.png?width=141&height=141&name=Transact%20(1).png)

The process of quickly and efficiently moving money around the world is a crucial element of a healthy, thriving global economy.

The rise of global eCommerce marketplaces, with internationally based merchants and vendors needing to pay at various times, using different methods has always created considerable complexity.

In the past, cross-border payments were typically slow, costly, and inefficient, not to mention mired in complicated fees, regulations, and taxes. And progress to improve cross-border payment processes has been painfully slow.

But today, with transformational reforms, a conflux of huge advancements in technology and determination from policymakers, significant improvements have influenced the state of cross-border payments.

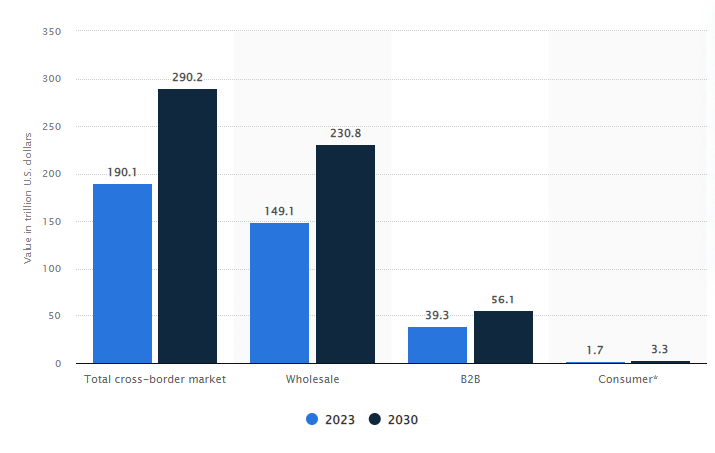

The value of cross-border payments

The internationalization of goods and capital markets puts cross-border payments at the heart of global economic activity. The need to answer the worldwide call for reform, has prompted banks and fintech companies to prioritize their investments in more efficient and up-to-date cross-border payment technology.

According to Statista, the total value of cross-border payments worldwide is forecast to increase by over 65% by 2030, to $290.2 trillion. The chart below shows the global wholesale, B2B, and B2C market values, and their projected values over the next 7 years.

Instigating change

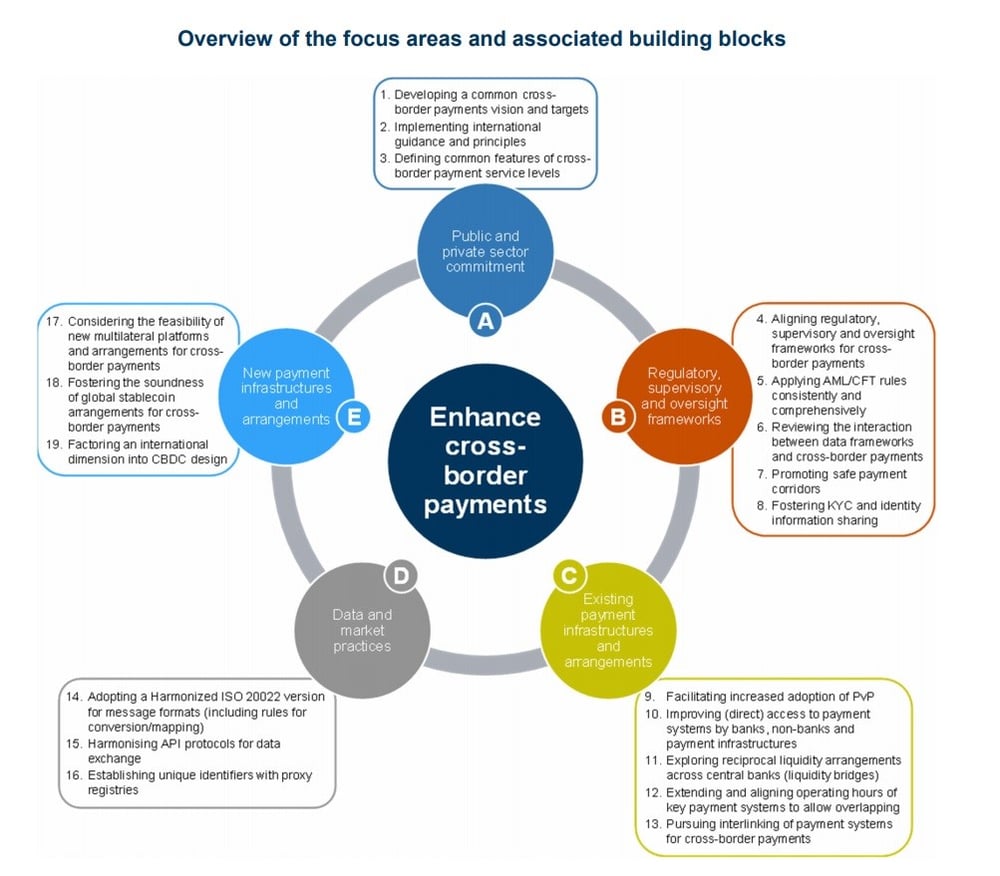

Since 2020, the Roadmap for Enhancing Cross-border Payments, created by G20 leaders, has accomplished a great deal.

The instigation of the roadmap’s 19 building blocks (BBs) has brought about improvements in existing and potential multilateral processes.

Image source: FSB

The key aim was to make cross-border payments, including remittances faster, cheaper, more inclusive, and transparent, while upholding safety and security.

The launch of the roadmap has created widespread benefits for citizens, organizations, and global economies.

Speedy, cost effective, more transparent, and more inclusive cross-border payments will undoubtedly bring about universal advantages for companies conducting transnational business, tourists visiting other countries or migrants sending money home to their families.

These benefits support economic growth and global development, as well as enhancing international trade and financial inclusion.

Navigating the roadblocks

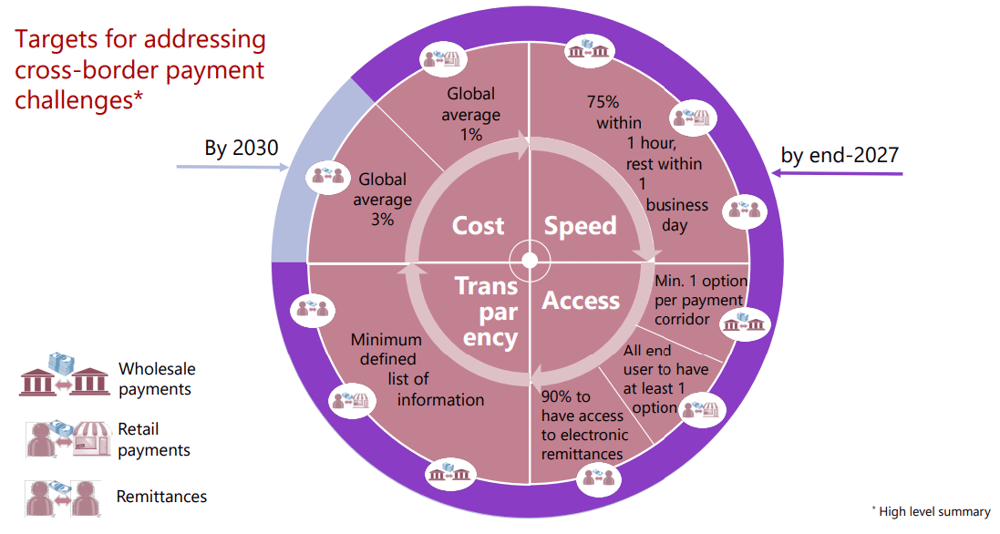

The FSB’s primary stance is the reduction of cross-border payment barriers for organizations and for citizens.

Changes to long-standing cross-border payment processes have already had a bearing on the stability of the international monetary system, particularly following the pandemic.

While much-needed reforms are ongoing, getting cross-border payment reform to where it needs to be sooner, will only be possible with global co-operation.

These are the four primary roadblocks for cross-border payments, and the FSB’s targets for addressing them.

Cost

Cross-border payments have always been expensive, with several intermediaries involved, all of whom charge fees for their services. There may also be hefty FX fees for converting from one currency to another, as well as varying regulatory costs.

International commerce is continuing to grow, crowding the cross-border payment space with overseas workers and global businesses. Banks, finance institutions and businesses now realize that they need to offer competitive rates to hang on to cross-border customer business.

Speed

Due to legacy technology, regulation, back-end processes, and market structure, sending money from one country to another is traditionally slow. Payments may be routed through many banks and intermediaries before they reach their destination, causing delays and incurring fees. Innovations in technology like digital wallets are enabling same-day payments.

International accounts for businesses with a multi-currency IBAN are helping manage cash flow trading history, and data.

Transparency

Sending and receiving funds across borders can often be fraught with uncertain and obscure processes that cause friction and frustration. With little to no choice over how transactions are conducted, customers are faced with unpredictable transfer speed, no clarity as to status of funds transfer, often waiting days for notification, and high costs. International communities and regulatory bodies worldwide are making transparency a global mandate.

Inclusion

Cost effective, transparent, and speedy financial services are part of a domestic payment system that most of the world takes for granted. But these key tenets often remain elusive to hundreds of millions of people and business owners making cross-border payments. Part of the FSB’s Roadmap is to ensure that 90% of customers have access to electronic remittances.

How technology is transforming the cross-border payments space

Digital innovation is being embraced by banks and their fintech partners, transforming the cross-border payments experience for treasurers, their beneficiaries, and their customers.

Let’s look at some of these technological breakthroughs.

ISO 20022 messaging standard

The period of co-existence between the legacy SWIFT MT standard and ISO 20022 ends in 2025. ISO 20022 enables richer, more structured data, an essential element of the next generation of cross-border payments.

ISO20022 will give financial institutions the ability to work smarter and faster, leading to greater operational efficiency in cross-border payments. It is one of the key factors driving innovation, particularly in the APAC and Middle East regions.

Real time FX rates with APIs

Global organizations are continually testing their digital solutions to optimize their cross-currency workflow without having a negative impact on their existing operations.

APIs are becoming a preferred solution to facilitate cross border payments, as they are relatively simple plug-and-play solutions. APIs integrate seamlessly into existing treasury infrastructure and interfaces allowing organization treasurers to access real-time visibility into FX rates. Early access to Foreign Exchange rates enables organizations to manage currency exposure, mitigate risk across global accounts and enhance reconciliation more effectively.

Virtual accounts for wider global reach

The flexibility to manage cash flow across currencies through a centralized account structure is invaluable to businesses, meaning they no longer need to maintain multiple local accounts in the same markets.

With centralized account structures, organizations can then easily manage balances held in one account in one currency to another account in another currency, or fund local payments using a centralized account. This maximizes liquidity, allowing them to operate in the currencies that best suit their business.

The regulatory landscape for cross-border payments

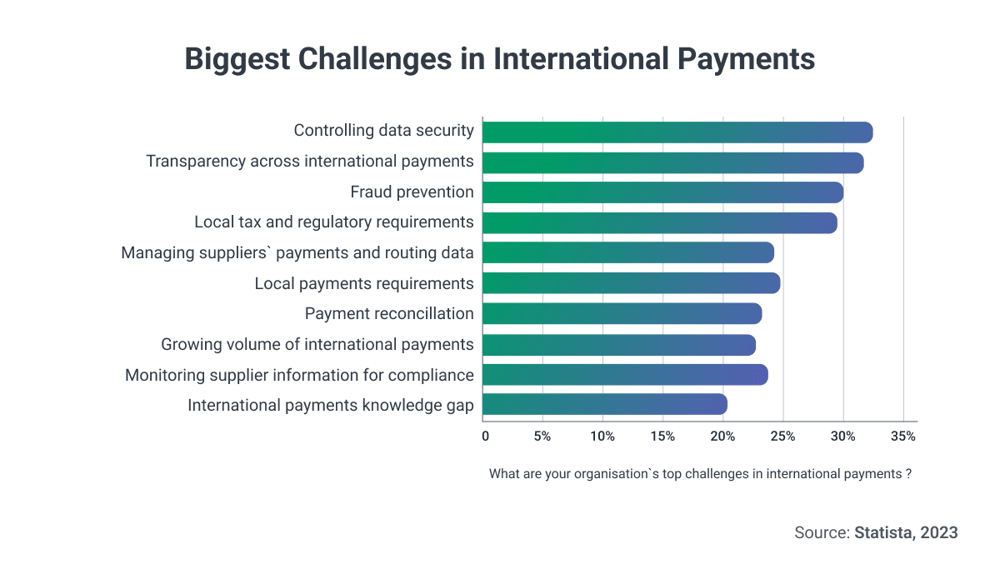

Legislation and compliance standards have always been a complicated path to navigate in cross-border payments.

To simplify cross-border payments and improve security, new digital technology innovations are making things easier. Digital identity technology is allowing fintech firms and creative startups to offer compliance solutions and expedite verification processes.

Regulation in cross-border payments is complex because it’s governed by international treaties and agreements, in addition to national regulations. This makes the exchange of information between FIs and regulators another important aspect of cross-border payment regulation.

Preventing money laundering and other illegal activities like terrorist financing, tax evasion, and fraud are high priorities for regulators, so strict anti-money laundering (AML) and know-your-customer (KYC) procedures need to be implemented and reviewed often. This includes verifying customer identities, and stringently monitoring cross-border transactions for suspicious activities.

Another crucial factor is implementing robust security measures, including encryption, multi-factor authentication, and secure payment systems to prevent unauthorized access to funds and protect against fraud and hacking.

The immediate future of cross-border payments

As the global cross-border payment landscape evolves, there are several trends emerging that could fundamentally change competitive dynamics.

- There is rising pressure from advanced technologies such as Distributed Ledger Technology (DLT) and card and network innovations. This is influencing international commerce in retail and corporate sectors.

- Customers demands and shifting regulatory and sanctions and frameworks.

- The increase in digital access points using smartphones and alternative payment methods (APMs) for remittances has boosted new demands that businesses are under pressure to meet.

- Alternative solution providers that provide faster, cheaper, and more transparent cross-border payment solutions are beginning to gain a competitive advantage over banks.

Innovative technologies are helping to remove the barriers that prevent smooth, efficient cross-border payments by addressing legislative complexity, and promoting inclusion and accessibility.

Technology is also helping to speed up settlement times and promote global connectedness.

Global organizations and individuals are now taking advantage of these innovative digital and technological opportunities to embrace new growth prospects and improve financial efficiency in cross-border payments.

Find out more about cross-border payments

Read our comprehensive Guide To Secure Cross-Border Payments

Emerging payment methods are a driving force for more financial inclusion. For example, in countries like Brazil and India, the next wave of innovation and economic growth is being spearheaded by younger populations who have grown up with technology.

Demand for alternatives to traditional wire transfers is also growing in Korea, where consumers and businesses increasingly expect solutions that enable low-cost, instant cross-border payments.

Digital payments are also being embraced by older demographics, who are not only surrendering to necessity, but recognizing the convenience.

The importance of real-time payment analytics

Payment trends are continuing to change with lightning speed. Real-time analytics have never been more important to measure and analyze payment data, view growth, and make decisions throughout the payment chain.

The power of data management and analytics is in having the ability to correlate different points of data. This enables organizations to identify security threats and fraud attempts, study metrics to observe patterns and ultimately detect system abnormalities.

Find out how monitoring your payments system with IR Transact can keep organizations on top of emerging technologies and regulatory changes. Complete visibility into your payment system will turn data into intelligence, assuring safe, efficient domestic and cross-border payments now and in the future.