.png?width=141&height=141&name=Transact%20(1).png)

Declined payments cost companies a staggering amount of money every year, and can significantly damage business reputation. In fact, research shows that 62% of customers who experience payment failures during an online payment process will not return to the website to try again.

Learn more about the impact of declined payments and how to manage your payments business by downloading our guide.

More than $145 billion dollars worth of online purchases are declined annually for a variety of reasons; in the case of an online subscription purchase, an expired card or incorrectly entered credit card number, or fraud suspicion. However, various studies have shown that only 1 out of 13 declined transactions was actually fraud.

Read our guide to managing and preventing declined payments here.

Payment methods and decline rates

A debit card transaction is the most popular payment method, however the gap between the credit and debit payment method is narrowing, with cash usage continuing to decline.

Due to the COVID pandemic, other payment trends have emerged, including the rise of digital wallets, P2P payments and other new payment technologies, but for now, let's look at debit and credit card decline rates.

The decline rate for credit varies between 4.5% and 7.5%, while debit declines vary between 7% for Bank of America to 12% for Chase. In fact, the worst credit card decline rates are still not as high as the lowest debit card decline rates.

Image source: Spreedly

Debit vs credit

From a customer's viewpoint, there are a number of pros and cons to using credit card vs debit card.

Debit card

When customers make a purchase with a debit card, the purchase amount is immediately withdrawn from their bank account, and they're using only existing funds. Below is a summary of the reasons for and against using a debit card as a primary payment method.

Image source: Cadence Bank

There's also a higher incidence of payment decline on a debit card if it's used overseas, as many banks and financial institutions may freeze a customer's card if it's used outside a normal payment pattern, requiring them to use different payment method.

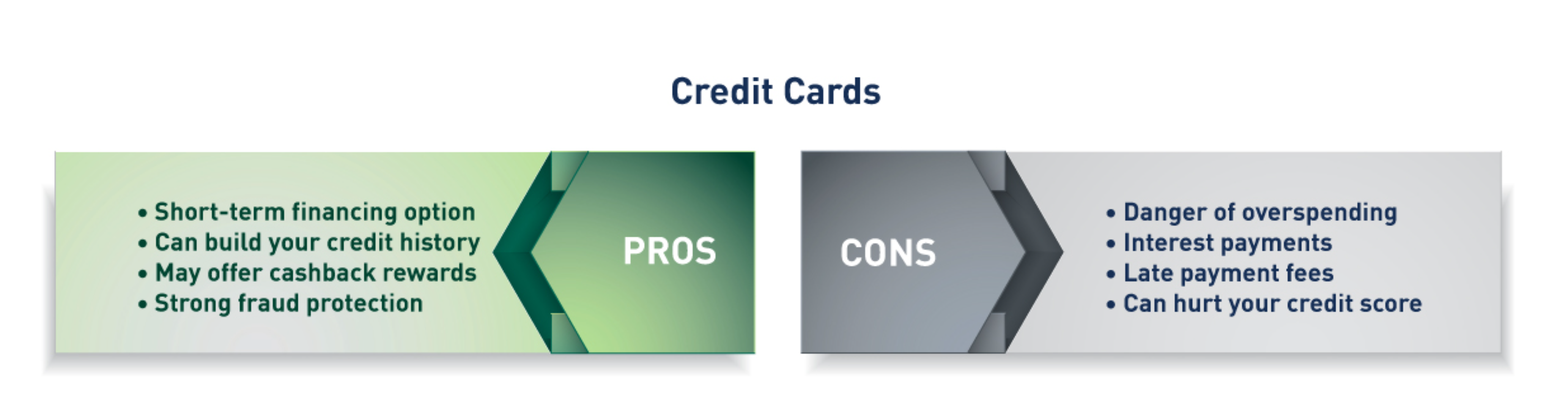

Credit card

Credit cards can offer many advantages, including cashback rewards and more robust fraud protection. A credit card can also be used to finance larger purchases, but it can lead to overspending and customers exceeding their limit.

Image source: Cadence Bank

From a merchant's perspective, payment processing fees for debit cards are substantially less than for credit cards - mostly due to the lesser risk factor. However, the higher decline rate on debit cards may often encourage merchants to suggest their customers use use a different payment method, such as a credit card.

Reasons for declined payment: Debit

Here are the main reasons a debit transaction may have been declined.

- Not enough funds in the account to cover the transaction

- The card has not been activated

- The billing address may be incorrect or need updating

- Entering the wrong PIN or CVV

- Other personal information doesn't match bank records

- Card flagged for suspicious activity

- A customer's remaining balance doesn't allow a hold on funds

- Card has reached its expiration date

- Card being used in a different country

Reasons for payment decline: Credit

Reasons for a declined credit card transaction can be similar to debit card failures, with added issues that go with borrowed funds .

- A missed payment, or history of missed payments can result in a declined card

- An unusually large purchase could cause a credit card issuer to freeze an account, causing a card decline

- A hold has been placed on a card, (e.g. for car rental or hotel deposit)and hasn't been lifted

- Card has exceeded its credit limit

Declined payments: Merchant, card issuer, and processor

Regardless of which payment method a customer chooses, payments can be declined for all the reasons listed above. But sometimes a payment failure occurs from the merchant, bank or payment processor's end, when a customer's account balance, security or card validity isn't in question. And this is where customer frustration can lead to lost sales.

- Downtime and/or system maintenance. While it's necessary for systems to close temporarily for maintenance and updates, companies should take precautions to limit this to the least busy periods to avoid unnecessary disruption.

- Security. Through the collection of customer data and payment details, banks and financial institutions use spending patterns and different locations to detect security threats and fraudulent activity. Often, perfectly legitimate transactions can be flagged, resulting in declined payments.

- Failed payment process. Payment processing involves multiple steps from the money leaving the customers' account to being deposited into the merchant’s account. Customers choose their payment method, and data is sent to the payment gateway and then the card network. This information process needs to be authorized and verified by the customer’s bank. The amount is transferred to the acquiring (merchant’s) bank, and only then to the merchant’s account. If there is an issue with any one of these steps, the payment fails. If the card issuer declines a payment, they may send feedback containing explanations as to the decline.

- Payment authentication friction. 3DS2, a multi-factor authentication protocol is designed to verify a customer's identity and reduce friction in the online checkout process. Card payment information can be shared between card provider or card issuer, issuing bank, and merchant to determine if for example, a credit card payment is risky. If so, the customer is required to provide additional information for authentication, like a fingerprint, face scan, or one-time password. If a customer is unable to provide more information to verify the transaction, or chooses not to, the payment can fail.

Using data insights to decrease declined payment rates

Although there are various tools and practices that may help merchants reduce the number of denied transactions, achieving a high approval rate is a long-term process, and each merchant should work on it continuously and strategically.

For this reason, identifying the reason for rejection behind each declined transaction will be key for the development of a sustainable strategy for any business.

To find out how using payments data can simplify complexity in your payments systems, you'll find this article helpful.

The power of payment analytics

To turn payment metrics and data into valuable information and provide value-added services, as well as differentiate in the marketplace, a card issuer, acquirer and retailer must have advanced reporting software and tools to highlight the KPIs. The more information they can gather, the more power and control they have to improve profitability, optimize revenue and cut costs.

Without transaction data and analytics to get clear visibility into the payment environment, a business wouldn't be able to identify transaction performance issues, or detect fraud, failed payments and other anomalies.

Monitoring and analyzing transactions with IR Transact

With IR Transact, merchants, acquirers, card issuers and payments providers can simplify the complexity of managing today's complex payments ecosystems.

Businesses can gain unlimited access and insights into customer usage data, and end-to-end transaction performance metrics. With dynamic visualization tools, businesses can easily get a clear view of all this information to make proactive management decisions.

Learn more about the impact of declined payments and how to manage your payments business by downloading our guide.