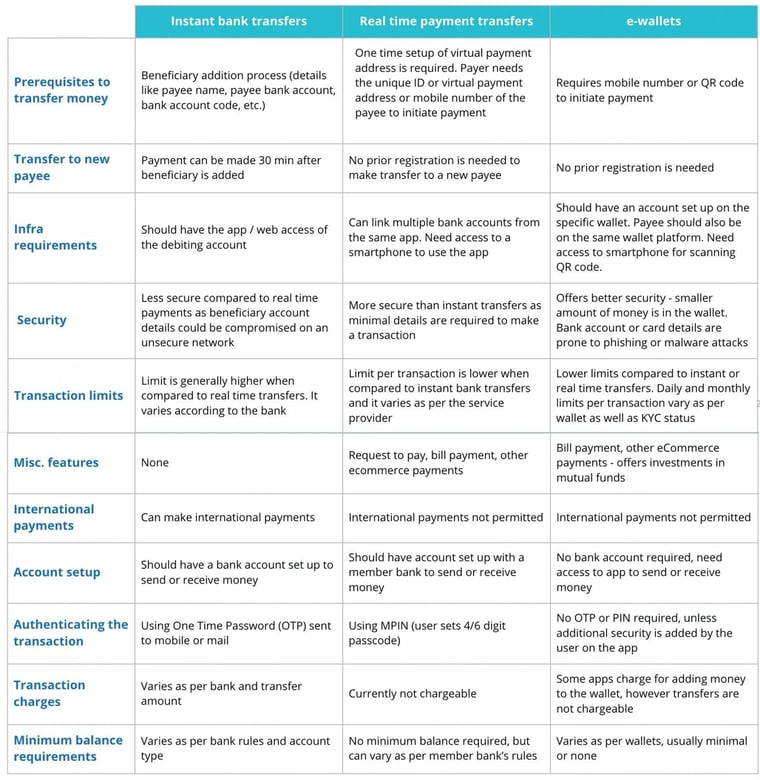

Types of real time payments

Primarily, there are three kinds of real time payments payment mechanisms:

- Instant bank transfers that use account numbers (the traditional approach)

- Real time payment (RTP) transfers from one bank account to another using an alias like a mobile number or a unique ID

- e-wallets

Below is a summary of their different features:

Image source: Thoughtworks

Image source: Thoughtworks

What is a Demand Deposit Account?

A demand deposit account (DDA) is an original form of real time payment, like a bank or checking account from which deposited funds can be withdrawn at any time, without advance notice. DDA accounts can pay interest on the deposited funds but aren’t required to.

"DDA" can also mean direct debit authorization, which is a withdrawal from an account for purchasing a good or service. It's what happens when you use a debit card. But it's fundamentally it's a real time payment concept; the money is immediately available, drawn on the linked account, for your use.

The reality of real-time payments

Although payments made with credit or debit cards, digital wallets, or P2P apps may seem like real-time payments, the funds transferred using these payment methods are not processed right away. Credit and debit card transactions go through a bank settlement process that can take up to 72 hours to clear and settle.

With real-time payments, there is no 'float,' which is the interval between when money leaves a payer’s account and becomes available in the receiver’s account. Payments can be made 24 hours a day, 365 days a year—and the funds are available immediately.

And digital wallet transactions, like Zelle, are not true real-time payments because they are non-bank money transfers that occur between personal wallet accounts, not bank accounts. Online transactions made through the clearing house payments company or Automated Clearing House (ACH) system can process same-day and next-day payments. However, payments are cleared in batches, which means that funds are not available until the settlement process is complete and the payments clear.

According to Mark Ranta, payments practice lead at Alacriti, ‘Although unseen and unnoticed, that time lag matters a lot. The lack of real-time money movement actually ends up making things a lot more expensive.’

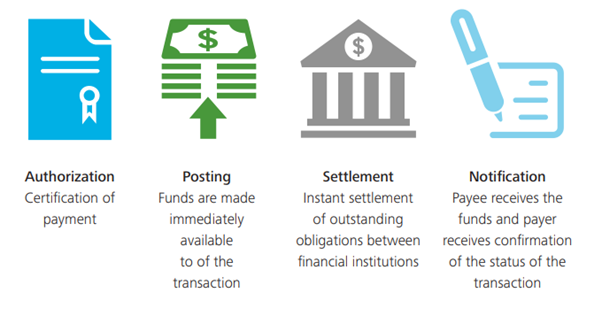

The benefits of real-time payments

Real-time payment systems offer instant, 24/7 secure interbank electronic funds transfers that can be initiated through smart phones, tablets, digital wallets and on the internet.

Source: DeLoitte

Source: DeLoitte

As well as faster payments, real time payments offer a great deal of benefits for financial institutions, including:

- Boosting revenue through increased customer spending

- Reduced payment costs, providing higher value services to consumers

- The engagement of new consumer segments

- The reduction of fraud and risk management

- Improving long term customer relationships

- Enabling innovative new product offerings to stay competitive

Real time payments can also help businesses to strengthen cash flows and subsequently improve operational efficiencies, budgeting, and overall cash management.

This growing preference for efficient real time payments among businesses is predicted to drive the market growth. In fact, a survey conducted by ACI Worldwide revealed that 77% of merchants worldwide are expecting real-time payments to replace physical payment cards.

Who can use real time payments?

Consumers, businesses, and government entities can use the RTP network. The technology for RTP transactions was designed to facilitate faster payments across all payment categories, including:

- Business-to-business (B2B)

- Business-to-consumer (B2C)

- Consumer-to-business (C2B)

- Peer-to-peer (P2P)

- Government-to-citizen (G2C)

- Account-to-account (A2A)

The growth of faster payments platforms in the U.S.

As more and more businesses, consumers, and municipalities embrace digital payment methods, financial institutions all across the U.S. are utilizing the RTP network’s capabilities to create faster and safer payment processing services.

The FedNow service (FedNowSM) is another real-time payment and settlement service created by the Federal Reserve Banks that will incorporate clearing house functionality into the process of settling payments. This functionality enables banks and financial institutions to exchange the debit and credit information needed to process payments and notify customers whether the payments were successful. FedNow is expected to go live in 2023 or 2024.

The challenges of RTP for financial institutions

Before the benefits of real-time payments can be universally recognized, there’s work to be done. Financial institutions and infrastructures need standardization and interoperability to expand their RTP network, along with a cost-effective flexible interface that fully supports technology re-use.

While Payments Market Infrastructures (PMIs) are being built to make real-time payments possible, banks are being forced to restructure their business models. They must deal with obligations to their domestic customers to provide round-the-clock payments, as well as managing the multiple payments schemes worldwide, and combating the risk of fraud.

Building a solid RTP network capability is challenging in itself, but significantly increased with legacy infrastructures and existing system or operational constraints.

To truly capitalize on the opportunity of real-time payments, each country’s payments ecosystem must closely monitor its development and start planning for the future accordingly. The best way to do that successfully is to have access to the relevant data.

ISO20022 and real time payments

In November 2022, banks will be mandated to transition to the ISO 20022 messaging standard to fix issues with infrastructure, compliance, and customer experience.

This will, in turn, provide an interoperable standard for financial data exchange and at the same time, streamline payments and reconciliation. This will be of great benefit to the growing number of real-time payment networks already citing ISO 20022 as their standard.

It has already prompted a larger number of financial institutions to re-engineer their real time payment rails to connect with each other, improving efficiency for instant payments, cross border payments and paving the way for enhanced real-time domestic networks.

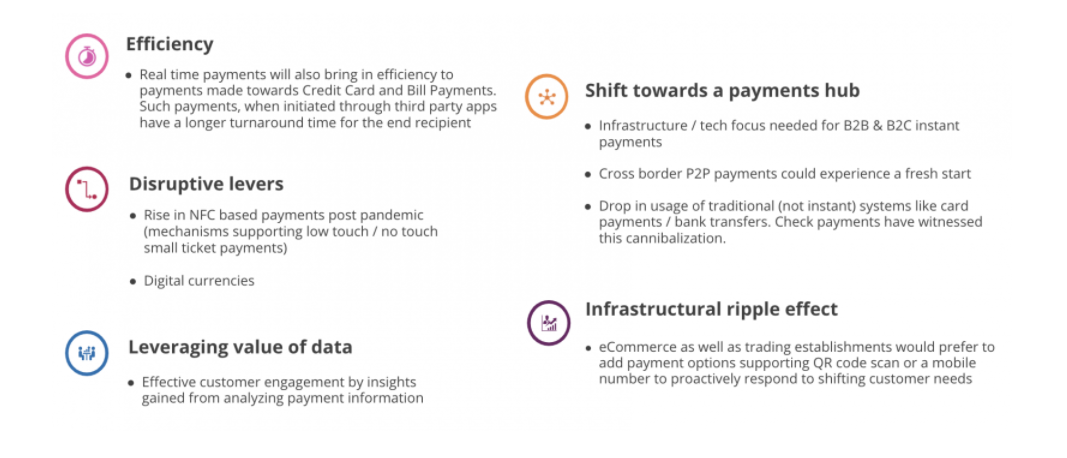

Building the future of real-time payments

The future success of real time payments will depend on how quickly and efficiently banks and financial institutions can bring about a global standardization of their RTP network ecosystem. It will also depend on the type of value added services and RTP-related benefits that customers can access. The key considerations include:

- Investing in better infrastructure. Developing an efficient real time payments platform will test a bank's existing infrastructure and their ability to process transactions. Banks will need to upgrade their infrastructure to support these transactions.

- Integration. Banks should begin to integrate with RTP systems as quickly as possible to avoid losing out to fintechs and niche merchants.

- Modernization. Banks and financial institutions need to modernize their platforms to enable easy API integration, the development of intuitive payment apps and more.

- Connectivity issues. Regulators will need to integrate offline payments solutions to increase adoption in rural or remote areas that have connectivity constraints.

- Focusing on the customer. There is plenty of opportunity to make customer experience more seamless and intuitive, including digitization of the customer journey, easy onboarding, transaction security, integration and omnichannel accessibility.

Image source: Thoughtworks

Image source: Thoughtworks

Why transaction monitoring is crucial

The financial services industry is one that deals with massive data volumes. The need to detect complex patterns in real-time, correlate this information and analyze it is critical. Leveraging the value of data through transaction analytics and insights will drive sales and provide more streamlined services to customers.

For banks, financial institutions, central infrastructures and other key players in the real time space, transaction monitoring identifies glitches in payment systems and mitigates risk. It can analyze historical information and spot abnormalities and fraud attempts.

Real time visibility simplifies complexity

With digital transaction volumes booming, new payment technologies to accommodate, and customers demanding a seamless payments experience, everyone in the payments space has more complexity to contend with than ever before.

IR Transact brings real-time visibility to your entire payments environment, unlocking unparalleled insights into transactions and trends, streamlining the payments experience, from end-to-end.

Read more about the key business drivers for real-time payments transactions for insights that can help you navigate the changing payments world.

Find out how you can monitor and analyze payment transactions with IR Transact

Request a demo

Interested to learn more about real-time payments? Download our eBook for more information.