.png?width=141&height=141&name=Transact%20(1).png)

By deploying high-performance AI models for transaction monitoring, banks financial institutions and payment providers are keeping pace with financial crime, and turning compliance into a strategic advantage.

But the role of artificial intelligence-based transaction monitoring solutions extends beyond risk management, financial crime compliance and fraud prevention.

What is AI-based transaction monitoring?

AI-based transaction monitoring is vital for gaining valuable insights into a payment infrastructure, by:

-

Enhancing customer risk assessment

-

Maintaining market integrity

-

Protecting an organization's reputation.

It involves the use of artificial intelligence and machine learning algorithms to analyze payment transactions in real-time. Advanced transaction monitoring tools can proactively detect anomalies, fraud patterns, and compliance risks faster, with greater accuracy and fewer false positives than traditional rule-based systems.

By tailoring transaction monitoring rules and thresholds to specific behaviors and profiles relevant to a business, AI far surpasses manual tuning, reducing the chances of missed risks.

It continuously learns from transaction data to identify suspicious activity across complex, multi-channel payment ecosystems while adapting to evolving fraud tactics, money laundering and regulatory requirements.

What makes AI monitoring different from traditional transaction monitoring?

Traditional transaction monitoring systems rely on rule-based logic - a set of predefined thresholds and static conditions that determine what constitutes suspicious behavior.

For example, if a customer transfers more than a set limit of funds within 24 hours or makes multiple cross-border transactions in quick succession, the system raises an alert.

While this risk detection approach provides structure and regulatory consistency, the major drawbacks are rigidity and volume - or the inability to adapt to evolving emerging threats. Additionally, they often generate a high number of false-positive alerts, which can inundate compliance teams with alerts that lead nowhere.

Fraudsters, of course, are well aware of this, and learn how to operate just below detection thresholds or vary their behavior to stay invisible. Traditional systems are often reactive rather than proactive, responding to alerts generated, instead of anticipating suspicious activity.

Rule-based vs AI-models: Reactive vs proactive monitoring

AI-based transaction monitoring changes this paradigm completely. Instead of relying on static rules, AI and machine learning algorithms have the ability to analyze vast amounts of data to identify patterns, correlations, and anomalies that humans or rigid systems might miss.

They learn from historical transactions, continuously refining their models to detect new fraud techniques as they emerge. By incorporating contextual analysis, such as customer behavior, transaction history, device fingerprinting, structured and unstructured data like communication patterns, AI systems understand why something looks unusual, not just that it does.

The result is a more intuitive, far more adaptive approach that dramatically reduces false positives and identifies anomalous fraud patterns before they escalate.

An AI-powered transaction monitoring system doesn’t replace human oversight; it enhances it, allowing compliance teams to improve efficiency, and focus on the alerts that truly matter. In industries where speed, accuracy, and regulatory scrutiny are the highest priority, the shift from rule-based to AI-driven monitoring marks a decisive step toward proactive financial crime prevention.

How AI transaction monitoring works: Technical breakdown

Transaction monitoring powered by AI models relies on a suite of technologies that work together to detect risk, adapt to change, and give compliance teams sharper, more actionable insights. Below are the main building blocks.

1. Machine Learning (ML)

Machine learning refers to algorithms that improve their performance over time as they are exposed to more data. In financial transaction monitoring, two main methods are used:

-

Supervised learning: The AI model is trained using historical data that’s already labeled (for example, transactions confirmed fraudulent vs legitimate). It learns patterns that distinguish “bad” from “good” activity, and then applies what it’s learned to new transactions.

-

Unsupervised learning: Here, the AI model looks for unusual patterns without being told explicitly what “fraud” looks like. It might cluster transactions by similarity, then flag those that don’t fit into any cluster (i.e. outliers) as suspicious.

-

Semi-Supervised Learning: Hybrid approach combining labeled and unlabeled data

These ML techniques allow systems to adapt to changing fraud patterns. They can pick up subtle shifts, unusual transaction volumes, odd transaction times, or patterns across multiple accounts that rule-based systems might miss.

2. Neural Networks / Deep Learning

Neural networks mimic the way human brains work at a basic level, by having many layers of “neurons” (mathematical functions) that pass signals to one another. Deep learning makes it possible to recognize very complex, non-linear relationships in data.

For example, deep learning can help in detecting sequences of behavior: a user logging in from one location, making small transactions, then suddenly doing something very different. Or spotting patterns across datasets that combine transaction metadata, geographical info, device data, etc. Deep learning can be particularly useful in detecting fraud patterns that haven’t been seen before.

3. Anomaly Detection Algorithms

Anomaly detection is about spotting what’s unusual. There are different kinds:

-

Isolation forests, clustering methods (e.g. k-means, DBSCAN): These group similar transactions together, then find those that don't belong.

-

Autoencoders: A kind of neural network trained to compress (encode) data then reconstruct it. If a transaction reconstructs poorly, it may be anomalous.

-

Generative AI models (GANs, Variational Autoencoders, etc.): These can generate or model what “normal” data looks like, then detect stuff that doesn’t match.

-

Time-series anomaly detection: Many fraud or illicit activities reveal themselves through temporal patterns, like sudden spikes, or seasonal irregularities. Algorithms that examine time-based features help detect these.

Anomaly detection helps catch the “unknown unknowns” - or behaviors not anticipated by rules.

4. Predictive Analytics

Predictive analytics uses historical data plus statistical techniques to forecast potential risk before it becomes a problem. In transaction monitoring this could mean:

-

Assigning risk scores to customers or transactions based on behavior history.

-

Forecasting metrics like “what’s the probability this user’s pattern will escalate to fraud?”

-

Using features such as transaction amount trends, geolocation variance, frequency of transactions, device or channel changes, etc.

Because predictive models combine many signals, they can often give earlier warnings than rigid rule triggers.

5. Contextual & Hybrid Methods

Though sometimes overlooked, combining structured and unstructured data is powerful. That involves the use of:

-

Contextual signals - like customer history, geography, time of day, device fingerprinting.

-

Hybrid models - that combine ML + rules + anomaly detection: rules still play a role (for clear regulatory thresholds), but AI augments them and handles complexity.

6. Continuous Learning & Adaptation

One aspect that makes AI different is not just the model you begin with, but how it evolves. AI models can be updated with new fraud cases, new data sources, feedback loops (human adjudication), etc. This continuous influx of information ensures the monitoring system stays relevant even as fraudsters change tactics.

“With the ever-increasing volume of transaction data, from varied sources and formats, the traditional rule-based monitoring methods are no longer enough. Today, organizations need anomaly detection platforms driven by unsupervised machine learning and predictive analytics to uncover unknown risk patterns in real time.”

– Manpreet Singh Ahuja, Partner & Chief Digital Officer, PwC India

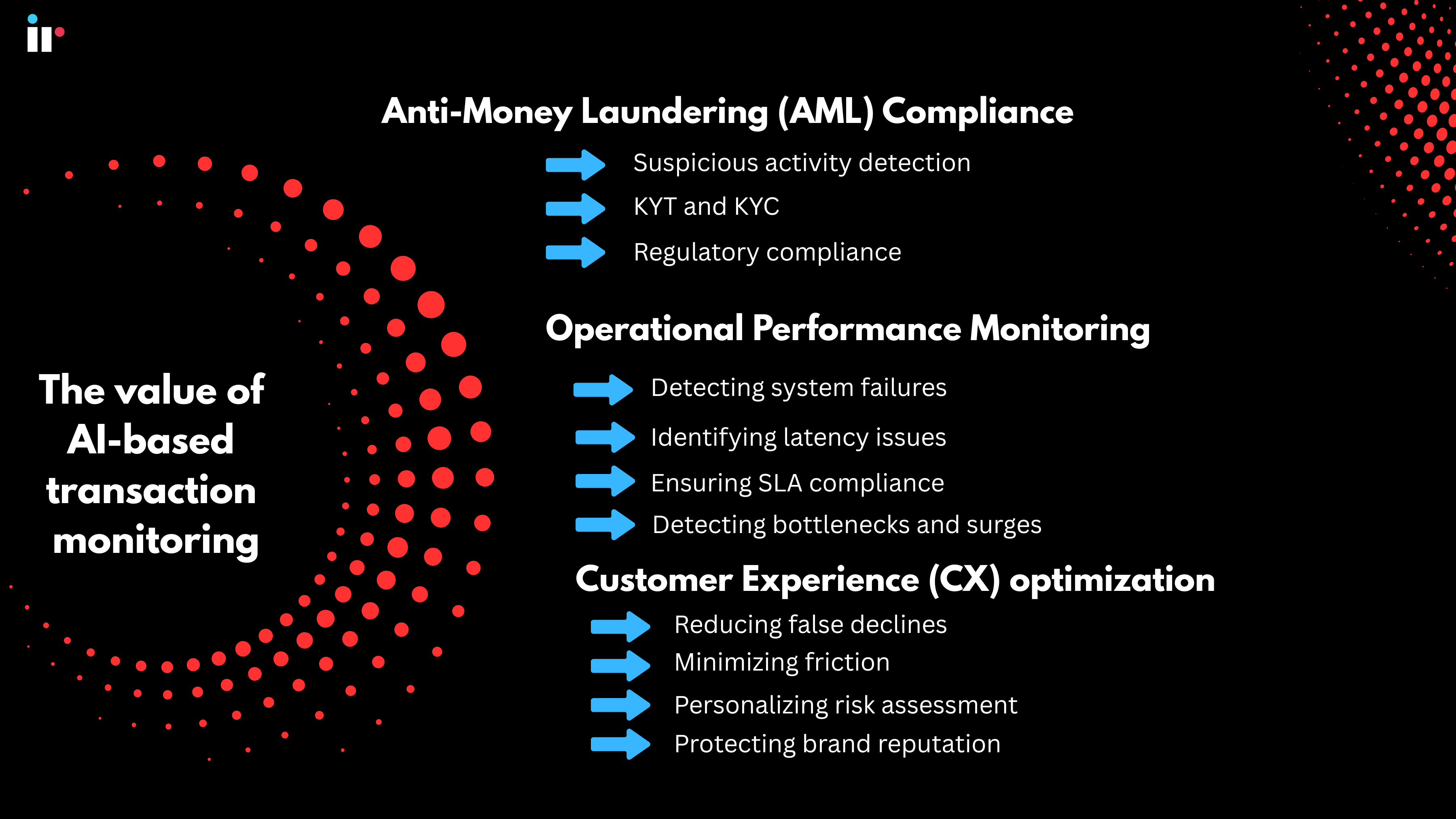

Key use cases for AI-based transaction monitoring

AI-based transaction monitoring is valuable in many ways beyond simply curtailing financial crime. Below are three of the most important use cases, showing how AI tools excel at risk management, by delivering impact in compliance, operations, and customer experience.

Anti-Money Laundering (AML) Compliance

-

Suspicious Activity Detection: AI models can detect suspicious behavior patterns that static rules would miss. For example, structuring (many small deposits) spread over multiple accounts, sudden changes in transaction behavior, or atypical geographical flows. AI technology can identify the transactions that are not posing the transactional risk of money laundering and terrorist financing.

-

Know Your Transaction (KYT): As well as performing customer due diligence in KYC (Know Your Customer), KYT focuses on the transaction level. AI helps financial institutions map each transaction in context (who is making transactions, what typical history looks like, channels used, etc.) so that fraud detection is flagged more precisely.

-

Regulatory Compliance: Global bodies like the Financial Action Task Force (FATF) and national regulators (for example FinCEN in the U.S., and local financial services authorities in APAC/MEA) require financial institutions to monitor transactions for suspicious patterns, submit SARs (Suspicious Activity Reports), and maintain a full audit trail. AI helps satisfy those requirements by increasing detection capability, reducing the incidence of false positives, and improving traceability.

Case study:

One of the world's leading banks, HSBC, faced massive volumes of false-positive alerts (over 95%) from its rules-based system, leading to slow and costly human reviews. Implementing AI-powered solutions allowed it to significantly reduce false positives, provide more pertinent information to law enforcement, and improve customer satisfaction. The success led to the bank receiving the "Celent Model Risk Manager of the Year 2023" award.

Operational Performance Monitoring

Traditional transaction monitoring systems are focused almost exclusively on fraud and compliance. But AI systems can also monitor the health of the transaction processing systems themselves, making a significant impact on operational efficiency. This includes:

-

Detecting system failures, including server or infrastructure issues that delay or drop transactions.

-

Identifying latency issues, for example, when transaction authorization or clearing is delayed, which can degrade user experience.

-

Spotting processing bottlenecks, such as surges overwhelming a part of the pipeline (e.g. API endpoints, third-party dependencies).

-

Ensuring internal or external SLA compliance, including transaction response times, error rates, uptime.

-

Monitoring customer experience impacts beyond financial crime, for example false declines or delays which frustrate users, impacting conversion, retention, or brand reputation.

AI-based transaction monitoring differentiates by enabling proactive detection, so operational teams can address issues before they escalate into outages or widespread customer complaints.

Customer Experience (CX) optimization

-

Reducing false declines: Traditional systems often err on the side of caution, declining or flagging legitimate financial transactions because of over-broad or poorly tuned rules. AI models, by analyzing behavioral history and richer context, can more accurately distinguish risky vs safe transactions, meaning less false positives.

-

Minimizing friction: AI monitoring can help design smoother customer journeys, for example allowing low-risk users to encounter fewer hurdles (less friction) by escalating reviews only when necessary. This might mean fewer multi-factor authentication (MFA) steps for trusted users, or fewer interruptions for validation.

-

Personalizing risk assessment: AI excels at risk management by tailoring risk scores per customer or per transaction type, taking into account prior behavior, devices used, geolocation, etc. A high-value, long-standing customer will be treated differently than a first-time user in a high-risk geography.

-

Protecting brand reputation: When customers experience declines, delayed transactions, or poor performance, it damages trust. By reducing false alerts and improving operational reliability, AI monitoring helps ensure smoother transactions, higher approval rates, and overall better perception of the company.

Comparison table

|

Use Case |

Traditional Monitoring Challenges |

AI Monitoring Benefits |

Key Metrics to Track |

|

AML Compliance / Suspicious Activity Detection |

Static rules miss evolving fraud patterns; many false positives; high manual investigation effort |

Detects novel financial crime/ money laundering; improves precision; reduces work for compliance teams; stronger audit trails |

False positive rate; # of suspicious transactions correctly flagged; time to resolve/full investigation; compliance/regulatory penalty incidents |

|

Operational Performance Monitoring |

Little visibility on system performance or process bottlenecks; often reactive rather than proactive |

Real-time system health monitoring; early detection of latency / failures; ensures SLAs; improves uptime and reliability |

Transaction processing time; latency distribution; system error rates; SLA breach rate; downtime incidents |

|

Customer Experience Optimization |

High friction for legitimate users; false declines; poor UX when rules are over-broad; brand damage |

Reduced false declines; more frictionless experience for low-risk users; personalized risk scoring; better customer satisfaction |

Conversion rate / approval rate; customer complaints related to declines; average time to complete transaction; NPS or CSAT; retention or churn related to transaction issues |

Challenges & Limitations of AI in Transaction Monitoring

While AI brings powerful capabilities to transaction monitoring, it is not a silver bullet. Understanding the limitations of AI-based transaction monitoring is crucial for designing realistic expectations and governance frameworks.

1. Data quality and availability

AI models are only as good as the data they learn from. Inconsistent, incomplete, or outdated transaction data can lead to inaccurate issue detection.

Example: Merging data from multiple systems, or legacy banking platforms alongside modern fintech applications can introduce errors.

2. Explainability & regulatory scrutiny

Many financial regulators require firms to demonstrate why a transaction was flagged as suspicious. Complex AI models, particularly deep learning networks, can become “black boxes,” making it hard to justify decisions to auditors or regulators. Compliance teams face the task of balancing model sophistication with explainability, often using hybrid approaches that combine AI scoring with rule-based logic for transparency.

3. False positives and negatives

While AI lessens false positives compared to static rule systems, it's far from perfect. Poorly trained models, biased data, or overfitting can still generate alerts that are irrelevant or miss genuinely suspicious transactions. Continuous monitoring, retraining, and human oversight remain essential.

4. Integration with existing systems

Many organizations operate hybrid environments with legacy monitoring systems. Integrating AI monitoring tools and external data sources with these existing infrastructures can be technically challenging and requires careful planning to avoid disruption to ongoing operations.

5.Cost and resource considerations

Building, maintaining, and scaling AI-based monitoring involves upfront investment in technology, people, and processes. Financial institutions need to weigh the benefits of improved detection, lessen false positives, and operational efficiency against ongoing costs.

FREQUENTLY ASKED QUESTIONS:

Q: How accurate is AI-based monitoring compared to traditional systems?

A: It's generally significantly more accurate than traditional rule-based systems, particularly when dealing with financial risk management, anti money-laundering (AML) and financial crime. Traditional systems rely on static rules and thresholds, which can miss suspicious activity.

Q: What types of transactions can an AI-based monitoring solution analyze?

A: Any digital transaction processed by a financial institution or business, including card payments, wire transfers, ACH transactions, mobile and online payments, cross-border transfers, and peer-to-peer transactions. It can also incorporate non-traditional or unstructured data, like account behavior, device information, geolocation, and payment channel metadata. Any activity that generates transactional data can be monitored, allowing AI to spot fraud, money laundering, or operational anomalies across multiple channels in real time.

Q: How long does it take to implement AI-based monitoring systems?

A: A few weeks to a couple of months. Large enterprises with multiple legacy systems, cross-border operations, or extensive regulatory requirements may take several months for full deployment. Key factors include data preparation, model training, integration with existing workflows, and validation. A phased approach, starting with high-risk transaction types and gradually expanding coverage will minimize operational disruption.

Q: Do I need to replace my existing transaction monitoring system?

A: Not necessarily. Many organizations implement AI as a complement to existing rule-based systems, creating a hybrid approach. AI can handle anomaly detection and adaptive learning while rules manage known patterns and specific compliance requirements. This allows for phased migration and risk mitigation.

Q: What data is required to train AI-based transaction monitoring models?

A: Effective AI models require historical transaction data (typically 12-24 months), labeled examples of fraudulent and legitimate transactions, customer profile information, device and behavioral data, and contextual information like geographic location and transaction timing. Data quality and completeness directly impact model performance.

Q: How does AI-based transaction monitoring handle new fraud patterns it hasn't seen before?

A: Unsupervised learning and anomaly detection algorithms allow AI to identify unusual patterns and behaviors that deviate from established baselines, even without prior labeled examples. The system flags these anomalies for investigation and incorporates feedback to continuously improve detection of emerging threats.

Q: Is AI-based transaction monitoring accepted by financial regulators?

A: Yes, regulators increasingly recognize AI and machine learning as valuable tools for transaction monitoring, provided organizations can demonstrate model governance, explainability, validation, and appropriate oversight. Key requirements include audit data, documentation of decision-making logic, and human review processes for high-risk decisions.