.png?width=141&height=141&name=Transact%20(1).png)

Understanding their impact and the critical role of monitoring for financial success.

What are high value payments?

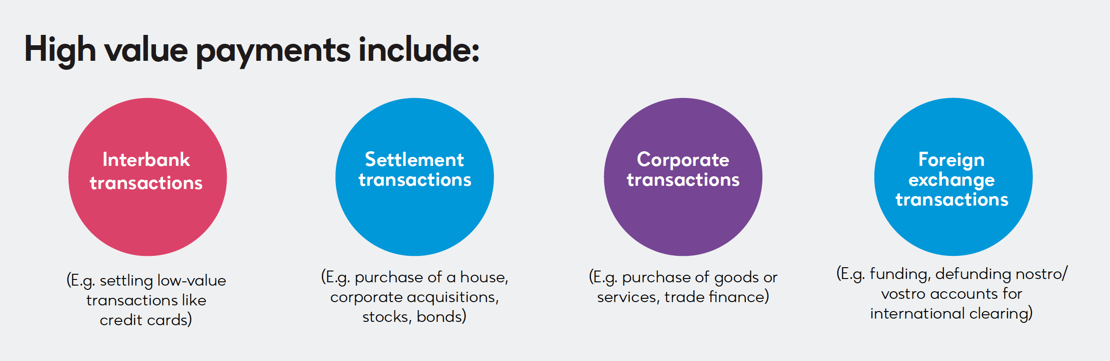

High value (or wholesale) payment systems are known by many names. Each country has different references for interbank and corporate payment schemes – such as Institutional payments, High- Value Clearing Systems (HVCSs in Australia), Large-Value Payments Systems (LVPSs in the US), Clearing House Automated Payment Systems (CHAPS in the UK).

High value payments in banking are a commodity item, and these payment types represent the largest part of the world’s payments infrastructure.

Download a PDF of Mastering High Value Payments

Regulation and compliance

Banks must comply with various regulations in their countries to ensure they operate within their respective regulatory environments.

Globally compliance rules and regulations are varied. They are specific to the jurisdiction in which the banks operate and legislated, with penalties imposed for non-compliance.

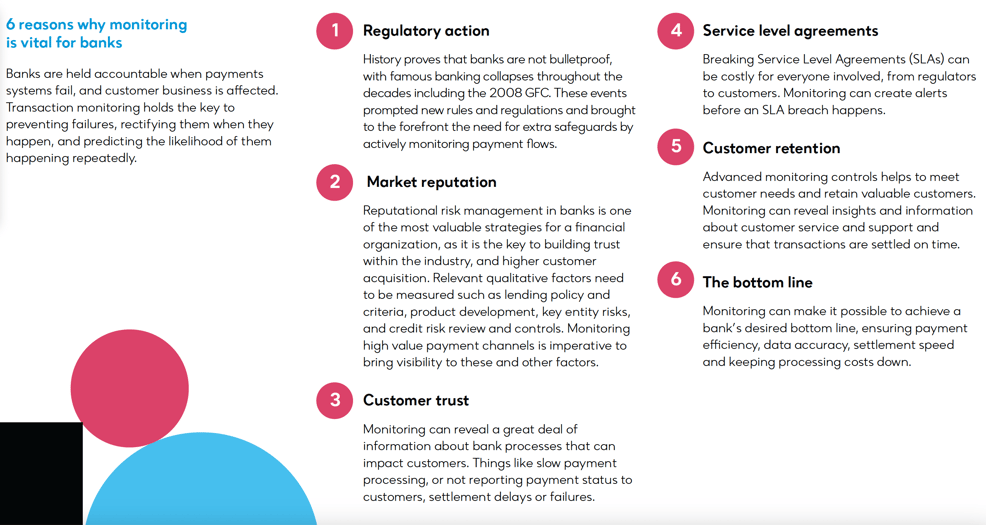

Regulators can impose significant financial penalties, not to mention the potentially devastating reputational damage that could come from a breach of SLA’s.

Monitoring high-value payment ecosystems can help banks detect and prevent potential violations of these regulations such as settlement defaults, missing daily limits or cut-off times, or flagging suspicious transaction patterns.

Stability and robustness

High-value payment systems must be stable and robust to ensure they are available and functioning as intended. System failures can result in significant financial losses and damage to a bank's reputation.

Monitoring high-value payment systems can help banks detect potential system failures and prevent them from occurring. For example, monitoring can flag potential system overload, hardware or software failure, or network issues.

Operational compliance guidelines in most jurisdictions require yearly system audits for security, robustness and resilience including mandating that fallback, disaster recovery policies systems and procedures are in place to be allowed membership in the payments network.

Legacy systems

Modern electronic payment systems have been around since the 1970’s, vendors in this space are just as old and are the dominant encumbers especially at larger banks. The technologies used are dated and the scale of business is too large to risk on a “Greenfields” buildout.

These legacy platforms get upgraded regularly to keep them current, however the core architecture of these systems precludes them from being easily interfaced with more modern systems. Dominant vendors in payment hub systems all suffer from the same legacy system syndrome, these systems are huge, complicated beasts and especially at larger banks are deemed “too big to change”.

Chapter 2: ISO 20022 and the impacts to high value

Banks and financial institutions globally have begun to transition their payment systems from using SWIFT messages exchanges network (known as ISO 15022) to the highly structured, and datarich ISO 20022 financial messaging standard.

By 2025 ISO 20022 will be the universal standard for high, or large-value payments systems of all reserve currencies.

What is ISO 2022 exactly?

ISO 20022, first introduced in 2004, is an international standard for relaying electronic messages between financial institutions.

It was created to give the financial industry a common platform for sending payments messages and exchanging payments data, using a central dictionary, a standard modelling methodology, and a series of Extensible Markup Language (XML) and Abstract Syntax Notation (ASN.1) protocols.

Why standardization is important

Standards are a critical factor when initiating financial transactions and reporting financial activity. An international standard is a way to simplify interoperability between service providers and clients, and enable the efficient, consistent, and secure exchange of files.

Traditionally, large global financial institutions have had tendencies to develop, approve and implement standards without seeking input from other organizations.

This has resulted in inconsistency, and a lack of customization, leaving overwhelmed IT departments with the task of handling onboarding, testing, and managing ongoing partner relationships.

The ISO 20022 financial messaging standard was designed to remedy this, as a flexible framework providing an internationally agreed business message syntax, where user organizations and developers will use the same message structure, form and meaning to exchange transaction information globally.

What are the benefits of ISO 20022?

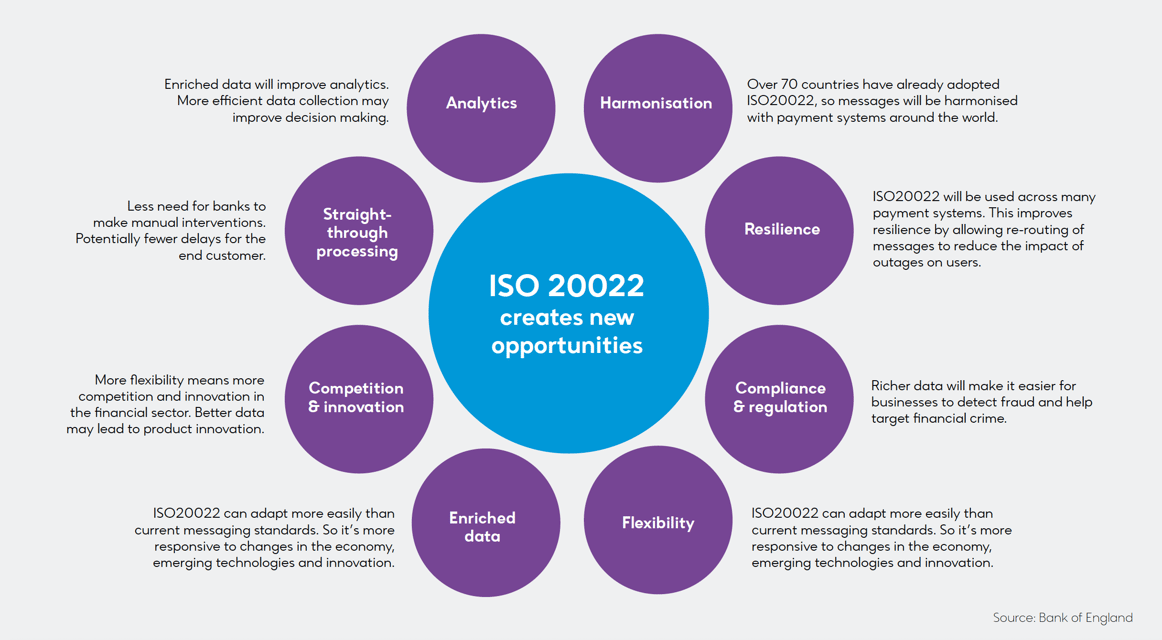

Global adoption of ISO 20022 will create a common language and model for payments data. It will provide higher quality data which translates to better quality payments for everyone in the financial industry, with an open standard that can adapt to changing needs and new approaches. As it will not be controlled by a single interest, it can be used by anyone in the industry of financial services and implemented on any network.

Key benefits include:

-

Richer, more granular data

Having enriched data at their fingertips will enable financial organizations to deliver a faster and improved service to its customers while developing new, tailored products based on analysis of customer behaviors. Increased flexibility and better data also means more competition in the financial sector, potentially leading to product innovation.

-

Better transparency and visibility

More transparency with more remittance information leads to better customer experience. Enhanced visibility and real-time perspective of liquidity flows will provide stronger forecasting capabilities. This means financial services organizations can adopt an agile approach and better manage and control their liquidity.

-

Better integration and compliance

Using modern, mainstream XML technology ISO 20022 will reach every market infrastructure and payments system to pave the way for more efficient integration. Improved analytics, requiring less manual intervention will result in a more accurate compliance process, improved security, and fraud prevention.

-

Improving STP rates

By acting as a common language among worldwide integrated systems and establishing an identical format of processing at all levels of the chain, ISO 20022 dramatically improves Straight Through Processing (STP) rates and reduces maintenance costs for all the formats. In the payments industry, efficiency is typically measured by assessing the level STP - or the percentage of transactions that are passed straight through the system from start to finish without manual intervention.

-

Regulatory and security enhancement

The higher level of detail required, and the identical standards, protocols and formats implemented allow better regulatory reporting, more secure payment information and customer data to inform business strategy and streamline security procedures. It also allows for more efficient sanctions & AML validations as well as more effective claims & investigations.

-

Creating potential new revenue streams

It improves liquidity management by providing a new level of financial communication. The ability to capture more data in a uniform way, it enables the adoption of data analysis solutions and added value services that can provide customer insights and generate new revenue streams for banks, for example Request to Pay and e-invoicing.

-

Standardizing non-Latin alphabets

An important consideration is that the standard will allow longer references for non-Latin alphabets, with a character set ten times larger than MT messages and carrying a great deal more information. This is a functionality that was widely explored in China.

Source: Bank of England

What will be the impact of the global adoption of ISO 20022?

It is expected that this worldwide adoption of this type of financial messaging will have a profound impact on financial institutions, corporations, and any business with a stake in financial services and the large value payments industry. ISO 20022 is the only way to go into the future as it is the most comprehensive financial data standard in existence today.

Over 70 countries have already adopted ISO 20022 in their payment systems including Switzerland, China, India, and Japan. And with over 200 payment types in scope, ISO 20022 will harmonize formats and data components from different payment methods that could not previously work together.

ISO 20022 will apply to domestic, ACH, high value and cross-border payments.

ISO 20022 and cross-border payments

The ISO 20022 standard will change the way banks relay cross-border payments instructions. Some banks are already prepared, while others have a lesser degree of readiness. A break in the chain could mean the potential loss of vital information. The consequences of this are a direct reflection on the bank seen to be the weaker link.

ISO 20022 and high value payments

SWIFT, along with major global banks and market infrastructures have formed the HVPS+ market practice task force to create a road map to harmonization for high value payments and real time gross settlement (RTGS).

Key challenges of ISO20022 implementation

As with any system migration, plans need to balance meeting deadlines, with solidifying a future-proof state.

The complexities of ISO 20022, along with interdependencies of implementing new industry standards can create some challenges.

-

The cost of implementation

Any legacy technology used by payments providers that pre-date ISO 20022 will need to be reviewed, mapped, and translated to the new standard. This includes the correct rules for AML, fraud, and compliance checks. In addition, outdated legacy systems that cannot process or support the ISO 20022 format need to be updated, replaced, or converted. This of course, involves budget, which needs to be agreed upon between financial institutions, stakeholders, and partners.

-

Timelines and deadlines

With different markets setting different deadlines for ISO 20022 adoption, payments firms operating across borders need to carefully plan their migration strategy, and the high-stakes complexities that go with it. Many banks are also contending with other transformation projects, so they need to ensure that their migration solutions are solid, not simply 'designed to budget' and providing a poor fit overall.

-

Managing additional information

ISO messages can be hundreds of times longer than standard payments messages. This dramatic expansion of data means that infrastructures will need to be redefined to manage the additional ISO 20022 information. Each and every character within a message must be 100% aligned with the specifications. The format is validated at several steps along the communication channel chain on the sending and receiving sides. Even a single missing colon could result in a multi-million transfer being rejected or delayed for days.

Chapter 3: How to ensure the health of your high value payments

We’ve established that high value payment systems are crucial components of the global banking industry, enabling the movement of large sums of money between banks and their customers, both domestically and internationally.

Avoiding outages is essential, but increased demand, complexity and competition heightens operational risk, banks need to do more than just avoid outages.

Robust monitoring mechanisms are essential to ensure that these systems are secure, stable, and compliant with relevant regulations. Failure to monitor high-value payment systems can result in significant financial losses for both the banks and their customers, regulatory fines, and reputational damages.

To effectively monitor these transactions, businesses need to have access to real-time data on transaction performance, including response times, success rates, and error rates.

They also need to have the ability to analyze this data to identify patterns and trends that may indicate potential issues, this is not a trivial task when you factor in the multi-layered complexity of domestic and international payment markets.

Why is monitoring high value payments crucial

The importance of monitoring high value payments cannot be overstated. First, it helps detect errors or discrepancies that may arise during the payment process. For instance, a payment may be sent to the wrong account, resulting in a delay or loss of funds.

High value payments are also a prime target for fraudsters and monitoring them can help detect fraudulent activities and prevent losses. Additionally, monitoring high value payments helps financial institutions comply with regulatory requirements and identify any suspicious activity that may indicate money laundering or terrorist financing.

Monitoring high value payments requires robust technology solutions that can detect anomalies and identify potential fraud.

By using the right tools and techniques, businesses can ensure that their high-value transactions are performing optimally and minimize the risk of costly downtime or lost revenue.

IR Transact

When dealing with high value payments, businesses need to ensure they have oversight over large value and high priority payments. Monitoring even a single payment can be complex, requiring multiple checks, balances, and approvals.

Without detail into these transactions, issues such as settlement or processing delays can cause major impacts to banks and corporations, including losing customer trust, regulatory action and penalties, and negative credit rating.

IR Transact’s solution for High Value Payments provides a single dashboard to monitor the health of your high value in-flight transactions across payment queues and delivers an end-to-end view of transactions impacting associated bank accounts.

To effectively monitor these transactions, businesses need to have access to real-time data on transaction performance, including response times, success rates, and error rates.

Leverage your own business data to get a view of key accounts, such as your Settlement or High Value customer accounts, and easily monitor balance thresholds, flagged accounts, project liquidity shortfalls or abnormal account usage patterns.

With IR Transact you can ensure that anomalies, such as bottlenecks and processing backlogs are identified as they develop, ensuring you get ahead of potentially disruptive events before they occur and saving you time monitoring and analyzing time-critical data and systems.

Download a PDF of Mastering High Value Payments